Menghitung Pajak Penghasilan PPh 21 terbaru tahun 2023 #pph21 #pajakpenghasilan #pajak

Summary

TLDRIn this video, the host explains the updated income tax rates (PPH 21) that took effect in Indonesia starting January 2023. The tax system is progressive, with rates ranging from 5% for income up to 60 million IDR to 35% for income above 5 billion IDR. The host also discusses tax exemptions (PTKP), deductions, and examples of how to calculate income tax based on different income levels. Through examples, the video simplifies the tax calculation process, making it easier to understand for both individuals and married taxpayers with dependents.

Takeaways

- 😀 The new PPH 21 tax rates for 2023 are as follows: 5% for taxable income (PKP) up to 60 million IDR, 15% for 60 million to 250 million IDR, 25% for 250 million to 500 million IDR, 30% for 500 million to 5 billion IDR, and 35% for income above 5 billion IDR.

- 😀 The tax rate has been adjusted from 50 million IDR to 60 million IDR as the threshold for the 5% tax bracket, and the maximum tax rate was raised to 35% for incomes above 5 billion IDR.

- 😀 Individuals earning below 5 million IDR per month (54 million IDR annually) are exempt from income tax as their income falls under the non-taxable income (PTKP) category.

- 😀 The PTKP value is 54 million IDR for single individuals, 58.5 million IDR for married individuals, and an additional 4.5 million IDR for each child or dependent, up to a maximum of 3 dependents.

- 😀 For a married couple with no children, the PTKP is 58.5 million IDR, but with 3 children, it rises to 72 million IDR for the couple's combined income.

- 😀 Tax deductions can include 'biaya jabatan' (job expenses), which is 5% of the gross income, with a maximum deductible amount of 500,000 IDR per month (6 million IDR annually).

- 😀 The script illustrates how to calculate PPH 21 using a series of example calculations, starting with a person earning 5.5 million IDR per month. The tax rate applied is 5% on the taxable income after deductions.

- 😀 In the second example, a person earning 7.5 million IDR per month (90 million IDR annually) with BPJS and pension contributions is subject to a tax of 1.26 million IDR per year after deductions.

- 😀 The third example involves a person earning 12.5 million IDR per month, with a taxable income of 75 million IDR after deductions. The tax calculation uses multiple rates: 5% for the first 60 million IDR and 15% for the remaining amount.

- 😀 The PPH 21 tax system is progressive, meaning the higher the income, the higher the tax rate applied. This ensures that individuals with larger incomes pay a proportionally higher amount of tax.

Q & A

What are the income tax rates for PPH 21 in Indonesia for the year 2023?

-The income tax rates for PPH 21 in 2023 are as follows: 5% for income up to 60 million IDR, 15% for income between 60 million to 250 million IDR, 25% for income between 250 million to 500 million IDR, 30% for income between 500 million to 5 billion IDR, and 35% for income above 5 billion IDR.

How do the 2023 tax rates compare to the previous year?

-In 2023, the tax rates start at 5% for incomes above 60 million IDR, compared to 50 million IDR in previous years. The maximum tax rate has also increased to 35% for incomes above 5 billion IDR, compared to the previous maximum rate of 30%.

What is the minimum income threshold to be liable for PPH 21 tax in 2023?

-In 2023, the minimum taxable income threshold for PPH 21 is 5 million IDR per month. Income below this threshold is not subject to income tax.

How is PTKP (Non-Taxable Income) calculated for individuals in Indonesia?

-PTKP is calculated based on the individual's marital status and dependents. A single person has a PTKP of 54 million IDR, a married person with no children has 58.5 million IDR, and a married person with children can have up to 67.5 million IDR in PTKP, with an additional 4.5 million IDR per child.

What is the maximum allowable job expense deduction (biaya jabatan) for tax purposes?

-The maximum allowable job expense deduction is 5% of the gross income, with a cap of 6 million IDR per year or 500,000 IDR per month.

What is the significance of BPJS contributions in calculating PPH 21 tax?

-BPJS contributions, both for health (BPJS Kesehatan) and employment (BPJS Ketenagakerjaan), are deducted from the gross income to determine the taxable income (net income). These deductions help reduce the amount of income subject to tax.

How do you calculate the taxable income (PKP) for a married person without children?

-For a married person without children, the PTKP is 58.5 million IDR. The taxable income (PKP) is calculated by subtracting this PTKP from the net income. For example, if the net income is 83.7 million IDR, the PKP would be 25.2 million IDR.

What is the tax liability for an individual with a taxable income of 7.5 million IDR per year?

-For an individual with a taxable income of 7.5 million IDR per year, the tax rate applied would be 5%. The tax liability would be 5% of 7.5 million IDR, which equals 375,000 IDR per year.

How are tax calculations adjusted when a person has multiple dependents?

-When a person has multiple dependents, the PTKP increases. For example, a married person with three children has a PTKP of 72 million IDR. This higher PTKP reduces the taxable income (PKP), leading to a lower overall tax liability.

How do you calculate the tax liability for someone with a taxable income of 75 million IDR?

-For someone with a taxable income of 75 million IDR, the tax is calculated using two tax brackets. The first 60 million IDR is taxed at 5%, and the remaining 15 million IDR is taxed at 15%. The total tax liability would be 3 million IDR (5% of 60 million IDR) plus 2.25 million IDR (15% of 15 million IDR), totaling 5.25 million IDR.

Outlines

Esta sección está disponible solo para usuarios con suscripción. Por favor, mejora tu plan para acceder a esta parte.

Mejorar ahoraMindmap

Esta sección está disponible solo para usuarios con suscripción. Por favor, mejora tu plan para acceder a esta parte.

Mejorar ahoraKeywords

Esta sección está disponible solo para usuarios con suscripción. Por favor, mejora tu plan para acceder a esta parte.

Mejorar ahoraHighlights

Esta sección está disponible solo para usuarios con suscripción. Por favor, mejora tu plan para acceder a esta parte.

Mejorar ahoraTranscripts

Esta sección está disponible solo para usuarios con suscripción. Por favor, mejora tu plan para acceder a esta parte.

Mejorar ahoraVer Más Videos Relacionados

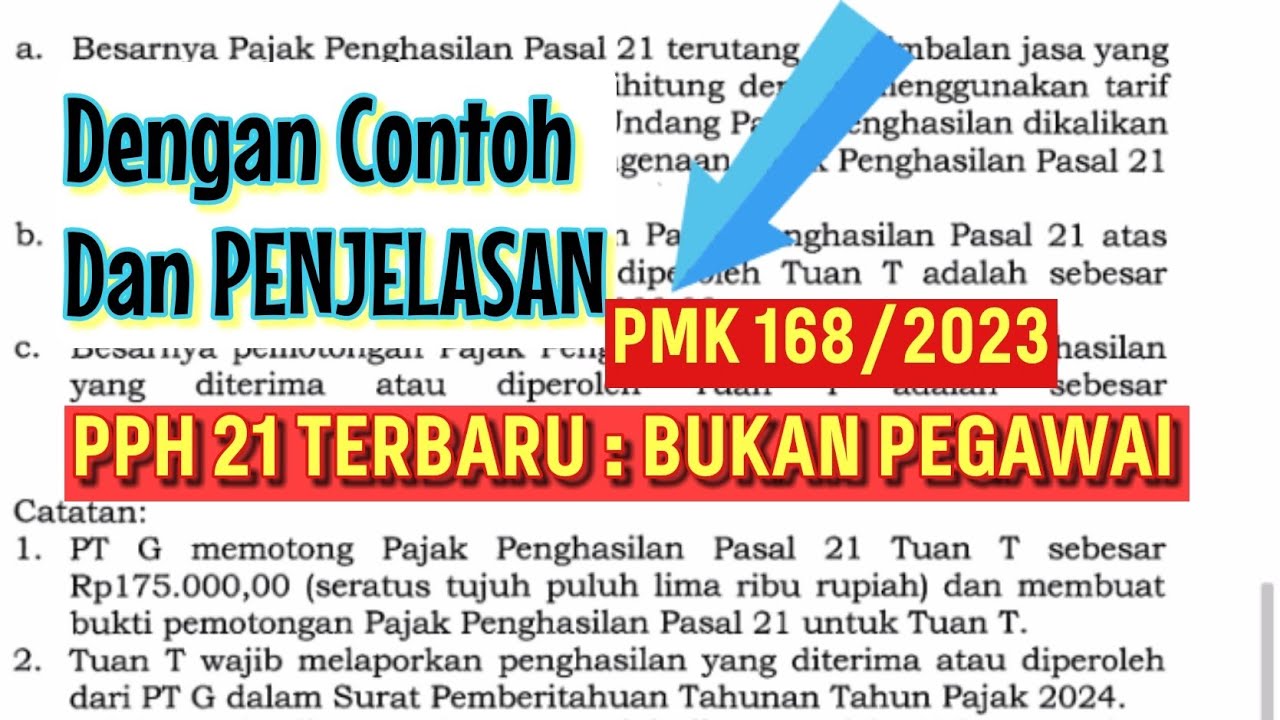

Sesuai PMK 168/2023 Berlaku Januari - Cara Hitung PPH 21 Bukan Pegawai

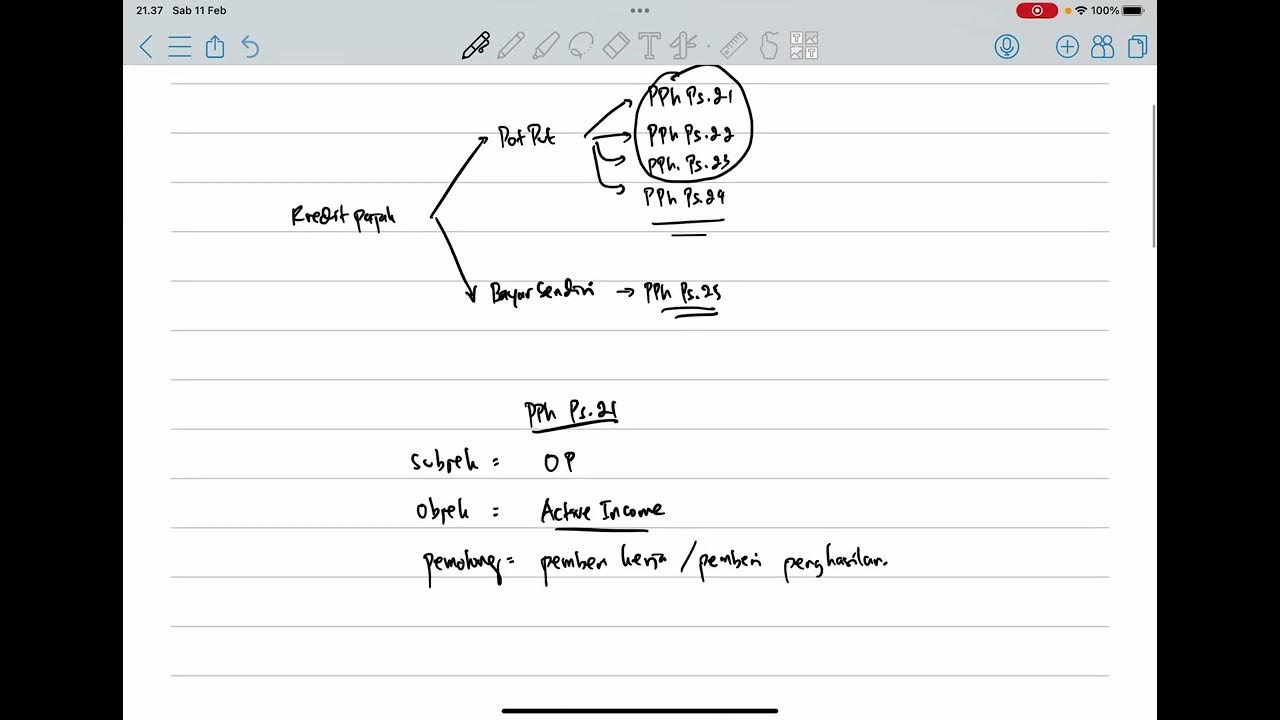

PPh Orang Pribadi (Update 2023) - 5. Kredit Pajak

Menghitung Pajak Penghasilan Pasal 21 || Materi Ekonomi Kelas XI

Aritmatika Sosial - 5 Tipe Soal Tentang Pajak | Pajak PPH dan PPN (Part 01)

Cara Menghitung Pajak Penghasilan (PPh) Badan Perusahaan Tahun Pajak 2023

Konsep dan Penghitungan PPh Pasal 23

5.0 / 5 (0 votes)