Audit Risk Overview

Summary

TLDRThis video explains the relationship between material misstatement risk, detection risk, and the need for substantive testing during an audit. It highlights how material misstatement is driven by inherent and control risks, with control risk being influenced by the company’s control environment. When control risk is high, auditors must set detection risk low, meaning more extensive substantive testing is needed. The video also discusses the hierarchy of audit evidence, stressing the importance of direct, external, and internal evidence in shaping the level of audit procedures. Ultimately, the decision to perform thorough substantive testing is a judgment call based on the risk assessment.

Takeaways

- 😀 Risk of material misstatement is driven by inherent risk and control risk.

- 😀 Inherent risk refers to the likelihood of material misstatement occurring, while control risk relates to the effectiveness of the company’s controls.

- 😀 If a company's controls are weak, control risk increases, making it difficult for the audit team to rely on them.

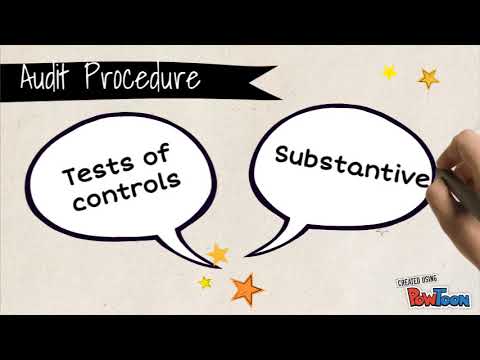

- 😀 When control risk is high, the audit team must set detection risk at a low level to perform more substantive testing.

- 😀 A low detection risk means more substantive testing is required to identify any material misstatements.

- 😀 The level of substantive tests to be performed depends on the auditor's judgment and the effectiveness of the procedures.

- 😀 The hierarchy of audit evidence is based on the level of assurance it provides, starting with direct and personal knowledge.

- 😀 Direct observation of inventory or checking for obsolescence provides the highest level of audit evidence.

- 😀 External evidence, such as confirmations from banks or accounts receivable customers, is the next best form of evidence.

- 😀 Internal evidence, such as inspecting invoices or re-performing tasks, is used when external evidence is not available.

- 😀 Inquiry, providing oral evidence, is considered the least effective form of audit evidence.

Q & A

What drives the risk of material misstatement?

-The risk of material misstatement is driven by inherent risk and control risk.

What does control risk address?

-Control risk addresses the control environment and how well the company designs and operates its controls.

How does the effectiveness of controls affect control risk?

-If the company's controls are not operating effectively, control risk will be higher, meaning the audit team cannot rely on the controls to detect or correct material misstatements.

What is the relationship between detection risk and substantive testing?

-When detection risk is low, the audit team needs to perform more substantive testing procedures to identify material misstatements.

What does setting detection risk at a low level imply for the audit team?

-Setting detection risk at a low level means the audit team believes they need to conduct more substantive testing to identify any material misstatements.

How does the auditor determine the level of substantive testing to perform?

-The auditor determines the level of substantive testing based on their judgment and the specific line item or cycle under examination.

What is the hierarchy of audit evidence?

-The hierarchy of audit evidence, in order of importance, is direct and personal knowledge, external evidence, internal evidence, and finally, inquiry-based evidence.

What is considered the highest level of audit evidence?

-The highest level of audit evidence is direct and personal knowledge, such as observing inventory or checking if something is obsolete.

Why might the auditor use external evidence like confirmations?

-External evidence, such as confirmations from banks or customers, provides independent validation and is considered reliable evidence in audits.

What happens when the auditor only has internal evidence available?

-When only internal evidence is available, the auditor will request invoices, inspect them, and re-perform tasks to gather evidence.

Outlines

Esta sección está disponible solo para usuarios con suscripción. Por favor, mejora tu plan para acceder a esta parte.

Mejorar ahoraMindmap

Esta sección está disponible solo para usuarios con suscripción. Por favor, mejora tu plan para acceder a esta parte.

Mejorar ahoraKeywords

Esta sección está disponible solo para usuarios con suscripción. Por favor, mejora tu plan para acceder a esta parte.

Mejorar ahoraHighlights

Esta sección está disponible solo para usuarios con suscripción. Por favor, mejora tu plan para acceder a esta parte.

Mejorar ahoraTranscripts

Esta sección está disponible solo para usuarios con suscripción. Por favor, mejora tu plan para acceder a esta parte.

Mejorar ahora

5.0 / 5 (0 votes)