2023 Meet 3 Akuntasi Manajemen : Konsep dan Prilaku Biaya

Summary

TLDRThis lecture on Management Accounting focuses on cost accounting, defining key terms such as costs, expenses, and revenues. It explores various cost classifications, including direct, indirect, fixed, and variable costs. The lecture also discusses the relationship between cost behavior and production functions, highlighting how costs are managed for pricing, control, and decision-making. Methods like direct tracing, cost drivers, and allocation are explained. The goal of cost accounting is to provide relevant financial information for both internal management and external reporting, ultimately aiding in strategic planning and organizational control.

Takeaways

- 😀 Accounting for costs involves recording, classifying, summarizing, and presenting costs related to the production or sale of goods and services.

- 😀 Costs are defined as sacrifices of economic resources, measured in money, to acquire goods or services that provide current or future benefits.

- 😀 Expenses occur when costs are utilized to generate revenue, whereas unused costs are classified as assets.

- 😀 The goal of cost accounting is to provide cost information for various purposes such as pricing, cost control, and decision-making.

- 😀 Cost accounting involves creating reports for internal use (management) and external use (investors, stakeholders).

- 😀 Costs can be classified based on their object of expenditure, primary function within the company, relationship to the funded object, behavior with respect to activity volume, and time benefits.

- 😀 Direct costs can be traced to specific objects, while indirect costs cannot be easily traced to a particular object.

- 😀 There are three primary functions in a manufacturing company: production, marketing, and administration, each involving different types of costs such as production costs, marketing costs, and administrative costs.

- 😀 Variable costs change in total with the level of activity, while fixed costs remain unchanged, regardless of activity levels. Mixed costs have both variable and fixed cost characteristics.

- 😀 Costs can be categorized by the type of activity they support: raw material costs, direct labor costs, and manufacturing overhead costs.

- 😀 The cost allocation method includes direct tracing, cost driver tracing, and cost allocation, depending on the relationship between the cost and the cost object.

Q & A

What is the primary goal of cost accounting?

-The primary goal of cost accounting is to record, classify, summarize, and present the costs related to the creation and sale of goods or services. It helps businesses understand their expenses and make informed financial decisions.

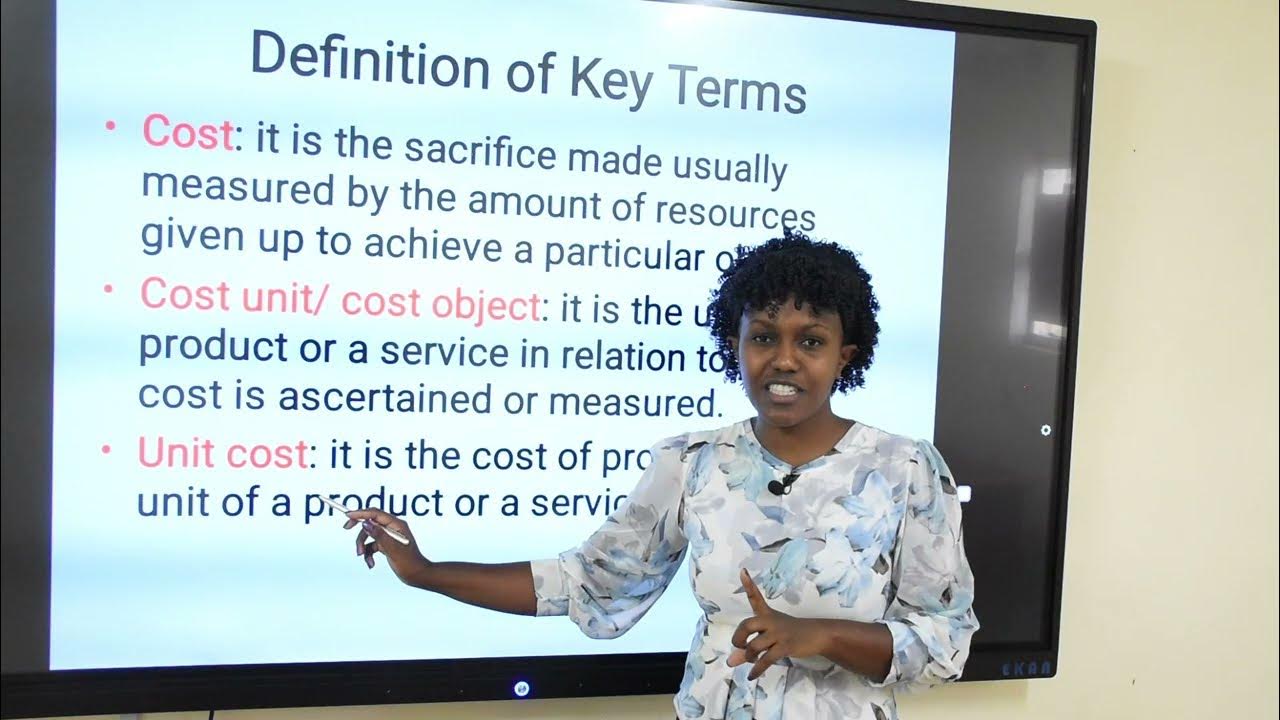

What is the definition of 'cost' in cost accounting?

-In cost accounting, 'cost' refers to the sacrifice of economic resources, measured in monetary terms, made to acquire goods or services that are expected to provide benefits either in the present or future for an organization.

What is the difference between 'cost' and 'expense'?

-A cost refers to the economic sacrifice made to acquire goods or services, while an expense occurs when the goods or services are used to generate revenue. Costs that are not yet utilized are classified as assets.

How does cost accounting contribute to decision-making?

-Cost accounting provides detailed cost information that helps in decision-making related to pricing, cost control, and profitability analysis. It also provides insights for special decisions such as make-or-buy decisions.

What are the three main objectives of cost accounting?

-The three main objectives of cost accounting are: 1) to determine the cost of production, 2) to control and manage costs, and 3) to provide relevant cost information for decision-making.

What is the difference between direct and indirect costs?

-Direct costs are those that can be directly traced to a specific cost object, such as raw materials for production. Indirect costs, on the other hand, cannot be traced to a specific cost object and are usually allocated across multiple objects, such as administrative expenses.

What are variable costs and how do they behave?

-Variable costs are expenses that change in direct proportion to changes in production or activity level. For example, raw material costs increase as production volume rises.

What are fixed costs and how do they behave?

-Fixed costs are expenses that do not change regardless of the level of production or activity. Examples include rent, salaries of permanent staff, and insurance.

What is a mixed cost?

-A mixed cost contains both fixed and variable components. It changes with the level of activity, but not in direct proportion. An example is utility bills, where a base charge (fixed) is supplemented by usage-based charges (variable).

What is the relationship between cost accounting, financial accounting, and management accounting?

-Cost accounting focuses specifically on tracking costs related to production and operations. Financial accounting involves recording all financial transactions to produce financial statements for external stakeholders. Management accounting provides internal management with financial and operational information for decision-making, often utilizing data from cost accounting.

Outlines

This section is available to paid users only. Please upgrade to access this part.

Upgrade NowMindmap

This section is available to paid users only. Please upgrade to access this part.

Upgrade NowKeywords

This section is available to paid users only. Please upgrade to access this part.

Upgrade NowHighlights

This section is available to paid users only. Please upgrade to access this part.

Upgrade NowTranscripts

This section is available to paid users only. Please upgrade to access this part.

Upgrade Now

5.0 / 5 (0 votes)