MENTORING - Akuntansi Keuangan Menengah 1 (Semester 2)

Summary

TLDRThis video discusses the key concepts of financial reporting frameworks, emphasizing the importance of conceptual frameworks in guiding the preparation and presentation of financial statements. It covers objectives like providing useful financial information to stakeholders, and explains qualitative characteristics, such as relevance, neutrality, and comparability. The video also explores the elements of financial reports, including assets, liabilities, and equity. Additionally, it delves into accounting principles like revenue recognition and full disclosure, and concludes with practical examples of financial statement adjustments and reconciliations, offering a comprehensive view of the financial reporting process.

Takeaways

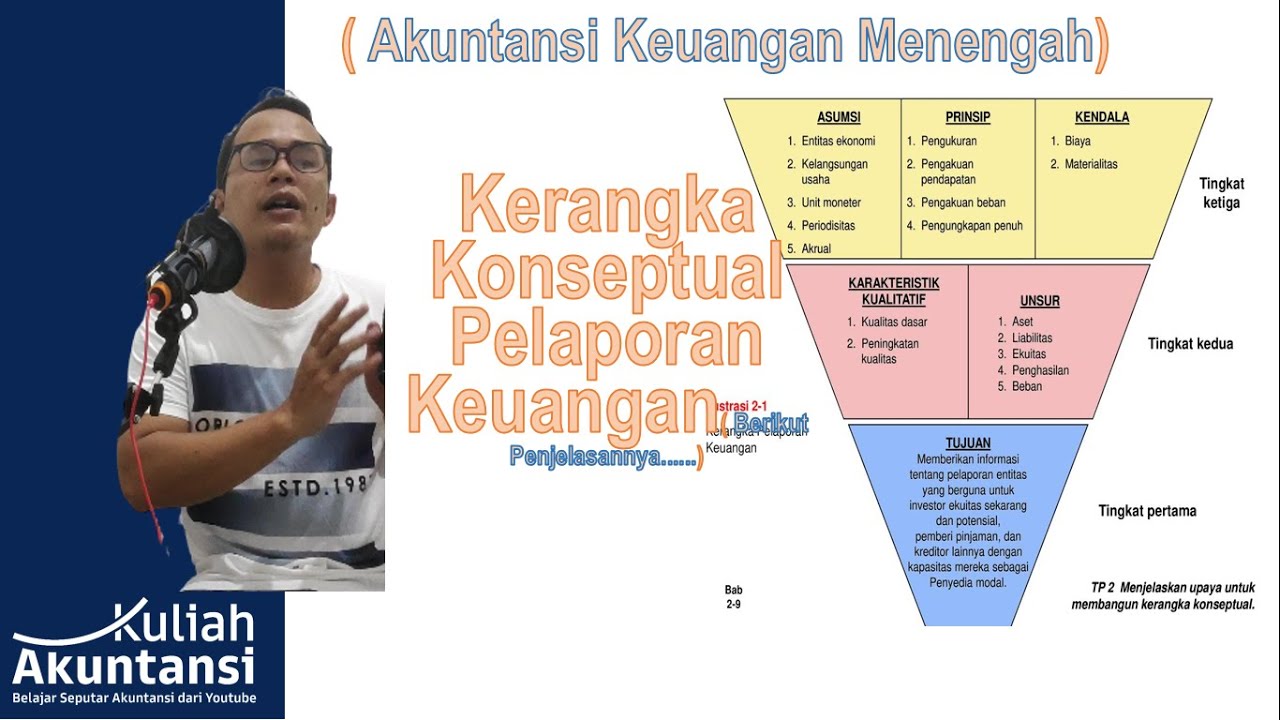

- 😀 Framework for financial reporting is a conceptual structure used to guide the preparation and presentation of financial reports.

- 😀 The primary objective of financial reports is to provide useful information about a company's financial condition to investors, lenders, and creditors.

- 😀 Key qualitative characteristics of financial reports include relevance, reliability, comparability, verifiability, timeliness, and understandability.

- 😀 Elements of financial reports include assets, liabilities, equity, revenues, and expenses, which provide a clear view of a company's financial position.

- 😀 The recognition, measurement, and disclosure in financial reports are governed by principles like cost, fair value, revenue recognition, and full disclosure.

- 😀 The fundamental accounting assumption includes the economic entity assumption, going concern assumption, monetary unit assumption, and accrual basis.

- 😀 A financial report's accuracy is influenced by the cost-benefit principle, where the benefit of the information should outweigh its cost.

- 😀 The income statement provides essential data such as gross profit, operating expenses, non-operating expenses, and net profit, which contribute to equity changes.

- 😀 In financial reporting, adjustments such as correcting errors in cash entries or recognizing transactions like bank fees and receivables must be properly accounted for.

- 😀 The reconciliation of bank statements helps match the balance reported by the bank with the book balance of the company, ensuring all transactions are reflected correctly.

- 😀 In managing accounts receivable, businesses must account for aged receivables and estimate potential losses based on aging analysis and historical data.

Q & A

What is the purpose of the Framework for Financial Reporting?

-The Framework for Financial Reporting is a conceptual framework used to guide the process of preparing and presenting financial reports. It helps ensure that financial statements are made according to standard principles and provide useful information to investors, creditors, and other stakeholders.

What is the first level objective of financial reporting?

-The first-level objective of financial reporting is to provide information about the financial condition of a company. This information is used by investors, lenders, and creditors to make decisions, such as whether to buy, sell, or hold investments, or to extend credit to the company.

What are the fundamental qualitative characteristics of financial information?

-The fundamental qualitative characteristics of financial information are relevance and faithful representation. Relevance means the information should help in predicting future outcomes and confirming past decisions. Faithful representation means the information should be complete, neutral, and free from error.

What does the characteristic of 'comparability' mean in financial reporting?

-Comparability means that financial reports should allow users to compare financial data across different periods or companies in the same industry. This helps in assessing trends and making informed decisions.

What are the key elements of financial statements?

-The key elements of financial statements include assets, liabilities, equity, revenue, and expenses. Assets represent what the company owns, liabilities represent its obligations, equity is the owners' residual interest, revenue represents income from business operations, and expenses are costs incurred to run the business.

What does the term 'going concern' refer to in financial reporting?

-The term 'going concern' refers to the assumption that a company will continue its operations in the foreseeable future, and will not be liquidated or forced to halt operations in the near term.

What is the difference between cost and fair value measurement in financial reporting?

-Cost measurement records assets based on their historical purchase price, while fair value measurement records assets at their current market value. Fair value reflects how much the asset could be sold for in an open market.

How does the accrual basis of accounting affect financial reporting?

-Under the accrual basis of accounting, transactions are recorded when they occur, not when cash is received or paid. This method provides a more accurate representation of a company’s financial performance and position over time.

What is the role of 'full disclosure' in financial reporting?

-Full disclosure means that all relevant information that could influence the decisions of users of financial statements must be disclosed. This includes both financial and non-financial information that could affect the decision-making process.

What is the purpose of bank reconciliation in accounting?

-Bank reconciliation is a process of matching the balance in the company’s books with the balance in the bank statement. It ensures that both records are accurate and identifies any discrepancies, such as unrecorded transactions or errors.

Outlines

This section is available to paid users only. Please upgrade to access this part.

Upgrade NowMindmap

This section is available to paid users only. Please upgrade to access this part.

Upgrade NowKeywords

This section is available to paid users only. Please upgrade to access this part.

Upgrade NowHighlights

This section is available to paid users only. Please upgrade to access this part.

Upgrade NowTranscripts

This section is available to paid users only. Please upgrade to access this part.

Upgrade NowBrowse More Related Video

Conceptual Framework for Financial Reporting 2018 (IFRS Framework) - still applies in 2024

AKM I.1. Kerangka Konseptual Pelaporan Keuangan

Chapter 1, Part 1 - Introduction to Accounting

REGULASI : STANDAR AKUNTANSI PEMERINTAH

Akuntansi Keuangan Menengah : Kerangka Konseptual Pelaporan Keuangan

Dasar Akuntansi Pajak

5.0 / 5 (0 votes)