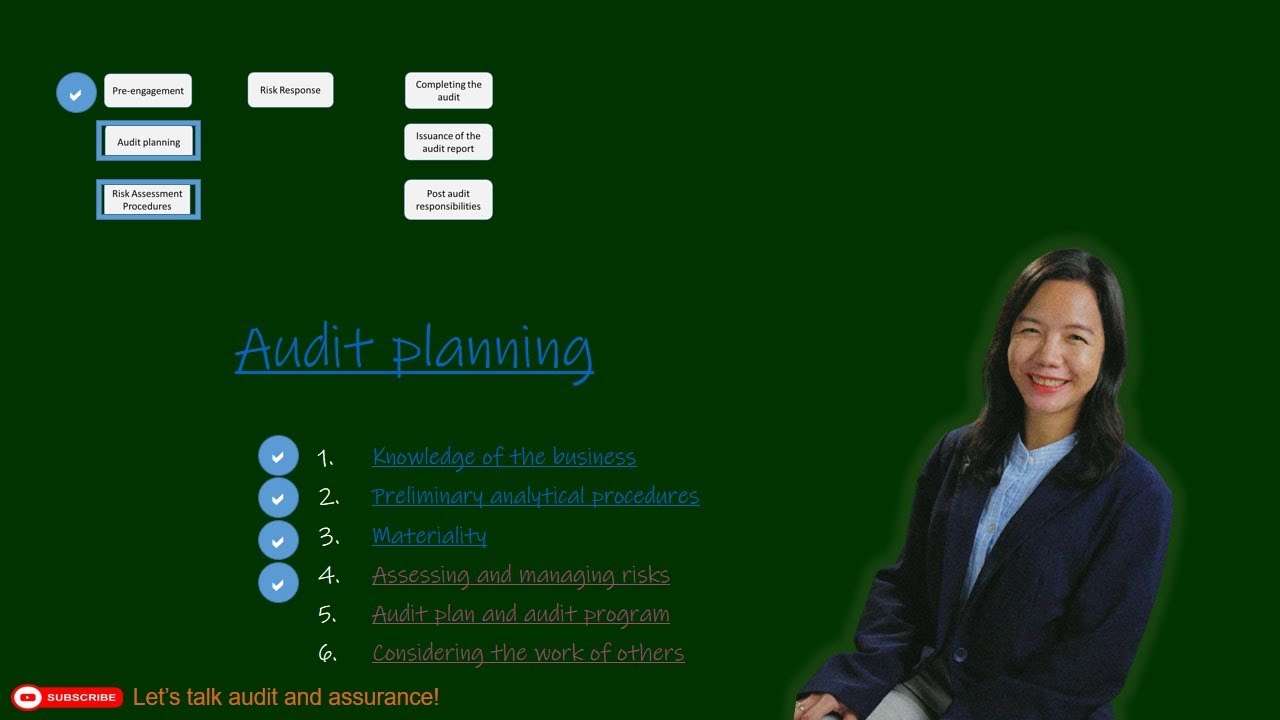

2.1 Overview of the Audit Process Introduction and Pre Engagement Activities

Summary

TLDRThis video script delves into the financial statements audit process, emphasizing a risk-based approach with three key phases: risk assessment, risk response, and conclusion and reporting. It starts with pre-engagement procedures, discussing client acceptance and continuance, and the importance of evaluating management's integrity. The script also highlights the necessity of an engagement letter to define the audit's scope and terms, and touches on considerations for recurring audits and changes in engagement terms.

Takeaways

- 📘 The script introduces a module focused on the financial statements audit process, emphasizing a deeper dive into the subject beyond the initial overview.

- 🔍 It highlights the importance of the risk-based audit approach, which is central to the financial statement audit process and consists of three phases: risk assessment, risk response, and conclusion and reporting.

- 🤔 The video discusses the pre-engagement phase, which includes client acceptance and continuance, and stresses the need for auditors to evaluate their competence, ethical requirements, and the client's auditability.

- 👤 The importance of assessing management's integrity is underscored, as it is critical to avoid complications during the audit engagement and to ensure a successful audit process.

- 📑 The necessity of an engagement letter is explained, which serves as a formal written agreement between the auditor and the client, outlining the terms of the engagement and minimizing misunderstandings.

- 💼 The script covers the contents of an engagement letter, which include the audit's objective, management's responsibilities, the financial reporting framework, and the scope of the audit, among other details.

- 🔄 The discussion touches on the conditions under which a new engagement letter may be required, such as changes in senior management, the nature or size of the client's business, or the financial reporting framework.

- 🚫 It advises on how to handle situations where a client requests a change in the terms of engagement, suggesting that auditors should only agree to changes if the reasons are justifiable and refuse or withdraw if they suspect the client is trying to avoid an unfavorable audit opinion.

- 👥 The video script also addresses the considerations for auditing components, such as subsidiaries or divisions, and the factors that may influence whether a separate engagement letter is needed for them.

- ⏰ The presenter acknowledges feedback about the length of previous videos and commits to keeping the discussion within 25 to 30 minutes per segment to enhance understanding and retention of concepts.

- 📈 The next phase of discussion will focus on audit planning, including topics like materiality, which is a significant aspect of the audit process and will be covered in subsequent videos.

Q & A

What is the main focus of the module discussed in the video script?

-The main focus of the module is to provide an overview of the financial statements audit process, including client acceptance, audit planning, and the risk-based audit approach.

What is the significance of the risk-based audit approach in the financial statement audit process?

-The risk-based audit approach is significant as it guides the auditor through three distinct phases: risk assessment, risk response, and conclusion and reporting, ensuring a structured and comprehensive audit.

What are the three phases of the risk-based audit approach?

-The three phases of the risk-based audit approach are risk assessment, risk response, and conclusion and reporting.

What does pre-engagement procedures involve in the context of auditing?

-Pre-engagement procedures involve client acceptance and continuance, evaluating the auditor's competence, ethical requirements including independence, and the capabilities to perform the audit engagement.

Why is evaluating the integrity of a client's management important in the auditing process?

-Evaluating the integrity of a client's management is crucial to avoid complications during the audit engagement and to ensure the reliability and credibility of the audit findings.

What is the purpose of an engagement letter in an audit engagement?

-An engagement letter serves as a formal written agreement between the auditor and the client, outlining the objectives, scope, responsibilities, and terms of the audit engagement to minimize misunderstandings and legal liabilities.

What factors determine whether a separate engagement letter should be sent to the components of an organization?

-Factors determining the need for a separate engagement letter for components include who appoints the auditor, whether a separate audit report is issued, legal requirements, the extent of work performed by other auditors, and the degree of ownership and independence of the component's management.

Why might an auditor consider discontinuing an engagement with an existing client?

-An auditor might consider discontinuing an engagement with an existing client due to evidence of management lacking integrity, difficulty in working with client personnel, inability to negotiate an acceptable fee increase, or if the client requires specialized services that the audit firm cannot provide.

What is the significance of discussing the company's management with the predecessor auditor?

-Discussing the company's management with the predecessor auditor is significant for understanding the reasons for the change in auditors, assessing management's integrity, and identifying potential disagreements that may impact the audit.

How can an auditor assess the auditability of a prospective client?

-An auditor can assess the auditability of a prospective client by evaluating the adequacy of accounting records and the quality of the client's internal controls, which are the responsibilities of the prospective client.

Outlines

Esta sección está disponible solo para usuarios con suscripción. Por favor, mejora tu plan para acceder a esta parte.

Mejorar ahoraMindmap

Esta sección está disponible solo para usuarios con suscripción. Por favor, mejora tu plan para acceder a esta parte.

Mejorar ahoraKeywords

Esta sección está disponible solo para usuarios con suscripción. Por favor, mejora tu plan para acceder a esta parte.

Mejorar ahoraHighlights

Esta sección está disponible solo para usuarios con suscripción. Por favor, mejora tu plan para acceder a esta parte.

Mejorar ahoraTranscripts

Esta sección está disponible solo para usuarios con suscripción. Por favor, mejora tu plan para acceder a esta parte.

Mejorar ahoraVer Más Videos Relacionados

5.0 / 5 (0 votes)