Pengertian, Fungsi, dan Cara Membuat Jurnal Penutup | Ekonomi Kelas 12 - EDURAYA MENGAJAR

Summary

TLDRThis video explains the final stage of the accounting cycle for a service company, focusing on the closing process. It covers the creation of closing entries, which include transferring temporary account balances (such as revenues, expenses, and drawings) to permanent accounts. Key steps include closing revenue accounts, closing expense accounts, transferring profit or loss to capital, and closing the drawings account. The video also touches on the preparation of journal entries for each step, ensuring accurate financial reporting at the end of the accounting period.

Takeaways

- 😀 Understanding the final stage of the accounting cycle in service companies is essential. This stage is referred to as the closing phase, which consists of four steps.

- 😀 The four steps in the closing phase include: closing journal entries, posting to the general ledger, preparing a post-closing trial balance, and preparing reversing journal entries.

- 😀 The first task in the closing phase is creating the closing journal entry, which is done at the end of the accounting period.

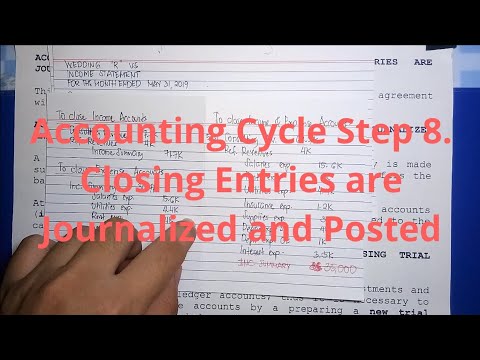

- 😀 Closing journal entries are used to transfer balances from temporary accounts to permanent accounts. Temporary accounts include revenue, expenses, profit/loss, and drawings.

- 😀 Permanent accounts, on the other hand, include assets, liabilities, and equity.

- 😀 The purpose of creating closing journal entries is to ensure the capital account reflects the correct balance at the end of the period, and to match the closing balance reported in the balance sheet.

- 😀 The first closing step involves closing the revenue accounts by debiting the revenue account and crediting the profit and loss summary account.

- 😀 After closing the revenue account, the next step is to close the expense accounts. The total expenses from the financial report are debited to the profit and loss summary and credited to the respective expense accounts.

- 😀 The third step in closing involves transferring the balance in the profit and loss summary to the capital account. This is done depending on whether the company made a profit or incurred a loss during the period.

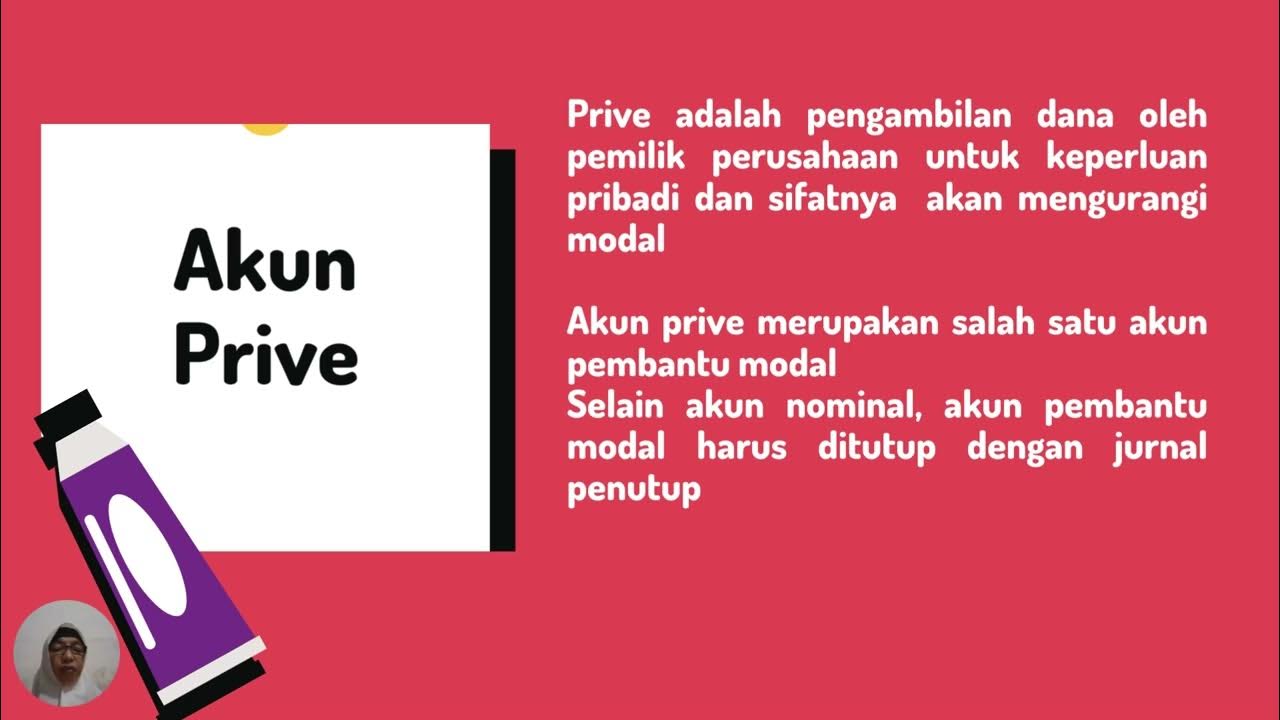

- 😀 The final step in closing involves closing the drawings account, where any balance in the drawings account is transferred to the capital account, typically through debiting the capital account and crediting the drawings account.

Q & A

What is the final stage of the accounting cycle for service companies?

-The final stage of the accounting cycle for service companies is called the closing phase, which consists of four steps: closing journal entries, closing the trial balance, post-closing trial balance, and reversal journal entries.

What is the purpose of the closing journal entries?

-The purpose of closing journal entries is to transfer temporary account balances (such as revenue and expenses) to permanent accounts, so that the temporary accounts are reset for the new period.

What are temporary accounts in accounting?

-Temporary accounts are those that accumulate transactions for a specific accounting period. These accounts include revenue, expenses, and income summary accounts.

Which accounts are affected by the closing journal entries?

-The accounts that are affected by the closing journal entries include revenue accounts, expense accounts, income summary account, and the owner’s drawing (prive) account.

Why is it necessary to close the revenue account?

-Closing the revenue account is necessary to transfer the balance to the income summary account. This ensures that the revenue balance is cleared and does not carry over into the next period.

What is the procedure for closing the revenue account?

-To close the revenue account, you debit the revenue account and credit the income summary account. The amount debited should equal the total revenue for the period.

How are expense accounts closed?

-Expense accounts are closed by debiting the income summary account and crediting the individual expense accounts. This transfers the balance of expenses to the income summary.

What happens if the company has a profit at the end of the accounting period?

-If the company has a profit, the income summary account will have a credit balance. This balance is then transferred to the owner’s equity account (capital account) via the closing journal entry.

What if the company has a loss instead of a profit?

-If the company has a loss, the income summary account will have a debit balance. The loss is then transferred to the owner’s equity account (capital account) via the closing journal entry.

How is the drawing account (prive) closed?

-The drawing account (prive) is closed by crediting the drawing account and debiting the capital (owner’s equity) account. This removes the drawing balance and updates the capital account accordingly.

Outlines

This section is available to paid users only. Please upgrade to access this part.

Upgrade NowMindmap

This section is available to paid users only. Please upgrade to access this part.

Upgrade NowKeywords

This section is available to paid users only. Please upgrade to access this part.

Upgrade NowHighlights

This section is available to paid users only. Please upgrade to access this part.

Upgrade NowTranscripts

This section is available to paid users only. Please upgrade to access this part.

Upgrade NowBrowse More Related Video

Jurnal Penutup, Buku besar setelah penutupan, Neraca saldo setelah penutupan | PART 3

Pengantar Akuntansi - Ayat Jurnal Penutup

Neng Ida Soniawati–Ekonomi XII-SMAN 1 Babakan Madang-Jurnal Penutup & Pembalik – Nov2022#pgtkjabar

Latihan Soal Pembuatan Jurnal Penutup Perusahaan Jasa Lengkap

"CARA MUDAH MEMAHAMI SIKLUS AKUNTANSI PERUSAHAAN DAGANG "

Basic Accounting | Accounting Cycle Step 8. Closing Entries are Journalized and Posted (Part 1)

5.0 / 5 (0 votes)