Long run supply when industry costs are increasing or decreasing | Microeconomics | Khan Academy

Summary

TLDRThis video explores the long-run equilibrium in a perfectly competitive market using the example of apple production. It discusses how shifts in demand, such as increased consumer interest in apples, can lead to higher prices and economic profits for firms. As new firms enter the market, input costs may rise, altering the cost structures and leading to a new equilibrium where economic profit returns to zero. The video also examines scenarios where input costs decrease with increased production, resulting in a downward-sloping long-run supply curve. This illustrates the dynamic nature of perfectly competitive markets.

Takeaways

- 📈 Perfectly competitive markets have many firms producing non-differentiated products with no barriers to entry or exit.

- ⚖️ Equilibrium price in a perfectly competitive market is determined by the intersection of supply and demand curves.

- 💰 Firms' marginal revenue is equal to the equilibrium price, influencing their production decisions.

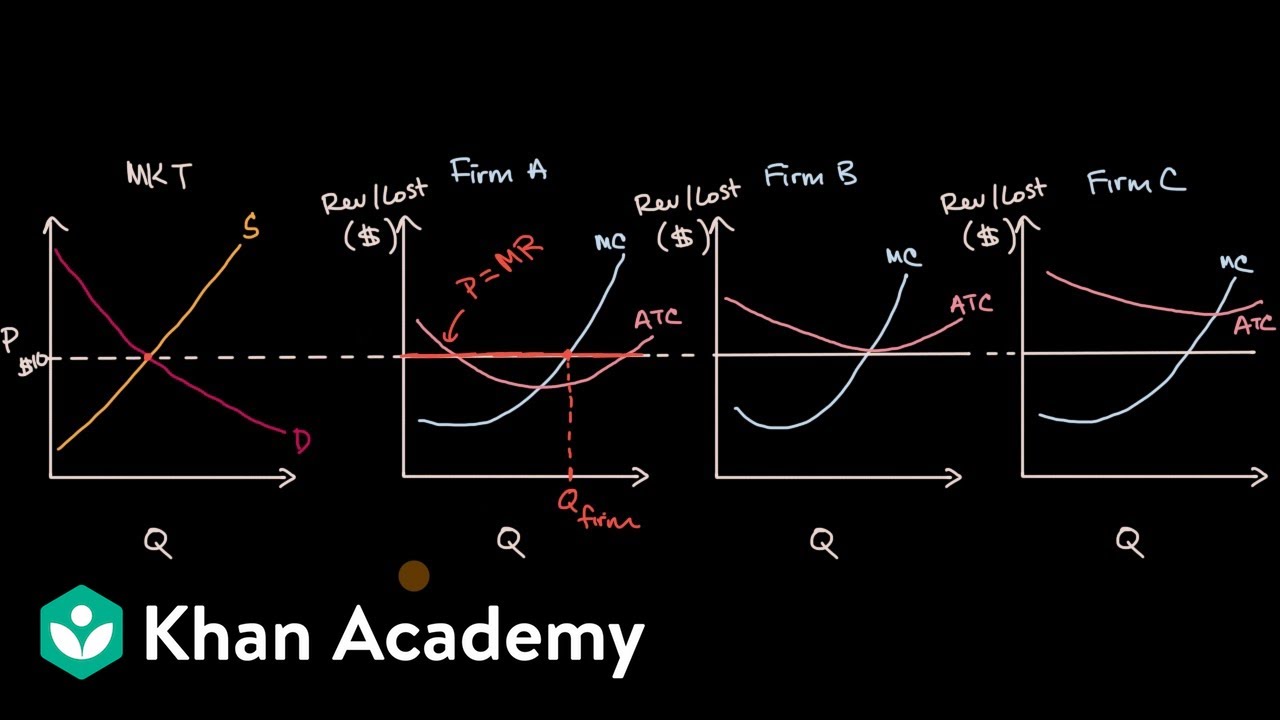

- 🔄 The rational quantity for firms to produce is where marginal revenue intersects marginal cost, leading to zero economic profit.

- 🚪 Positive economic profit attracts new firms to the market, while economic losses drive firms out.

- 🌟 A demand shock, such as a new study promoting apples, can shift the demand curve, increasing both equilibrium price and quantity.

- 📊 When demand increases, firms experience economic profit until more firms enter the market, shifting supply to a new equilibrium.

- 🔍 In an increasing cost environment, the entry of new firms raises input costs, affecting firms' marginal and average total cost curves.

- 🛑 Economic profit approaches zero as new firms enter until marginal revenue equals marginal cost and average total cost.

- ⬇️ In certain scenarios, increased market entry can lower input costs, leading to a downward sloping long run supply curve.

Q & A

What is the long-run equilibrium in a perfectly competitive market?

-The long-run equilibrium in a perfectly competitive market is the point where the equilibrium price is determined by the intersection of supply and demand curves, leading to zero economic profit for firms. At this point, average total cost equals marginal revenue.

How does a market shock affect equilibrium price and quantity?

-A market shock, such as an increase in demand due to new research on health benefits, shifts the demand curve to the right, resulting in a higher equilibrium price and quantity. This creates positive economic profits for firms.

What happens when firms in a perfectly competitive market experience economic profit?

-When firms experience economic profit, new firms are attracted to the market due to the opportunity for profit. This leads to increased competition and ultimately shifts the supply curve.

What is the significance of marginal revenue and marginal cost in production decisions?

-Firms decide their production quantity where marginal revenue equals marginal cost. This balance ensures that firms maximize their profits, as producing beyond this point would lead to losses.

What is the relationship between average total cost and marginal revenue at equilibrium?

-At equilibrium in a perfectly competitive market, average total cost equals marginal revenue. This condition ensures that firms earn zero economic profit, stabilizing the market.

What occurs if marginal revenue is greater than average total cost?

-If marginal revenue exceeds average total cost, firms earn positive economic profit, attracting new entrants to the market, which eventually increases supply and lowers prices.

What are the implications of increased input costs in a perfectly competitive market?

-Increased input costs, due to more firms entering the market, shift the marginal cost and average total cost curves upward. This can lead to a new equilibrium price that reflects these higher costs.

How do long-run supply curves behave in increasing cost environments?

-In increasing cost environments, the long-run supply curve slopes upward, indicating that as more firms enter the market, the costs of production inputs rise, leading to higher prices.

What happens in a decreasing cost environment for a perfectly competitive market?

-In a decreasing cost environment, increased market entry leads to lower production costs, resulting in a downward-sloping long-run supply curve as firms can produce more at lower prices.

How does the entry and exit of firms affect the market in the long run?

-The entry and exit of firms in response to economic profits or losses ensure that the market reaches a new equilibrium. This dynamic keeps the market competitive and stabilizes prices and quantities.

Outlines

This section is available to paid users only. Please upgrade to access this part.

Upgrade NowMindmap

This section is available to paid users only. Please upgrade to access this part.

Upgrade NowKeywords

This section is available to paid users only. Please upgrade to access this part.

Upgrade NowHighlights

This section is available to paid users only. Please upgrade to access this part.

Upgrade NowTranscripts

This section is available to paid users only. Please upgrade to access this part.

Upgrade NowBrowse More Related Video

Microeconomics Unit 3 COMPLETE Summary - Production & Perfect Competition

Long run supply curve in constant cost perfectly competitive markets | Microeconomics | Khan Academy

Long-run economic profit for perfectly competitive firms | Microeconomics | Khan Academy

Perfect Competition- Microeconomics 3.7

Market Structure Part 1: Introduction

Economic profit for firms in perfectly competitive markets | Microeconomics | Khan Academy

5.0 / 5 (0 votes)