PERENCANAAN AUDIT - Strategi Audit Keseluruhan dan Program Audit

Summary

TLDRThis video script covers the eight stages of audit planning, focusing on the development of audit strategy and audit programs. It discusses the use of five types of audit tests—risk assessment procedures and subsequent audit procedures—to evaluate financial statements' fairness. The script delves into four key types of subsequent audit procedures: test of control, substantive tests of transactions, analytical procedures, and test of details of balances. It emphasizes how auditors assess risks, apply various audit procedures, and adjust strategies based on the client’s internal control effectiveness and risk levels, ultimately ensuring accurate and sufficient audit evidence.

Takeaways

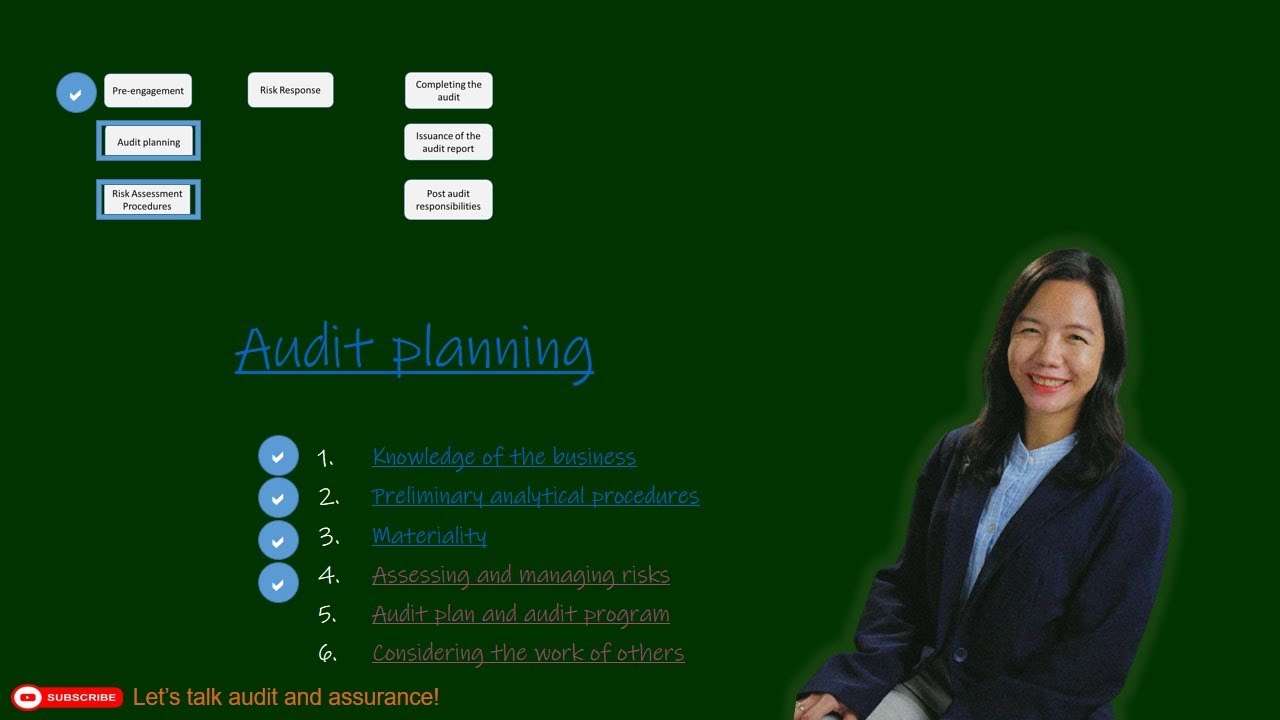

- 😀 The process of audit involves eight stages, with focus on the planning and design stages. The discussion centers around the development of the overall audit strategy and the audit program.

- 😀 Auditors use five types of audit tests to assess whether financial statements are presented fairly. These tests are categorized into two main groups: risk assessment procedures and subsequent audit procedures.

- 😀 Risk assessment procedures, from the first to the seventh stage of the audit, help identify and evaluate risks related to the client, including inherent risks, control risks, and fraud risks.

- 😀 The second group, subsequent audit procedures, is a response to the risks identified in the risk assessment stage. These procedures include four key audit tests: test of control, substantive test of transactions, substantive analytical procedures, and test of details of balances.

- 😀 The audit risk model helps auditors evaluate the relationship between risk factors and audit procedures, focusing on the assessment of inherent, control, and detection risks.

- 😀 Test of control (TOC) is used to gather sufficient evidence to support the assessment of control risk. Auditors use methods like inquiry, document examination, observation, and reperformance.

- 😀 Substantive test of transactions (STOT) directly impacts the accuracy of financial statement balances. It assesses the accuracy of transaction assertions, such as occurrence, completeness, accuracy, classification, and timing.

- 😀 Analytical procedures compare recorded amounts with auditor-developed expectations to detect potential material misstatements in financial statements.

- 😀 Test of details of balances focuses on verifying the ending balances of key accounts, especially those in the balance sheet or profit and loss accounts.

- 😀 Factors influencing the selection of audit tests include the availability of audit evidence, the relative cost of each test, the effectiveness of internal controls, and the inherent risks associated with the client.

Q & A

What are the eight stages in the audit planning process?

-The eight stages in the audit planning process are designed to help auditors assess risk and plan their procedures. The stages include client acceptance, risk assessment, understanding the client’s business and internal controls, testing the controls, performing substantive tests, and more. These stages guide the auditor in forming a strategy for the audit.

What is the role of risk assessment in the audit process?

-Risk assessment in the audit process helps the auditor identify potential risks in the financial statements. It involves evaluating the inherent risk, control risk, and fraud risk, which are key factors in determining the appropriate audit procedures and strategies.

How are the five types of audit tests used in audit planning?

-The five types of audit tests include risk assessment procedures, test of controls, substantive tests of transactions, substantive analytical procedures, and test of details of balances. These tests are used to evaluate the effectiveness of internal controls, assess financial statement assertions, and gather evidence to support audit conclusions.

What are the four types of audit procedures in the second group (further audit procedures)?

-The four types of audit procedures in the second group are: 1) Test of Control (TOC), 2) Substantive Test of Transactions (STOT), 3) Substantive Analytical Procedures (SAP), and 4) Test of Details of Balances (TDB). Each is designed to assess different aspects of financial accuracy and internal controls.

How does the auditor determine which audit procedure to prioritize?

-The auditor determines which procedure to prioritize based on factors such as the availability of evidence, the relative costs of each procedure, the effectiveness of internal controls, and the inherent risk of misstatements in the financial statements.

What is the relationship between control risk and the audit procedures used?

-If the auditor identifies a high control risk, they may choose to increase the use of substantive tests rather than relying on internal controls. The effectiveness of the controls influences whether the auditor will focus more on testing controls or substantive procedures.

What is the purpose of Test of Control (TOC) in an audit?

-Test of Control (TOC) is used to evaluate the effectiveness of a client's internal controls. This helps auditors understand how well the client’s controls work to prevent or detect material misstatements. The results help determine the extent of substantive testing required.

What is the function of Substantive Analytical Procedures (SAP)?

-Substantive Analytical Procedures (SAP) involve comparing recorded amounts to expected amounts developed by the auditor. They help detect inconsistencies or unusual fluctuations that may indicate misstatements in the financial statements.

How does the audit risk model influence audit strategy?

-The audit risk model helps the auditor assess and manage risk by evaluating three components: inherent risk, control risk, and detection risk. By understanding these factors, the auditor can adjust the audit strategy, choosing more or less extensive testing depending on the risk assessment.

What factors influence the auditor's decision between using Test of Control and substantive tests?

-Factors influencing the decision include the effectiveness of internal controls, the cost of obtaining sufficient audit evidence, and the level of inherent risk. If internal controls are weak, auditors tend to rely more on substantive testing. Conversely, strong internal controls may lead auditors to rely more on control testing.

Outlines

This section is available to paid users only. Please upgrade to access this part.

Upgrade NowMindmap

This section is available to paid users only. Please upgrade to access this part.

Upgrade NowKeywords

This section is available to paid users only. Please upgrade to access this part.

Upgrade NowHighlights

This section is available to paid users only. Please upgrade to access this part.

Upgrade NowTranscripts

This section is available to paid users only. Please upgrade to access this part.

Upgrade NowBrowse More Related Video

Tahapan Audit

Audit Snapshot: Audit Strategy, Audit Plan, Audit Program

FASE DE LA AUDITORIA PLANIFICACION ESPECIFICA

2.2 Overview of the Audit Process Auditing Planning Knowledge, Analytics, Materiality

Cara Melakukan Audit Kinerja Sektor Publik || Audit || Audit Kinerja

2.4 Overview of the Audit Process Audit Planning Audit Strategy vs Plan vs Program

5.0 / 5 (0 votes)