Perilaku Biaya | Wahyu Pramesti, S.E., M.Si,. Ak., C.A

Summary

TLDRIn this lecture on management accounting, Wahyu Pramesti explains cost behavior, focusing on variable, fixed, and mixed costs. Variable costs change proportionally with the level of activity, while fixed costs remain constant regardless of activity. Mixed costs combine both fixed and variable elements. The lecture covers the concept of activity bases (cost drivers), relevant ranges, and time horizons. Through graphical representations, Pramesti demonstrates how these costs behave as activity levels change. The session provides essential insights into understanding cost behavior for effective management accounting.

Takeaways

- 😀 Behavior of costs refers to how costs vary with changes in business activity.

- 😀 The main types of cost behavior are variable costs, fixed costs, and mixed costs.

- 😀 Variable costs change proportionally with the level of business activity, such as raw material costs.

- 😀 Fixed costs remain constant up to a certain activity level and then may increase in steps when a new capacity level is reached.

- 😀 Mixed costs combine elements of both variable and fixed costs.

- 😀 The activity base is a measure that causes costs to vary, such as direct labor hours, machine hours, or units produced.

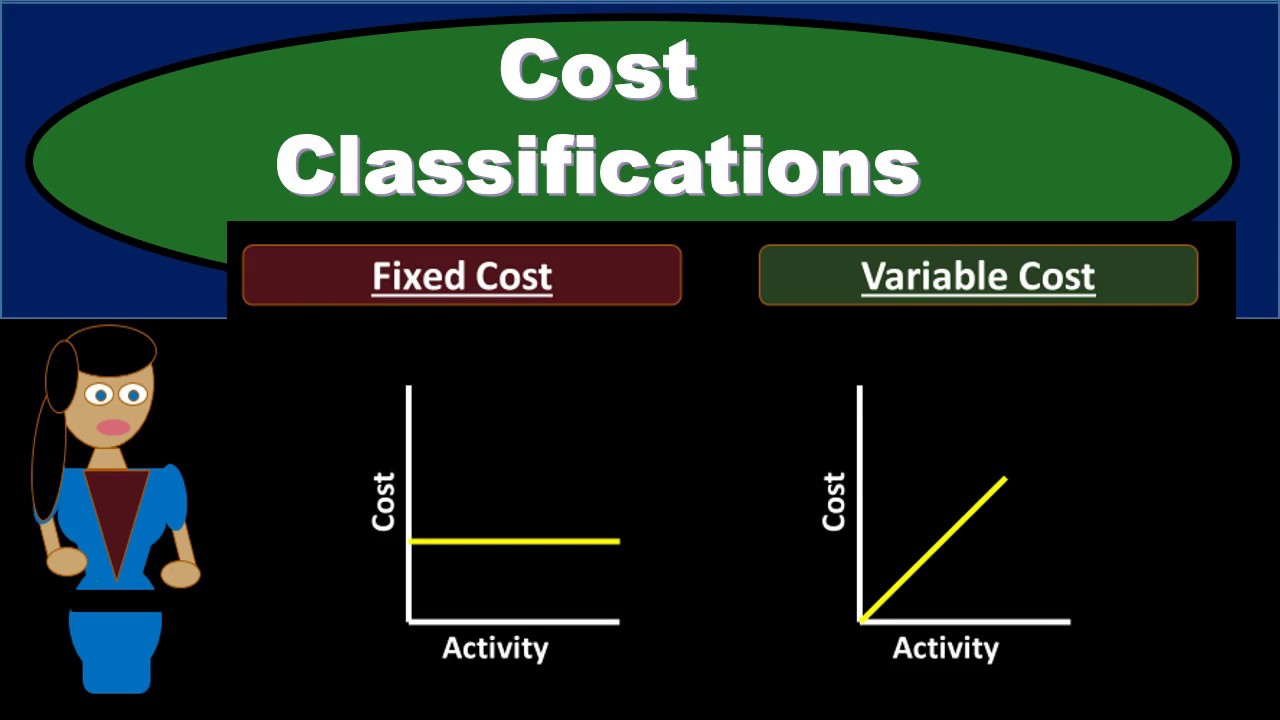

- 😀 Variable costs are illustrated on a graph where the total cost increases in a straight line as the number of units produced rises.

- 😀 Fixed costs are represented as a horizontal line on a graph, showing no change in total cost until a certain activity level is exceeded, after which they may jump to a new fixed level.

- 😀 Mixed costs can be represented by combining both variable and fixed cost components on a graph, showing an initial fixed cost and a slope for variable costs.

- 😀 The relevance of classifying costs into variable or fixed depends on the relevant range, which is the level of activity within which the behavior of costs remains consistent.

- 😀 In the short term, costs are classified as either variable or fixed, but over a longer time horizon, even fixed costs may behave like variable costs.

Q & A

What is the definition of cost behavior?

-Cost behavior refers to how the total cost changes with variations in the level of business activity. It describes the relationship between cost and activity levels.

What are the three main types of cost behavior?

-The three main types of cost behavior are variable costs, fixed costs, and mixed costs.

How does the basis of activity influence cost classification?

-The classification of a cost as either variable or fixed depends on its basis of activity, which is the factor that causes the cost to vary. Examples include direct labor hours, machine hours, and number of units produced.

What are variable costs, and how do they behave?

-Variable costs are costs that change in total in direct proportion to changes in the level of activity. The cost per unit remains constant, but the total cost increases as the level of activity increases.

Can you describe the graphical representation of variable costs?

-In a graph, the total variable cost is plotted on the Y-axis against the number of units produced on the X-axis. The graph starts at the origin (0,0) and increases proportionally with the level of activity, forming a straight line.

What are fixed costs, and how do they behave?

-Fixed costs remain constant in total regardless of changes in the level of activity. These costs do not change with production levels up to a certain point, after which they might change due to capacity limits or other factors.

How are fixed costs represented in a graph?

-In a graph, fixed costs appear as a horizontal line at a constant level, regardless of changes in the activity level. The line remains parallel to the X-axis, indicating that the total cost does not change with activity, until it might increase due to factors such as capacity limits.

What are mixed costs?

-Mixed costs combine elements of both variable and fixed costs. They have a fixed component that remains constant and a variable component that changes with the level of activity.

How are mixed costs represented in a graph?

-Mixed costs are represented by a graph that starts at the fixed cost level on the Y-axis and then increases proportionally as the activity level rises, combining the characteristics of both fixed and variable cost graphs.

What is the concept of relevant range in cost behavior?

-The relevant range refers to the range of activity levels within which the cost behavior assumptions are valid. Costs are classified as variable or fixed only within this relevant range; beyond this range, costs may change due to different factors.

Outlines

This section is available to paid users only. Please upgrade to access this part.

Upgrade NowMindmap

This section is available to paid users only. Please upgrade to access this part.

Upgrade NowKeywords

This section is available to paid users only. Please upgrade to access this part.

Upgrade NowHighlights

This section is available to paid users only. Please upgrade to access this part.

Upgrade NowTranscripts

This section is available to paid users only. Please upgrade to access this part.

Upgrade NowBrowse More Related Video

Akuntansi Manajemen Pertemuan 6 Perilaku Biaya Aktivitas

ANALISIS PERILAKU BIAYA

[MEET 2] AKUNTANSI MANAJEMEN - KONSEP & PERILAKU BIAYA

Akuntansi Biaya Bab 3: Analisis Perilaku Biaya

2023 Meet 3 Akuntasi Manajemen : Konsep dan Prilaku Biaya

Cost Classifications - Managerial Accounting- Fixed Costs Variable Costs Direct & Indirect Costs

5.0 / 5 (0 votes)