LAPORAN KEUANGAN PEMERINTAH & LAPORAN KEUANGAN KONSOLIDASIAN - Kelompok 8 PPKP

Summary

TLDRThis video explains Indonesia's government financial reporting process, focusing on the financial statements used to account for state revenue and expenditures. It outlines key components like the Budget Realization Report (LRA), the balance sheet, cash flow statement, and operational reports, which are essential for understanding the country's fiscal health. The script also dives into the concept of consolidated financial statements, describing the steps in consolidation and the role of various financial reports in ensuring transparency and accountability within the government.

Takeaways

- 😀 LKPP (Central Government Financial Report) is a comprehensive accountability report covering the implementation of the national budget, including budget realization, balance sheet, cash flow, and notes, all compiled according to government accounting standards.

- 😀 LKPP consolidates the financial statements of various ministries and government bodies to reflect the financial position and performance of the central government as a whole.

- 😀 The LKPP was first published in 2004 as part of Indonesia's financial accountability efforts after independence.

- 😀 The report is prepared by the Directorate of Accounting and Financial Reporting under the Ministry of Finance of Indonesia.

- 😀 There are three main components in the government financial report: cash basis reports (including budget realization and budget surplus changes), accrual-based reports (including balance sheet, operational reports, equity changes, and cash flow), and notes to the financial statements.

- 😀 The operational report provides additional detail on accrual accounting, linking operational performance with other financial reports such as the balance sheet and equity change report.

- 😀 Cash flow statements track cash inflows and outflows during a specific period, categorized by operating, investing, financing, and transitional activities.

- 😀 Notes to financial statements are integral for transparency and clarity, offering detailed explanations of financial entries, policies, and other relevant data.

- 😀 Consolidated financial reports combine the financial data of various entities, like regional government agencies and local financial managers, to present a comprehensive view of a government’s financial performance.

- 😀 The consolidation process involves identifying which entities to include, preparing individual financial statements, consolidating them with adjustments (eliminating inter-entity transactions and balances), and presenting the final consolidated report, which includes several types of reports such as the budget realization and cash flow statements.

Q & A

What is the LKPP and why is it important?

-The LKPP (Laporan Keuangan Pemerintah Pusat) is the financial report of the central government of Indonesia. It serves as an accountability document for the implementation of the national budget, including revenue, expenditure, and state financing. It is crucial for ensuring transparency and accountability in government financial management.

What components make up the LKPP?

-The LKPP consists of several key components: the Budget Realization Report, Balance Sheet, Cash Flow Statement, and Notes to the Financial Statements. These components provide a comprehensive overview of the government's financial activities and position.

What does the Budget Realization Report (LRA) represent?

-The Budget Realization Report (LRA) is a component of the government's financial statements that provides a summary of the sources and uses of financial resources managed by the central or local government. It compares the budgeted amounts with actual realizations for a specific period.

What is the purpose of the Notes to the Financial Statements?

-The Notes to the Financial Statements serve to clarify and provide detailed explanations about the entries in the financial reports. These notes aim to enhance transparency and provide a better understanding of the financial data presented, such as accounting policies, detailed figures, and other relevant information.

How are accrual-based financial statements different from cash-based ones?

-Accrual-based financial statements record financial transactions when they occur, regardless of when cash is exchanged, while cash-based statements record transactions only when cash is received or paid. This distinction provides a more accurate and comprehensive picture of an entity's financial situation.

What is the role of the Government Accounting Standards (PSAP)?

-The Government Accounting Standards (PSAP) provide the framework and guidelines for preparing government financial reports in Indonesia. These standards ensure consistency, transparency, and accountability in the presentation of financial information across government entities.

What is financial statement consolidation in government accounting?

-Financial statement consolidation in government accounting refers to the process of combining the financial reports of various government entities, such as ministries, local governments, and other subordinate agencies, into a single consolidated report. This helps present a comprehensive view of the government's overall financial position and performance.

What steps are involved in the consolidation process of government financial statements?

-The consolidation process involves several steps: identifying entities to be consolidated, preparing individual financial statements, creating consolidation worksheets, eliminating inter-entity transactions and balances, merging the financial reports, and finally preparing the consolidated financial statements.

What is the purpose of the Consolidated Financial Statements?

-The purpose of the Consolidated Financial Statements is to provide a unified and comprehensive report of the financial position and performance of the entire government. It helps stakeholders, including legislators and the public, to assess the financial health and accountability of the government as a whole.

What components are included in the Consolidated Financial Statements?

-The Consolidated Financial Statements include: the Consolidated Budget Realization Report, Consolidated Changes in Fund Balances, Consolidated Balance Sheet, Consolidated Operational Report, Consolidated Statement of Changes in Equity, Consolidated Cash Flow Statement, and the Notes to the Consolidated Financial Statements.

Outlines

This section is available to paid users only. Please upgrade to access this part.

Upgrade NowMindmap

This section is available to paid users only. Please upgrade to access this part.

Upgrade NowKeywords

This section is available to paid users only. Please upgrade to access this part.

Upgrade NowHighlights

This section is available to paid users only. Please upgrade to access this part.

Upgrade NowTranscripts

This section is available to paid users only. Please upgrade to access this part.

Upgrade NowBrowse More Related Video

Akuntansi Lembaga - ELEMEN BASIS AKUNTANSI DESA

NEW FORMATS of Financial Statements of Non-Corporate Entities | Proprietors| Firm | HUF | FY 2024-25

Lecture 05: Adjusting Entries Concept. Accounting Cycle. [Fundamentals of Accounting]

Praktikum Akuntansi Instansi/Lembaga Pemerintah XI AKL (Transaksi Pendapatan dan Belanja Daerah)

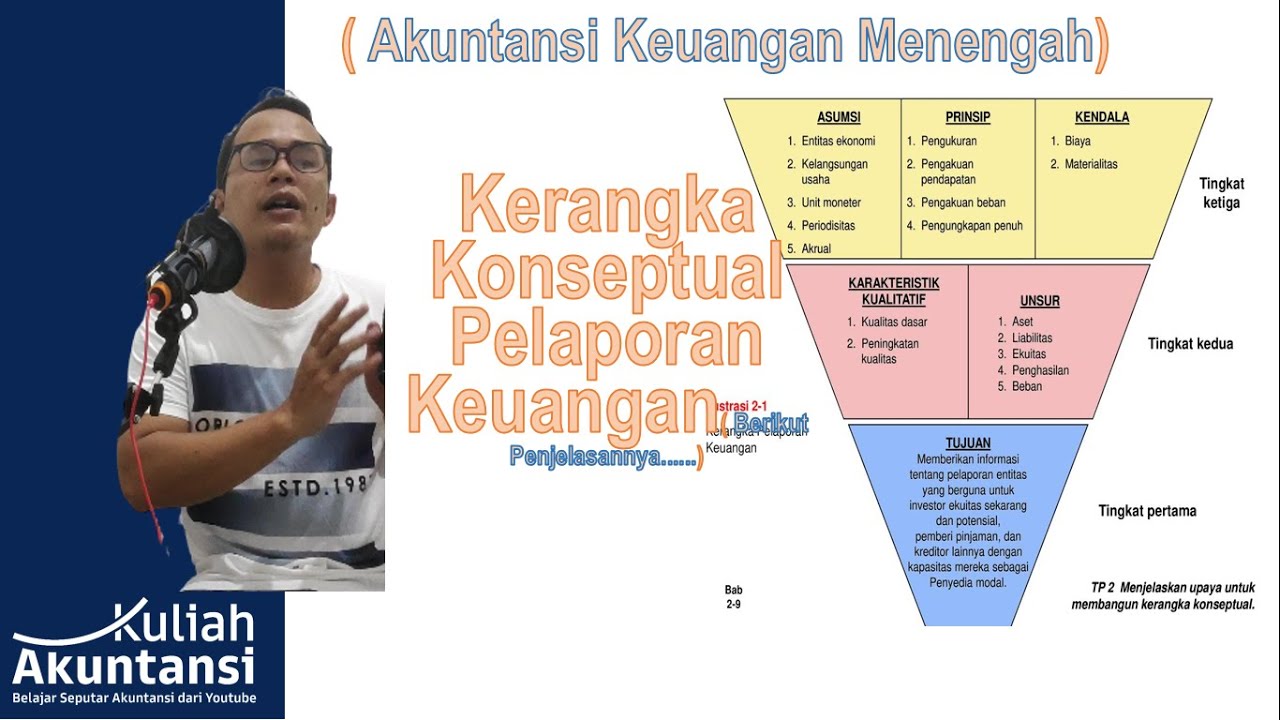

Akuntansi Keuangan Menengah : Kerangka Konseptual Pelaporan Keuangan

Power Point "Laporan Keuangan"

5.0 / 5 (0 votes)