Long run supply curve in constant cost perfectly competitive markets | Microeconomics | Khan Academy

Summary

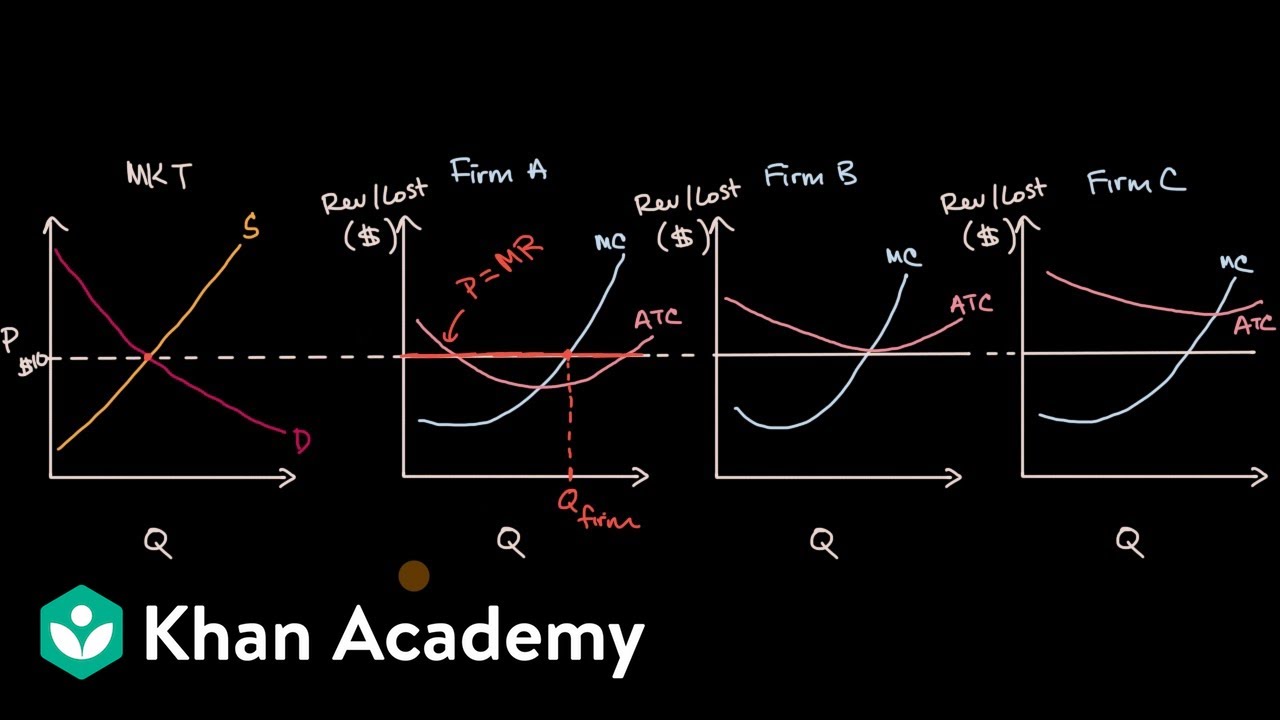

TLDRThe video discusses the dynamics of perfectly competitive markets, focusing on long-run implications. It explains how firms operate at zero economic profit due to market equilibrium, where price is determined by supply and demand. An increase in demand, illustrated by the rising popularity of apples, shifts the demand curve rightward, resulting in higher prices and economic profits for existing firms. This prompts new firms to enter the market, shifting the supply curve right until profits are eliminated. Ultimately, the market stabilizes at a higher quantity but returns to the original price, maintaining a horizontal long-run supply curve.

Takeaways

- 😀 The long run in economics is the timeframe in which firms can freely enter or exit the market, making fixed costs variable.

- 📈 In a perfectly competitive market, firms operate at zero economic profit in the long run, meaning total revenue equals total costs when opportunity costs are considered.

- 📊 Firms are price takers in a perfectly competitive market, responding to prices set by the equilibrium of supply and demand.

- 🍏 An increase in demand, such as due to a health study on apples, shifts the demand curve to the right, leading to a higher equilibrium price and quantity.

- 💰 When firms like Firm A see increased demand, they can achieve economic profit by producing until marginal revenue equals marginal cost.

- 🚪 Positive economic profits in a perfectly competitive market attract new firms, as there are no barriers to entry.

- ➡️ As new firms enter the market, the supply curve shifts to the right, eventually eliminating economic profits for all firms.

- 🔄 In a constant cost perfectly competitive market, the long-run supply curve becomes horizontal, indicating no change in costs with more firms entering the market.

- 📉 The market returns to a state where firms are making zero economic profit, even with a higher quantity of goods being sold.

- 📅 Future discussions will explore changes in cost structures based on the number of firms in the market.

Q & A

What distinguishes the long run from the short run in a perfectly competitive market?

-In the long run, firms can enter or exit the market, and fixed costs become variable. In contrast, the short run is a period during which firms cannot adjust their fixed costs.

What does it mean for firms in a perfectly competitive market to be price takers?

-Firms in a perfectly competitive market are price takers, meaning they must accept the market price determined by the equilibrium of supply and demand. They cannot influence the price with their output.

How is economic profit defined in the context of perfectly competitive markets?

-Economic profit is defined as the difference between total revenue and total costs, including opportunity costs. In the long run, firms in perfectly competitive markets typically earn zero economic profit.

What happens to the demand curve if a new study shows that a product, like apples, has significant health benefits?

-If a study reveals significant health benefits of apples, the demand curve shifts to the right, indicating that at every price level, consumers are willing to purchase more apples.

What is the impact of a rightward shift in the demand curve on equilibrium price and quantity?

-A rightward shift in the demand curve results in a higher equilibrium price and quantity, as suppliers respond to increased demand by producing more at the new price.

Why do firms enter a market when there are economic profits?

-Firms enter a market when they observe economic profits because the potential for profit motivates new entrants to capitalize on favorable market conditions.

What is a constant cost industry?

-A constant cost industry is one where the entry or exit of firms does not affect the cost structure of existing firms. In this type of market, the long-run supply curve is horizontal.

What occurs when new firms enter a perfectly competitive market?

-When new firms enter a perfectly competitive market, the supply curve shifts to the right, leading to a decrease in the equilibrium price until economic profits are eliminated.

How does a long-run supply curve behave in a constant cost perfectly competitive market?

-In a constant cost perfectly competitive market, the long-run supply curve is horizontal, indicating that the price remains stable regardless of the number of firms in the market.

What will happen to the market equilibrium if firms start incurring economic losses?

-If firms start incurring economic losses, some will exit the market, causing the supply curve to shift left until the remaining firms no longer experience losses, reaching a new equilibrium.

Outlines

Cette section est réservée aux utilisateurs payants. Améliorez votre compte pour accéder à cette section.

Améliorer maintenantMindmap

Cette section est réservée aux utilisateurs payants. Améliorez votre compte pour accéder à cette section.

Améliorer maintenantKeywords

Cette section est réservée aux utilisateurs payants. Améliorez votre compte pour accéder à cette section.

Améliorer maintenantHighlights

Cette section est réservée aux utilisateurs payants. Améliorez votre compte pour accéder à cette section.

Améliorer maintenantTranscripts

Cette section est réservée aux utilisateurs payants. Améliorez votre compte pour accéder à cette section.

Améliorer maintenantVoir Plus de Vidéos Connexes

Microeconomics Unit 3 COMPLETE Summary - Production & Perfect Competition

Economic profit for firms in perfectly competitive markets | Microeconomics | Khan Academy

Long run supply when industry costs are increasing or decreasing | Microeconomics | Khan Academy

Long-run economic profit for perfectly competitive firms | Microeconomics | Khan Academy

Perfect Competition- Microeconomics 3.7

"PASAR PERSAINGAN SEMPURNA" Kelompok 4

5.0 / 5 (0 votes)