Why Apple's Partnership with Goldman Sachs Is The Future Of Banking | Forbes

Summary

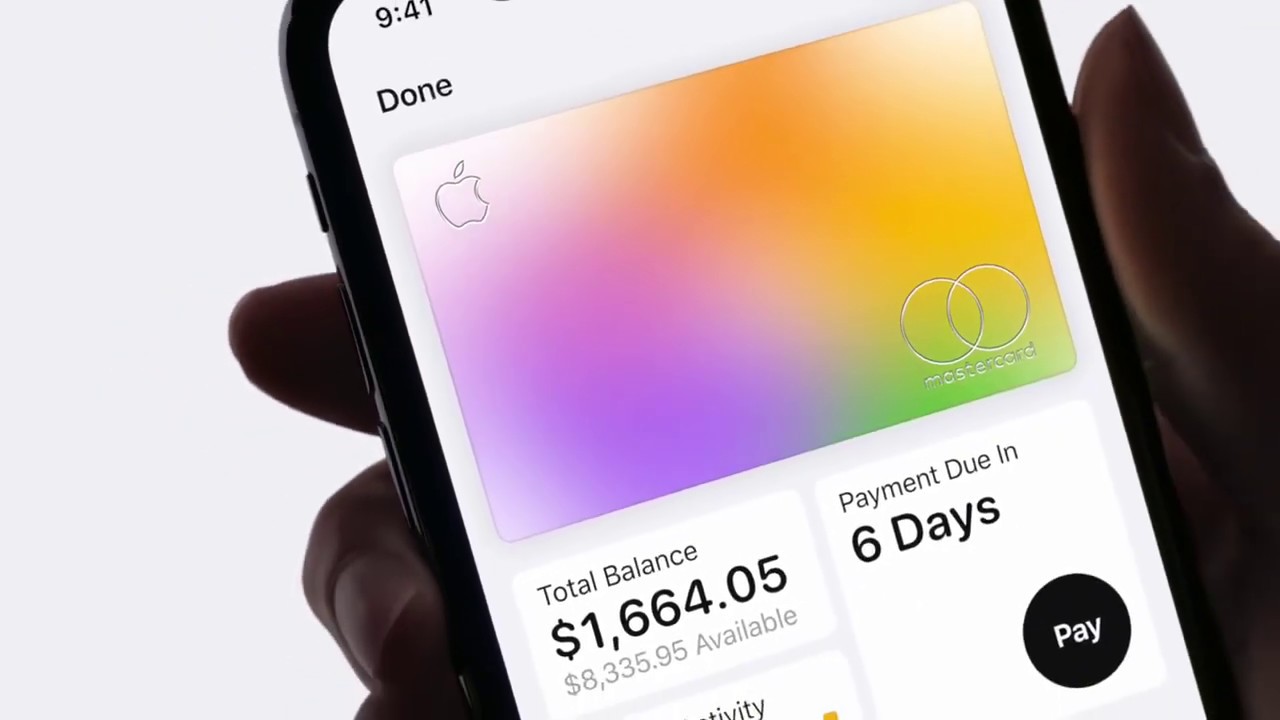

TLDRApple and Goldman Sachs have teamed up to launch a high-yield savings account for Apple Card holders, offering 4.15% returns with no minimums, lock-ups, and full FDIC insurance. This partnership leverages a banking-as-a-service model, with Goldman providing the banking infrastructure and Apple delivering a seamless tech interface. The move positions Apple as a neobank-like player, using its 2 billion iPhones as a distribution channel, while Goldman expands its consumer deposit base. The collaboration highlights a trend where banks serve as backend infrastructure for tech-driven financial services, signaling potential fintech consolidation and increased regulatory oversight in the coming years.

Takeaways

- 😀 Apple and Goldman Sachs are launching a high-yield savings account offering 4.15% returns, exclusively available to Apple Card holders.

- 😀 The partnership between Apple and Goldman Sachs is a 'banking as a service' arrangement, with Goldman providing banking infrastructure and Apple handling the consumer-facing tech interface.

- 😀 Unlike traditional banks, Apple and Goldman Sachs are offering no minimum balances, no lock-ups, and FDIC insurance on the savings account.

- 😀 Apple does not have a banking license, but is fronting for Goldman Sachs, which operates under the Marcus brand and is FDIC insured.

- 😀 This model places Apple in the category of neobanks like Chime or Monzo, offering financial services without a traditional bank license.

- 😀 Goldman Sachs benefits from Apple’s massive 2 billion iPhones worldwide, using them as a distribution channel for the savings account.

- 😀 The new offering from Apple and Goldman Sachs could be a competitive response to traditional banks, which generally offer lower savings account yields.

- 😀 Apple’s core business of selling phones allows them to enhance the user experience with services like financial products, unlike Google which had to abandon similar plans due to conflicts with cloud services customers.

- 😀 Online banks have gained market share by offering higher yields, and this move positions the Apple-Goldman partnership to compete with them more than traditional banks.

- 😀 This isn't the first time a large company has entered financial services; Sears tried a similar venture in the 1970s-1980s but eventually struggled due to retail competition.

- 😀 The partnership between Apple and Goldman Sachs may signal that banks are becoming behind-the-scenes providers for tech companies, with a focus on acquiring deposits through these partnerships rather than direct consumer marketing.

- 😀 There are regulatory considerations to the partnership, as the Office of the Comptroller of the Currency is keeping a close eye on banking-as-a-service models to ensure compliance with financial rules.

Q & A

What is the new savings account being launched by Apple and Goldman Sachs?

-Apple and Goldman Sachs are launching a high-yield savings account for consumers, offering a 4.15% annual return. This account is only available to Apple Card holders and can be accessed via the iPhone.

How is the partnership between Apple and Goldman Sachs structured?

-Goldman Sachs provides the banking infrastructure for the savings account, while Apple offers the user interface through its tech platform, combining banking with a seamless tech experience for consumers.

What makes this savings account different from traditional savings accounts?

-This savings account offers a 4.15% annual return with no minimum deposits, no lock-up periods, and FDIC insurance, which is significantly higher than the average savings account interest rate of less than 0.5% offered by traditional banks.

Why doesn’t Apple have a banking license for this savings account?

-Apple does not hold a banking license but fronts for Goldman Sachs Bank USA (Marcus), which is FDIC insured and has a state charter, allowing Apple to offer financial services through its platform.

What is a neobank, and how is Apple similar to one?

-A neobank is a digital bank without physical branches. Apple is considered a neobank because it offers banking services (through Goldman Sachs) without being a traditional bank itself, leveraging its tech to provide a seamless user experience.

How does the collaboration between Apple and Goldman Sachs benefit both companies?

-The collaboration allows Goldman Sachs to tap into Apple’s vast global distribution channel, as Apple has over 2 billion iPhones worldwide. This helps Goldman Sachs acquire more customers for its savings account. Meanwhile, Apple can enhance the utility of its devices by offering financial services.

How does this move by Apple and Goldman Sachs compare to Google’s attempt to launch a checking account?

-Unlike Google’s 2019 plan, which was canceled due to concerns about competing with its cloud service customers, Apple has no such conflict. Apple’s primary business is selling phones, so offering financial services enhances the utility of their devices, making them stickier and more valuable to users.

What advantages do online banks have over traditional banks in terms of savings accounts?

-Online banks operate without physical branches and fewer overhead costs, allowing them to offer higher interest rates on savings accounts compared to traditional banks, which are limited by their branch networks and larger support staff.

How do tech companies like Apple potentially change the future of the banking industry?

-Tech companies partnering with traditional banks could turn banks into invisible infrastructure, with the consumer-facing brand being the tech company. This could lead to a future where the banking brand becomes less important to consumers, shifting focus to the tech company providing the service.

What are the potential risks or challenges for the financials of this new partnership?

-The long-term financial viability of this partnership will need to be monitored closely, especially as fintech consolidates in the coming years. The regulatory landscape will also play a significant role in shaping the success of such partnerships.

Outlines

Этот раздел доступен только подписчикам платных тарифов. Пожалуйста, перейдите на платный тариф для доступа.

Перейти на платный тарифMindmap

Этот раздел доступен только подписчикам платных тарифов. Пожалуйста, перейдите на платный тариф для доступа.

Перейти на платный тарифKeywords

Этот раздел доступен только подписчикам платных тарифов. Пожалуйста, перейдите на платный тариф для доступа.

Перейти на платный тарифHighlights

Этот раздел доступен только подписчикам платных тарифов. Пожалуйста, перейдите на платный тариф для доступа.

Перейти на платный тарифTranscripts

Этот раздел доступен только подписчикам платных тарифов. Пожалуйста, перейдите на платный тариф для доступа.

Перейти на платный тарифПосмотреть больше похожих видео

5.0 / 5 (0 votes)