Long-run economic profit for perfectly competitive firms | Microeconomics | Khan Academy

Summary

TLDRThe video explores the dynamics of perfectly competitive markets, highlighting how firms are price takers that adjust output to where marginal revenue equals marginal cost. Initially attracting new entrants due to economic profits, the market's supply curve shifts right, lowering prices until firms reach a long-run equilibrium with zero economic profit. This state signifies productive efficiency, where firms minimize average total costs. Conversely, excessive entry may lead to losses, prompting exits that shift supply back, restoring equilibrium. Ultimately, the market balances itself, achieving allocative efficiency with no deadweight loss.

Takeaways

- 😀 In perfectly competitive markets, firms are price takers, meaning they accept the market price as given.

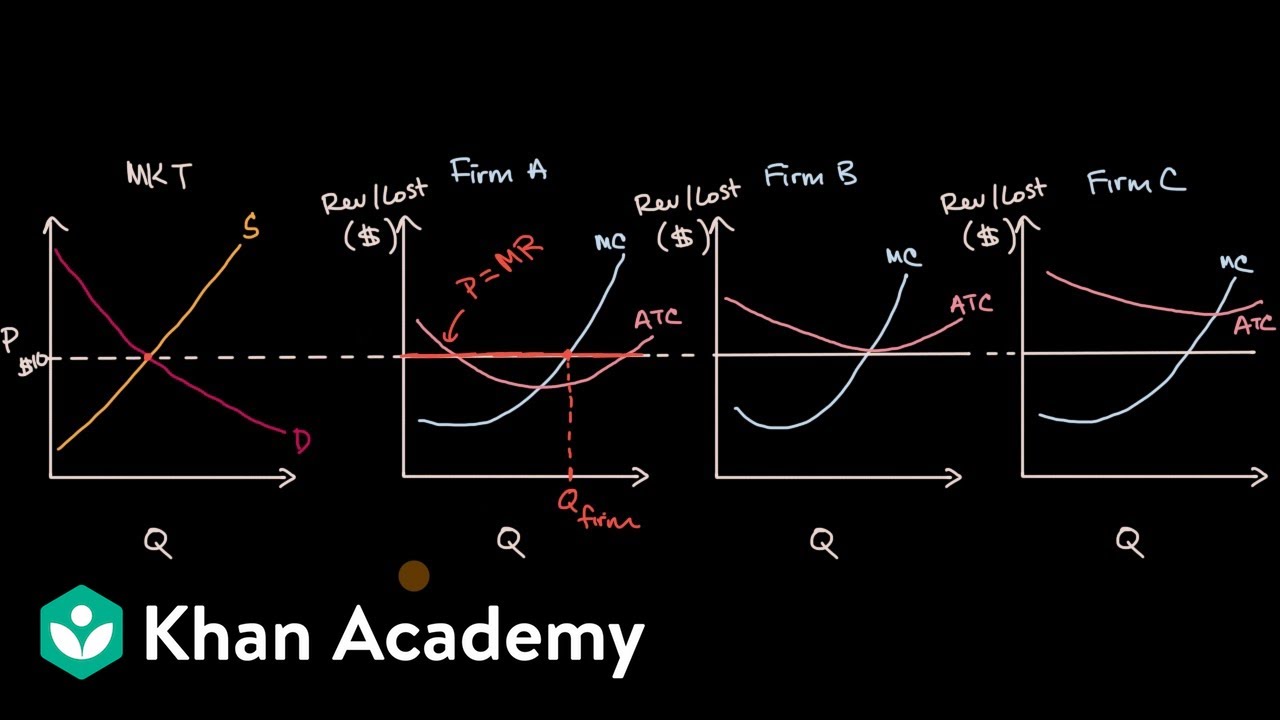

- 😀 Firms maximize profit by producing until marginal revenue equals marginal cost.

- 😀 Positive economic profits attract new firms to the market in the short run.

- 😀 The entry of new firms shifts the supply curve to the right, leading to lower equilibrium prices.

- 😀 In the long run, increased supply reduces economic profits to zero, achieving productive efficiency.

- 😀 Firms produce at the minimum point of the average total cost curve when economic profit is zero.

- 😀 Allocative efficiency occurs when marginal benefit equals marginal cost at the equilibrium price and quantity.

- 😀 If too many firms enter the market, firms may experience economic losses, prompting exits from the market.

- 😀 Exiting firms shift the supply curve back to the left, stabilizing prices and profits.

- 😀 The long-term outcome in a perfectly competitive market is zero economic profit, productive efficiency, and no deadweight loss.

Q & A

What defines the equilibrium price in a perfectly competitive market?

-The equilibrium price is defined by the intersection of the supply and demand curves.

What role do firms play in setting prices in a perfectly competitive market?

-Firms are price takers, meaning they do not set prices but accept the market price.

How do firms determine the quantity to produce in the short run?

-Firms produce where marginal revenue is greater than marginal cost, continuing until MR equals MC.

What happens to economic profit in the long run if firms are making a profit?

-If firms make economic profits, new firms enter the market, increasing supply and lowering prices until profits are zero.

What is the significance of marginal cost equaling average total cost in the long run?

-When marginal cost equals average total cost, firms are productively efficient, producing at the minimum point of the ATC curve.

What is the impact of new firms entering a market with existing economic profits?

-New entrants increase supply, shifting the supply curve to the right, which lowers the market price.

What happens when firms incur economic losses in a perfectly competitive market?

-Firms experiencing losses may exit the market, leading to a leftward shift in the supply curve and restoring equilibrium.

What is allocative efficiency in the context of perfectly competitive markets?

-Allocative efficiency occurs when resources are allocated such that marginal benefit equals marginal cost, maximizing societal welfare.

How is economic profit calculated?

-Economic profit is calculated by subtracting total costs, including opportunity costs, from total revenue.

What conditions lead to a perfectly competitive market achieving zero economic profit?

-Zero economic profit is achieved when firms operate at a point where MR equals MC and ATC, indicating no incentive for entry or exit.

Outlines

This section is available to paid users only. Please upgrade to access this part.

Upgrade NowMindmap

This section is available to paid users only. Please upgrade to access this part.

Upgrade NowKeywords

This section is available to paid users only. Please upgrade to access this part.

Upgrade NowHighlights

This section is available to paid users only. Please upgrade to access this part.

Upgrade NowTranscripts

This section is available to paid users only. Please upgrade to access this part.

Upgrade NowBrowse More Related Video

Economic profit for firms in perfectly competitive markets | Microeconomics | Khan Academy

Microeconomics Unit 3 COMPLETE Summary - Production & Perfect Competition

Introduction to Resource Markets and Marginal Revenue Product

Profit Maximisation in Perfect Competition

Perfect competition | Microeconomics | Khan Academy

TR, TC Approach & MR, MC Approach for Equilibrium Under Perfect Competition

5.0 / 5 (0 votes)