PAS 8 Accounting Policies, Changes in Accounting Estimates and Errors

Summary

TLDRThis session provides a concise overview of IAS 8, focusing on accounting policies, changes in accounting estimates, and the correction of prior period errors. It explains how companies select and apply accounting policies, the difference between policy changes and estimate changes, and how errors should be retrospectively or prospectively adjusted. The discussion highlights practical examples, transitional provisions, and the importance of relevance and reliability in financial reporting. Emphasis is placed on the application of standards, judgment in the absence of guidance, and ensuring financial statements remain useful, accurate, and decision-oriented for users.

Takeaways

- 😀 IAS 8 covers accounting policies, changes in accounting estimates, and correction of prior period errors.

- 😀 Accounting policies are principles, bases, conventions, rules, and practices used to prepare financial statements.

- 😀 Accounting policies are derived from PFRS, PFRS interpretations, other standard-setting bodies, and industry practices.

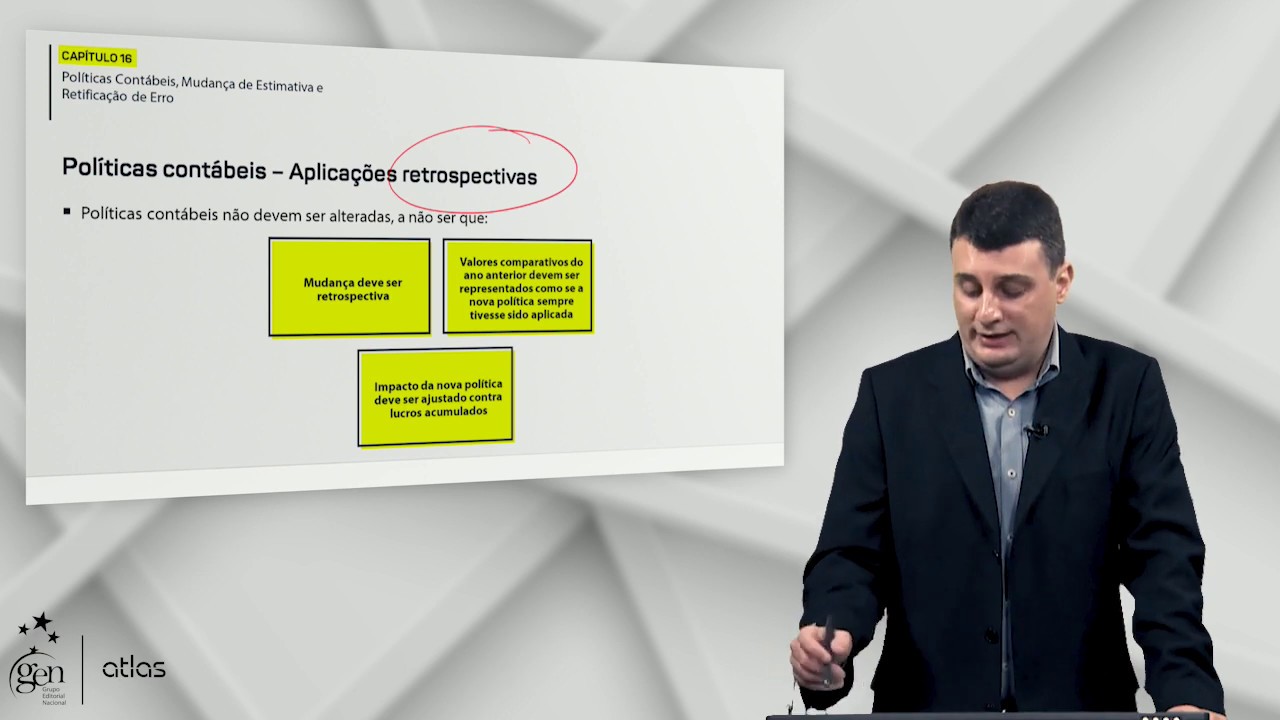

- 😀 Changes in accounting policy involve a change in measurement basis, method, or convention and may require retrospective or prospective application.

- 😀 Retrospective application adjusts past financial statements as if the new policy had always been applied, affecting the beginning balance of retained earnings.

- 😀 Prospective application applies a new policy only to current and future periods when retrospective application is impracticable.

- 😀 Changes in accounting estimates arise from new information or developments and are always applied prospectively.

- 😀 Examples of changes in estimates include adjustments to depreciation methods, useful lives, allowances, and fair value calculations.

- -

- 😀 Prior period errors are mistakes in earlier financial statements due to misapplication of principles, misinterpretation of facts, mathematical errors, or fraud.

- 😀 Correction of prior period errors generally requires retrospective restatement, adjusting prior balances as if the error never occurred.

- 😀 If it is difficult to distinguish between a change in policy and a change in estimate, it should be treated as a change in estimate.

- 😀 Changes in accounting policy must either be required by PFRS or result in more relevant and reliable information for decision-making.

Q & A

What is the main focus of IAS 8?

-IAS 8 focuses on accounting policies, changes in accounting estimates, and corrections of prior period errors, providing guidance on how to select, apply, and disclose them in financial statements.

How are accounting policies defined according to IAS 8?

-Accounting policies are specific principles, bases, conventions, rules, and practices adopted by an entity to prepare financial statements reliably and consistently.

What are the sources of accounting policies if there is no specific PFRS?

-If no specific PFRS exists, management can use similar PFRS, the Conceptual Framework, pronouncements from other standard-setting bodies, accounting literature, or established industry practices.

What distinguishes a change in accounting policy from a change in accounting estimate?

-A change in accounting policy involves changing the measurement basis or method used in accounting (except for depreciation, amortization, or depletion), while a change in estimate arises from revisions to the expected realization of assets or liabilities based on new information.

What is the retrospective application in accounting policy changes?

-Retrospective application means applying the new accounting policy to past periods as if the new policy had always been in place, adjusting the beginning balance of retained earnings accordingly.

When is prospective application used instead of retrospective application?

-Prospective application is used when retrospective application is impracticable due to high cost or infeasibility. It applies the new policy or estimate only to the current and future periods.

How should prior period errors be corrected?

-Prior period errors should be corrected using retrospective restatement, adjusting the previous financial statements as if the error never occurred. If impracticable, prospective application is used.

Can a company change an accounting policy voluntarily?

-Yes, a company can change an accounting policy voluntarily if it results in more relevant and reliable financial information, enhancing decision-making for users of financial statements.

What are examples of changes in accounting estimates?

-Examples include changes in the useful life of assets, depreciation or amortization percentages, allowances, and fair values based on market changes or observed trends.

What should a company do if it is difficult to distinguish between a policy change and an estimate change?

-If it is difficult to distinguish, IAS 8 recommends treating the change as a change in accounting estimate, as it is simpler to apply than a change in accounting policy.

Why are relevance and reliability emphasized when changing accounting policies?

-Relevance ensures that the financial information can influence users' decisions, while reliability ensures that the information faithfully represents the entity's financial position and performance. Both are key for meaningful decision-making.

How does IAS 8 apply to nonprofit organizations?

-For nonprofit organizations without specific PFRS guidance, IAS 8 allows referencing standards issued by other standard-setting bodies, such as FASB, or industry practices to develop relevant accounting policies.

Outlines

このセクションは有料ユーザー限定です。 アクセスするには、アップグレードをお願いします。

今すぐアップグレードMindmap

このセクションは有料ユーザー限定です。 アクセスするには、アップグレードをお願いします。

今すぐアップグレードKeywords

このセクションは有料ユーザー限定です。 アクセスするには、アップグレードをお願いします。

今すぐアップグレードHighlights

このセクションは有料ユーザー限定です。 アクセスするには、アップグレードをお願いします。

今すぐアップグレードTranscripts

このセクションは有料ユーザー限定です。 アクセスするには、アップグレードをお願いします。

今すぐアップグレード関連動画をさらに表示

[MEET 10] AKUNTANSI EKUITAS & PELAPORAN KEUANGAN - PERUBAHAN AKUNTANSI & ANALISIS KESALAHAN #2

[MEET 9] AKUNTANSI EKUITAS & PELAPORAN KEUANGAN - PERUBAHAN AKUNTANSI & ANALISIS KESALAHAN

Políticas Contábeis, Mudança de Estimativa e Retificação de Erro | Contabilidade Avançada | 2ª ed.

Neng Ida Soniawati–Ekonomi XII-SMAN 1 Babakan Madang-Jurnal Penutup & Pembalik – Nov2022#pgtkjabar

Summary of IAS 40 Investment Property - applies in 2024

IAS 37 Provisions, Contingent Liabilities and Contingent Assets summary - applies in 2024

5.0 / 5 (0 votes)