Menghitung Pajak Penghasilan Pasal 21 || Materi Ekonomi Kelas XI

Summary

TLDRIn this video, the concept of income tax (Pajak Penghasilan Pasal 21 or PPH 21) is explained in detail, focusing on how to calculate it. The script introduces the general principles of income tax and dives into the specifics of PPH 21, including its subjects and objects, such as employees, non-employees, and pensioners. Key terms like 'gross income,' 'net income,' and 'taxable income' (PKP) are clarified. Practical examples and step-by-step instructions on how to calculate taxes, including deductions and progressive tax rates, are provided to help viewers understand the process clearly.

Takeaways

- 😀 PPH 21 (Income Tax Article 21) is a tax on personal income, including salaries, wages, bonuses, and pensions.

- 😀 PPH 21 applies to both permanent and non-permanent employees, as well as independent contractors.

- 😀 The process of calculating PPH 21 involves determining **Gross Income (Penghasilan Kotor)** and subtracting allowable deductions to arrive at **Net Income (Penghasilan Neto)**.

- 😀 **Position Costs (Biaya Jabatan)** are deducted at a rate of 5% from gross income, capped at 6 million IDR per year.

- 😀 **Pension Costs (Biaya Pensiun)** are also deducted at 5% from gross income, with a cap of 2.4 million IDR per year.

- 😀 Social security contributions, like **BPJS**, are subtracted from the gross income to reduce taxable income.

- 😀 **PTKP (Non-Taxable Income)** is the amount of income that is exempt from tax, which includes personal, spouse, and dependent deductions.

- 😀 **PKP (Taxable Income)** is calculated by subtracting PTKP from the Net Income, which is the amount subject to tax.

- 😀 The progressive tax rates for PPH 21 are 5% for income up to 50 million IDR, 15% for income between 50 million and 250 million IDR, and 25% for income between 250 million and 500 million IDR.

- 😀 The tax rate increases to 30% for income exceeding 500 million IDR.

- 😀 An example of PPH 21 calculation was given for Doni, with an annual salary of 360 million IDR and a total tax liability of 43.125 million IDR after applying the progressive tax rates.

Q & A

What is PPh 21?

-PPh 21 is a personal income tax levied on individuals' earnings in Indonesia, including salaries, wages, bonuses, and other forms of compensation. It is defined under the Income Tax Law of 1984 and applies to income earned from work or services performed within Indonesia.

What are the key categories of PPh 21?

-The main categories of PPh 21 include taxes on income for permanent employees, non-permanent employees, freelancers, and retirees. It also covers income from severance pay and other job-related compensations.

How is gross income defined in the context of PPh 21?

-Gross income (penghasilan bruto) refers to the total income earned by an individual in a year before any deductions. It includes salary, bonuses, commissions, and any other forms of income received as compensation for services or work.

What is the difference between gross income and net income?

-Gross income is the total income earned before any deductions. Net income is the amount left after applying allowable deductions, such as job-related costs, pension contributions, and other eligible expenses.

What are the main allowable deductions in the calculation of PPh 21?

-Allowable deductions include job-related costs (5% of gross income, with a cap of IDR 6 million per year), pension costs (5% of gross income, capped at IDR 2.4 million per year), and social security contributions (such as BPJS).

What is PTKP, and how does it affect PPh 21 calculation?

-PTKP stands for Penghasilan Tidak Kena Pajak, which is the non-taxable income threshold. It reduces the taxable income of an individual, and if the individual's income is below this threshold, they are exempt from paying tax. PTKP increases for married individuals and those with dependents.

How is PTKP calculated for married individuals with children?

-For a married individual, PTKP includes IDR 54 million for the individual, IDR 4.5 million for the spouse, and IDR 4.5 million per child (up to three children). The total PTKP will depend on the individual's marital status and number of dependents.

What is the process for calculating PPh 21 step-by-step?

-The process involves three steps: 1) Calculate net income by subtracting allowable deductions from gross income. 2) Subtract PTKP from net income to get taxable income (PKP). 3) Apply the progressive tax rates to PKP to calculate the tax owed.

What are the applicable tax rates for PPh 21, and how are they structured?

-PPh 21 uses progressive tax rates: 5% for taxable income up to IDR 50 million, 15% for income between IDR 50 million and IDR 250 million, and 25% for income over IDR 250 million.

Can you give an example of how to calculate the PPh 21 tax liability for an individual?

-For example, if Doni has a gross salary of IDR 30 million per month, his annual gross income is IDR 360 million. After applying allowable deductions and PTKP, his taxable income (PKP) is IDR 292.66 million. The tax liability is calculated by applying the progressive tax rates, resulting in a total tax due of IDR 43,125,000 for the year.

Outlines

This section is available to paid users only. Please upgrade to access this part.

Upgrade NowMindmap

This section is available to paid users only. Please upgrade to access this part.

Upgrade NowKeywords

This section is available to paid users only. Please upgrade to access this part.

Upgrade NowHighlights

This section is available to paid users only. Please upgrade to access this part.

Upgrade NowTranscripts

This section is available to paid users only. Please upgrade to access this part.

Upgrade NowBrowse More Related Video

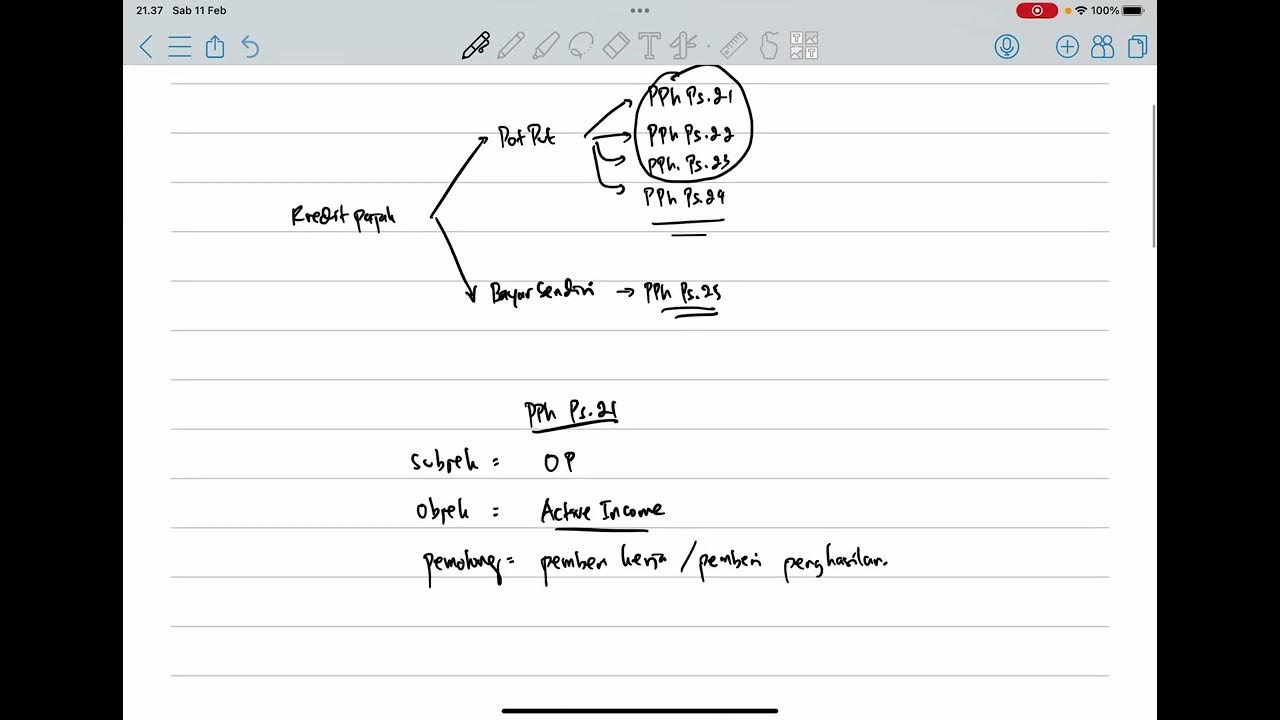

PPh Orang Pribadi (Update 2023) - 5. Kredit Pajak

MENGENAL PPH 21 LEBIH DEKAT AGAR TIDAK SALAH PAHAM DENGAN PERUSAHAAN ANDA

Aritmatika Sosial - 5 Tipe Soal Tentang Pajak | Pajak PPH dan PPN (Part 01)

Tips memahami apa saja jenis pajak perusahaan yang harus Anda laporkan

Perbedaan Pemotongan & Pemungutan Pajak || Withholding Tax #tutorialpajak

Cara Lapor SPT PPh 21 Desember Tahun 2024

5.0 / 5 (0 votes)