Volatility Arbitrage - How does it work? - Options Trading Lessons

Summary

TLDRIn this informative video, Patrick Boyle delves into the world of volatility trading, explaining the Black-Scholes model's role in pricing options and the real-world challenges it faces. He discusses how traders use delta hedging to manage risk and profit from volatility, highlighting the importance of understanding implied versus realized volatility. Boyle also explores the concept of volatility arbitrage, where traders buy low and sell high on volatility based on their forecasts, emphasizing the need for continuous re-hedging to capture profits. The video provides valuable insights for those interested in options trading and financial derivatives.

Takeaways

- 📚 Patrick Boyle introduces the topic of volatility trading and its relation to option pricing, specifically the Black-Scholes model.

- 💡 The Black-Scholes model assumes continuous and riskless delta hedging, which is not feasible in the real world due to trading limitations and market behavior.

- 💼 Real-world trading involves less frequent hedging, and traders often hedge after significant market moves, leading to deviations from the Black-Scholes model's predictions.

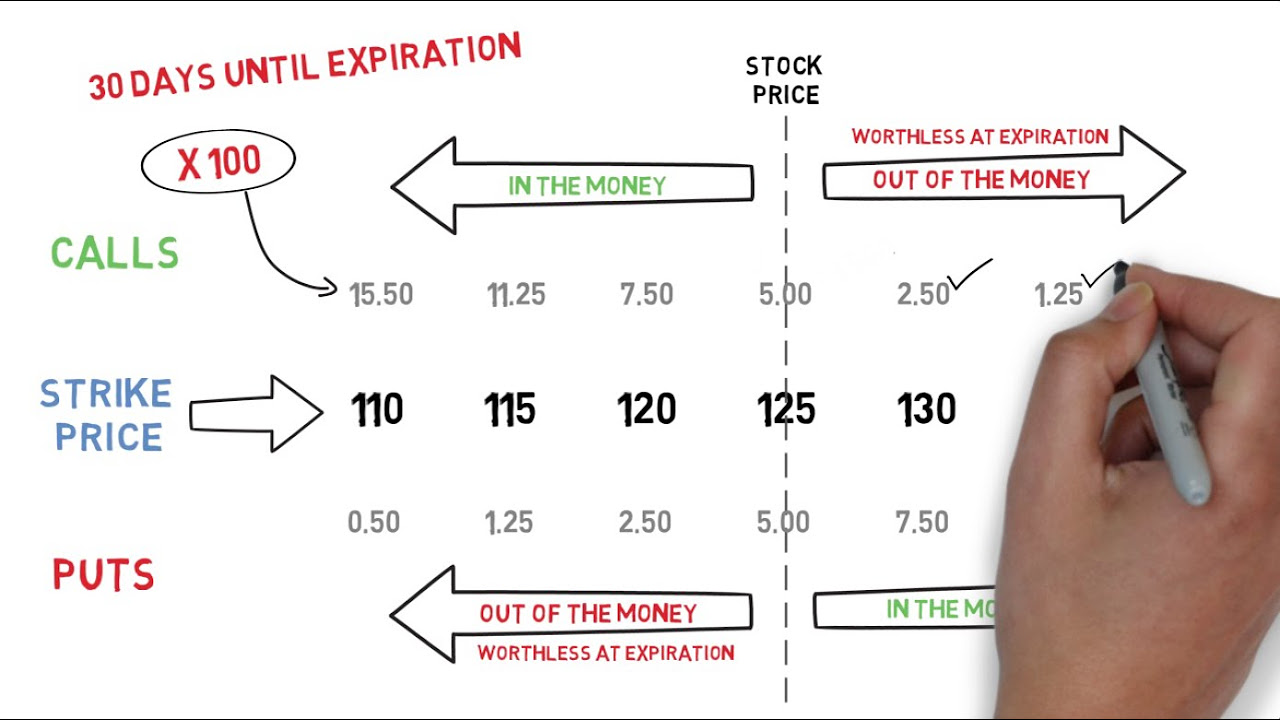

- 📉 The underlying assets do not always behave as the Black-Scholes model expects, with trading not being 100% continuous and asset prices experiencing jumps.

- 🌡 Volatility, or the standard deviation of the market, is not stable over the life of the option, which is a key assumption in the Black-Scholes model.

- 💰 Due to the challenges in perfect hedging, options are often sold at a premium to compensate for the risks and costs involved in trading.

- 🔄 Sellers of options are the counterparty with nearly unlimited downside, so they require additional compensation for selling options.

- 🛍 The price of an option is related to the cost of creating it, similar to any other product, and must cover the costs of production, including the risks involved.

- 🔄 Volatility arbitrage involves trading a delta-neutral portfolio to take advantage of differences between implied and forecasted realized volatility.

- 🤔 Volatility traders do not have a directional opinion on the market; they aim to profit from their view on volatility rather than the movement of the underlying asset.

- 📈 The profit in volatility trading comes from the continual rehedges required to maintain a delta-neutral position, which can result in gains if the realized volatility aligns with the trader's forecast.

Q & A

What is the main topic of Patrick Boyle's video?

-The main topic of Patrick Boyle's video is volatility trading, specifically how option traders trade and profit from the volatility of the underlying asset's price on which their option is based.

Why is the Black-Scholes model important in the investment industry?

-The Black-Scholes model is important because it provides a theoretical framework for pricing options. It suggests that if traders could continuously and risklessly delta hedge, the model would perfectly price options.

What are some real-world issues with the Black-Scholes model?

-Some real-world issues include the inability to trade continuously at every microsecond, the fact that underlying assets don't behave as the model assumes (e.g., asset prices jump on news), and that volatility is not stable over the life of the option.

Why do volatility traders and market makers charge a premium above the Black-Scholes price?

-Volatility traders and market makers charge a premium to compensate for the costs and risks associated with imperfect and riskless delta hedging, as well as for the administrative and IT expenses involved in trading options.

What is the relationship between the price of an option and implied volatility?

-The price of an option is closely tied to the implied volatility used in its calculation. Higher implied volatility generally leads to a more expensive option, and vice versa.

What is the role of a volatility arbitrage trader?

-A volatility arbitrage trader attempts to profit from differences between the implied volatility of an option and their forecast of future realized volatility. They aim to buy volatility when they believe it is low and sell when they think it is too high.

How do traders manage the directionality of options through hedging?

-Traders manage the directionality of options by delta hedging. This involves buying or selling the underlying asset to maintain a delta-neutral position, thereby isolating exposure to volatility rather than direction.

What is the significance of gamma in delta hedging?

-Gamma represents the rate of change of delta for a 1% change in the price of the underlying asset. It is crucial in delta hedging because it dictates how often and by how much the trader needs to adjust their position to maintain delta neutrality.

How can a trader realize a profit from a volatility trade?

-A trader can realize a profit if the realized volatility of the underlying asset is closer to their forecast than to the market's forecast (implied volatility). Profits are extracted through the continual rehedges required to maintain a delta-neutral portfolio.

What happens if the underlying asset's volatility is less than the implied volatility?

-If the underlying asset's volatility is less than the implied volatility, the trader who is long volatility (and has bought options) will likely lose money, as they would not make back the premium paid for the options through hedging.

What is the opposite outcome for a trader who is short volatility?

-If a trader is short volatility and the underlying asset's volatility is less than the implied volatility, they would keep the entire premium received from selling the options, as there would be no significant market movements requiring hedging.

How does the concept of 'Delta hedging' relate to the profitability of a volatility trade?

-Delta hedging is directly related to the profitability of a volatility trade. If the market moves less than expected, the trader makes back less of the premium paid. If it moves more, they make more than the premium spent, potentially generating significant profits.

Outlines

Esta sección está disponible solo para usuarios con suscripción. Por favor, mejora tu plan para acceder a esta parte.

Mejorar ahoraMindmap

Esta sección está disponible solo para usuarios con suscripción. Por favor, mejora tu plan para acceder a esta parte.

Mejorar ahoraKeywords

Esta sección está disponible solo para usuarios con suscripción. Por favor, mejora tu plan para acceder a esta parte.

Mejorar ahoraHighlights

Esta sección está disponible solo para usuarios con suscripción. Por favor, mejora tu plan para acceder a esta parte.

Mejorar ahoraTranscripts

Esta sección está disponible solo para usuarios con suscripción. Por favor, mejora tu plan para acceder a esta parte.

Mejorar ahoraVer Más Videos Relacionados

Understanding Market Makers || Optiver Realized Volatility Kaggle Challenge

Apa itu Instrumen Keuangan? - Dr. Erwinna Chendra

How to Trade with the Black-Scholes Model

Predict Market Volatility with 74% Accuracy Using this Key Metric

Options Trading: Understanding Option Prices

Everything you need to know to become a quant trader (in 2024) + sample interview problem

5.0 / 5 (0 votes)