SBR Topic Explainer: Solving questions using the conceptual framework

Summary

TLDRThis video script offers an in-depth exploration of the conceptual framework for financial reporting, led by expert tutor Alina Karim. It covers the framework's eight chapters, emphasizing the purpose of financial reporting, the importance of qualitative characteristics for useful financial information, and the fundamental elements of financial statements. The tutorial clarifies the distinction between recognition and measurement in accounting, and the significance of historical and current value measurement bases. Alina encourages students to practice applying these concepts to various accounting standards for exam success.

Takeaways

- 📚 The Conceptual Framework is a comprehensive guidance document for financial reporting, broken down into eight chapters, each addressing different aspects of financial statement preparation.

- 🎯 The primary purpose of the Conceptual Framework is to provide a basis for the development of accounting standards, ensuring consistency and addressing issues when no specific standard applies.

- 🤝 It focuses on the needs of decision-makers who will use the financial information, emphasizing the importance of the primary users and stakeholders in financial reporting.

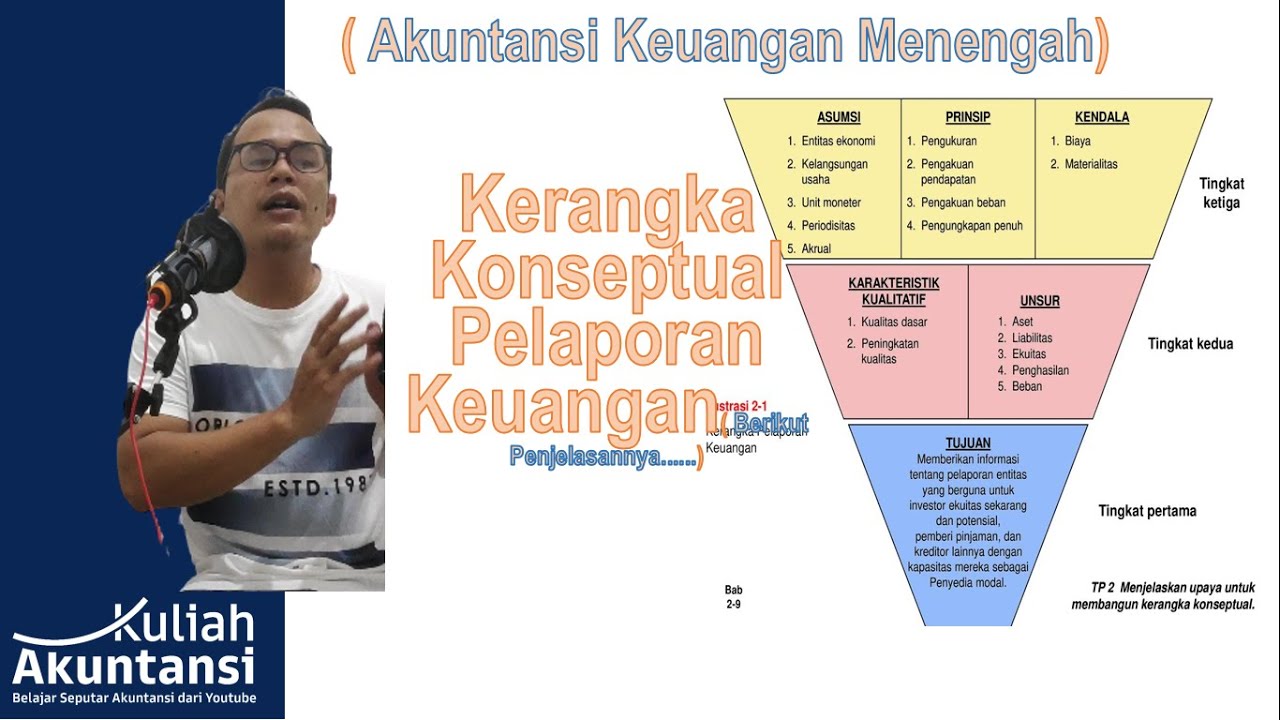

- 💡 The framework outlines the objective of general purpose financial statements, which is to provide information about the amount, timing, and uncertainty of future net cash flows.

- 🔍 Qualitative characteristics of useful financial information are crucial, with relevance and faithful representation being fundamental, while comparability, verifiability, timeliness, and understandability enhance the usefulness of the information.

- 📈 The framework defines five elements of financial statements: assets, liabilities, equity, income, and expenses, which form the basis for financial reporting globally.

- 🔑 Recognition and derecognition criteria are pivotal; recognition pertains to when and how an item is recorded in financial statements, while derecognition involves the removal of an item.

- 📊 Measurement bases in financial reporting are categorized into historical and current values, with each having its specific application depending on the context and standard.

- 🏢 The framework applies the concept of substance over form, emphasizing the underlying economic reality rather than legal form, which influences how items like leases and consolidations are reported.

- 📝 The Conceptual Framework is a foundational document for all accounting standards, guiding the interpretation and application of specific standards in various scenarios.

- 📘 For exam preparation, understanding and applying the principles from the Conceptual Framework can lead to higher marks, especially when explaining the rationale behind accounting treatments.

Q & A

What is the purpose of the conceptual framework for financial reporting?

-The purpose of the conceptual framework for financial reporting is to provide a basis for the development of International Financial Reporting Standards (IFRS), ensure consistency across these standards, and guide the selection of appropriate accounting treatments in the absence of a specific standard for a particular item.

Why is the conceptual framework not a standard itself?

-The conceptual framework is not a standard itself because it serves as a guidance document for the preparation of financial statements and for the development of IFRS, rather than prescribing specific accounting rules or transactions.

What are the main areas covered in the conceptual framework?

-The main areas covered in the conceptual framework include the objective of general purpose financial reporting, qualitative characteristics of useful financial information, elements of financial statements, recognition and derecognition criteria, measurement criteria, presentation and disclosure, and concepts of capital and capital maintenance.

What is the definition of 'assets' according to the conceptual framework?

-According to the conceptual framework, an 'asset' is a present economic resource controlled by an entity as a result of past events.

How does the conceptual framework define 'liabilities'?

-The conceptual framework defines 'liabilities' as present obligations of the entity to transfer an economic resource as a result of past events.

What are the two fundamental qualitative characteristics of financial information?

-The two fundamental qualitative characteristics of financial information are relevance and faithful representation.

What is the importance of 'relevance' in the context of financial information?

-Relevance is important because it means the financial information must be capable of making a difference in the decisions made by users, either through its predictive value or by confirming or correcting prior evaluations.

What does 'faithful representation' mean in the context of financial statements?

-'Faithful representation' means that the financial statements should depict what is actually happening in the business, free from bias, error, and omission.

How does the conceptual framework address the concept of 'materiality'?

-The conceptual framework addresses materiality by stating that all material information should be included in the financial statements, as it is relevant to the decision-making needs of the users.

What are the enhancing qualitative characteristics of financial information?

-The enhancing qualitative characteristics of financial information are comparability, verifiability, timeliness, and understandability.

Why is 'comparability' important in financial reporting?

-Comparability is important in financial reporting because it allows users to compare the financial information of different entities or the same entity over time, ensuring consistency in the application of accounting policies.

What is the role of 'verifiability' in the context of financial statements?

-'Verifiability' ensures that the financial information is credible and reliable, meaning that different people should reach the same conclusion when interpreting the information.

How does 'timeliness' contribute to the usefulness of financial information?

-'Timeliness' contributes to the usefulness of financial information by ensuring that the information reaches the users in time to influence their decision-making effectively.

What does 'understandability' mean in the context of presenting financial information?

-'Understandability' means that the financial information should be clear, concise, and presented in a manner that is easy for users to comprehend.

What is the difference between 'recognition' and 'measurement' in financial reporting?

-Recognition refers to the process of incorporating an item into the financial statements, determining when and how to record it, while measurement is about determining the amount at which the item should be recognized.

What are the two main categories of measurement bases mentioned in the conceptual framework?

-The two main categories of measurement bases mentioned in the conceptual framework are historical cost and current value.

How does the conceptual framework guide the recognition of revenue?

-The conceptual framework guides the recognition of revenue by stating that it should only be recognized when it meets the definition of an asset, liability, income, or expense, and when it is relevant and faithfully represents the underlying transaction or event.

What is the importance of the conceptual framework in the context of an exam?

-The importance of the conceptual framework in the context of an exam is that it forms the basis for all accounting standards, and understanding it can help in explaining the principles behind accounting treatments, which can lead to extra marks for conceptual understanding in exam answers.

Outlines

This section is available to paid users only. Please upgrade to access this part.

Upgrade NowMindmap

This section is available to paid users only. Please upgrade to access this part.

Upgrade NowKeywords

This section is available to paid users only. Please upgrade to access this part.

Upgrade NowHighlights

This section is available to paid users only. Please upgrade to access this part.

Upgrade NowTranscripts

This section is available to paid users only. Please upgrade to access this part.

Upgrade NowBrowse More Related Video

Conceptual Framework for Financial Reporting 2018 (IFRS Framework) - still applies in 2024

Akuntansi Keuangan Menengah : Kerangka Konseptual Pelaporan Keuangan

AKM I.1. Kerangka Konseptual Pelaporan Keuangan

MANAJEMEN MUTU 01 - Sejarah, Pengertian, Kriteria dan Karakteristik Mutu - Bowo Irianto

Akuntansi Lembaga Keuangan Syariah : Kerangka Dasar Penyusunan Laporan Keuangan Syariah

آموزش پرایس اکشن ( قسمت 1 ) | شناسایی ترند قوی و ضعیف

5.0 / 5 (0 votes)