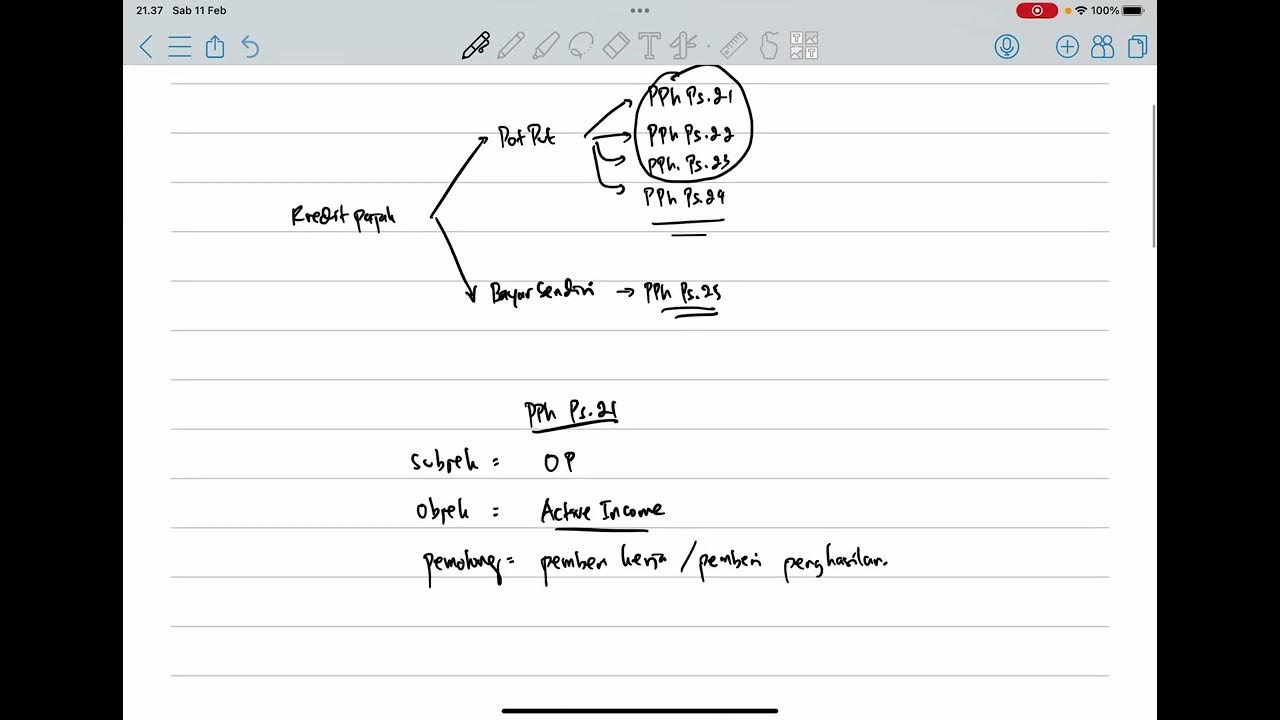

PPH Orang Pribadi (Update 2023) - 2. Objek Pajak

Summary

TLDRThis video explains the process of calculating personal income tax (PPH) in Indonesia, covering key concepts such as gross income, tax allowances, and deductions. It breaks down the tax calculation for different income types: business income, freelance income, employee income, and model income. The video also highlights distinctions between non-final, final, and non-taxable income, providing insights into how each is taxed. Additionally, it discusses special rules for employees and the taxation of various other income types like royalties and currency exchange gains, making it a comprehensive guide to understanding Indonesian income tax.

Takeaways

- 😀 To calculate Personal Income Tax (PPH) for individuals, start with gross income, subtract costs, then deduct personal exemptions (PTKP) to determine taxable income. Apply the tax rate and deduct any tax credits to find the tax payable or refundable.

- 😀 Income can be divided into three categories: non-final income, final income, and non-taxable income, each treated differently under the tax law.

- 😀 Non-final income is subject to regular tax calculations, while final income has a simplified tax calculation method, and non-taxable income is not included in the PPH calculations.

- 😀 Income from business or freelance work can be categorized into two groups: businesses with turnover below 4.8 billion IDR, which qualify for a final tax rate of 0.5%, and businesses with turnover above that, which are subject to normal tax calculations.

- 😀 Freelancers or those with a turnover below 4.8 billion IDR who do not maintain proper accounting records will calculate net income based on gross income multiplied by a standard rate (NPPN).

- 😀 Businesses or freelancers with turnover above 4.8 billion IDR must calculate net income by subtracting expenses from gross income using regular accounting methods.

- 😀 For employees, net income is calculated by subtracting allowable expenses like salaries, benefits, insurance premiums, and pension contributions from gross income.

- 😀 Employee benefits, including nature benefits (e.g., goods provided by the employer), can be considered as taxable income, while certain insurance contributions (e.g., BPJS Ketenagakerjaan) are deductible.

- 😀 Dividends are considered non-taxable income for individuals if reinvested in Indonesia, otherwise, they are treated as final income subject to tax.

- 😀 Interest income from loans and royalties are taxable, whereas interest from deposits and savings accounts is excluded from taxable income.

- 😀 Other income types, such as currency exchange differences or asset sales, are taxable and should be calculated based on either the gain or loss from the transaction, with specific rules based on whether proper accounting records are kept.

Q & A

What is the first step in calculating PPH for individuals?

-The first step in calculating PPH (Pajak Penghasilan) for individuals is to start with gross income, subtract any allowable expenses, and then calculate the taxable income. This is followed by applying the tax rates according to Article 17, and deducting any tax credits to determine the final amount of tax due, or if there is an overpayment or underpayment.

How are income sources categorized for tax calculation in Indonesia?

-Income sources in Indonesia are categorized into three types: non-final income, final income, and non-taxable income. Only non-final income is included in the PPH calculation, while final income and non-taxable income are excluded.

What distinguishes final income from non-final income in tax calculations?

-Final income is not included in the PPH calculation, while non-final income is. Non-final income requires a more complex calculation based on gross income, deductions, and applicable tax rates, while final income is generally subject to a flat rate tax or is not taxed at all.

What is the tax treatment for businesses with an annual turnover of less than IDR 4.8 billion?

-For businesses with an annual turnover of less than IDR 4.8 billion, they are subject to a final tax rate of 0.5% on their turnover, governed by the PP 23 regulation. They do not need to conduct detailed bookkeeping for tax purposes.

How is taxable income calculated for businesses with turnover greater than IDR 4.8 billion?

-For businesses with turnover greater than IDR 4.8 billion, the taxable income is calculated by subtracting allowable expenses from gross income, resulting in net income. This requires more detailed bookkeeping compared to businesses with lower turnover.

What tax calculation method applies to individuals engaged in freelance work or independent professions?

-For individuals in freelance work or independent professions, if their turnover is less than IDR 4.8 billion per year and they do not maintain proper books, the taxable income is calculated using a fixed percentage (NPPN) of their gross income. If they exceed this turnover or maintain proper books, they must calculate their taxable income using the standard method of gross income minus expenses.

What types of employee benefits are considered taxable income for employees?

-Employee benefits that are considered taxable income include salaries, bonuses, allowances, and natura (such as food or housing benefits). However, contributions made by employers to certain employee benefits like BPJS Ketenagakerjaan (social security) are not taxable.

What is the tax treatment for dividends received by individuals in Indonesia?

-Dividends received by individuals in Indonesia are generally considered non-taxable income, provided they are reinvested within Indonesia. If the dividend is not reinvested locally, it is subject to a final tax.

How are rental income and royalties taxed under Indonesian tax law?

-Rental income and royalties are taxable under Indonesian tax law, with rental income being taxable unless it is derived from land and building leases, which are subject to a final tax. Royalties from patents and other intellectual property are also taxable as income.

How is income from asset sales treated for tax purposes if an individual maintains proper bookkeeping?

-For individuals who maintain proper bookkeeping, income from asset sales is calculated by subtracting the asset's book value from the sale price. If they do not maintain proper books, the taxable income is calculated as the difference between the sale price and the purchase price, without accounting for depreciation.

Outlines

此内容仅限付费用户访问。 请升级后访问。

立即升级Mindmap

此内容仅限付费用户访问。 请升级后访问。

立即升级Keywords

此内容仅限付费用户访问。 请升级后访问。

立即升级Highlights

此内容仅限付费用户访问。 请升级后访问。

立即升级Transcripts

此内容仅限付费用户访问。 请升级后访问。

立即升级浏览更多相关视频

Aritmatika Sosial - 5 Tipe Soal Tentang Pajak | Pajak PPH dan PPN (Part 01)

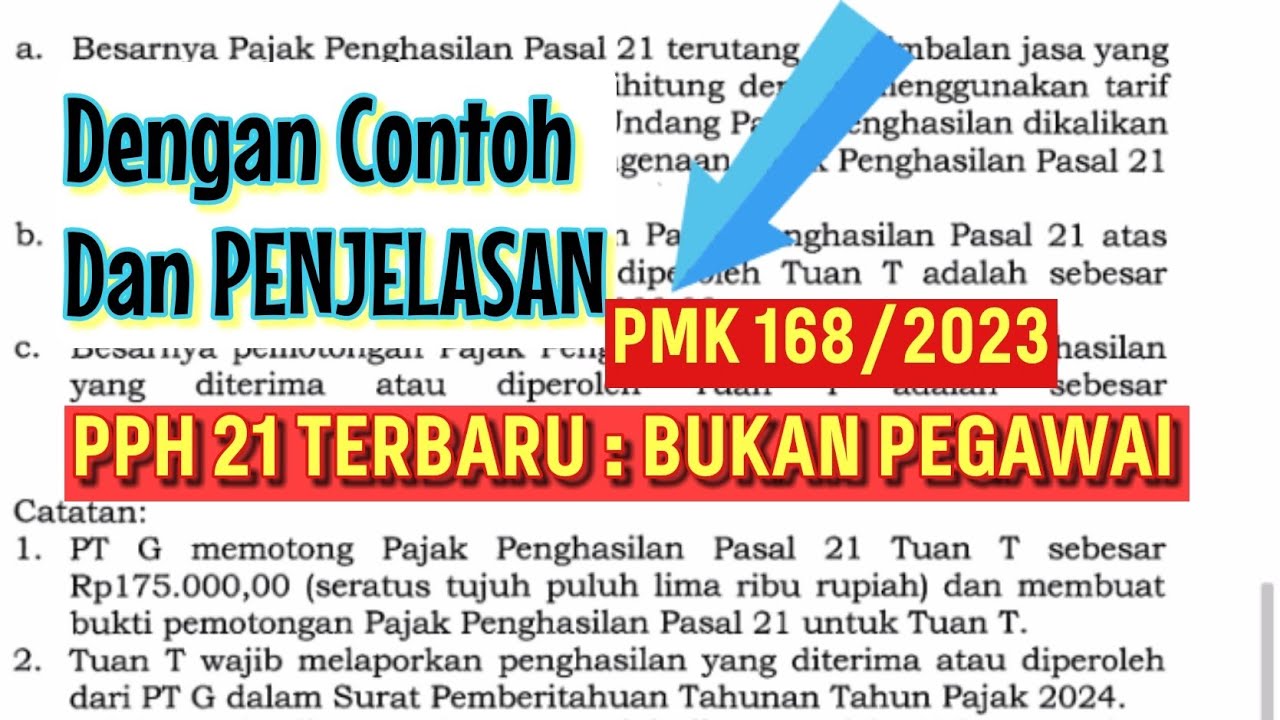

Sesuai PMK 168/2023 Berlaku Januari - Cara Hitung PPH 21 Bukan Pegawai

Menghitung Pajak Penghasilan Pasal 21 || Materi Ekonomi Kelas XI

PPh Orang Pribadi (Update 2023) - 5. Kredit Pajak

PART 10 | TUTORIAL E-BUPOT 21/26 | Perbedaan Perhitungan PPh Pasal 21 Nett, Gross, dan Gross Up

Menghitung Pajak Penghasilan - PPh

5.0 / 5 (0 votes)