Functionality is LIVE for filing rectification application of Adverse Order in Pursuance ofS.16(5/6)

Summary

TLDRThe video explains the new functionality available on the GST portal for filing rectification applications regarding wrongly availed credit due to time limitations, as outlined in Sections 16(4), 16(5), and 16(6). Taxpayers can now submit rectification applications within six months from October 8, 2024, to rectify adverse orders related to credit claims. The process involves downloading Annexure A, filling in details of the adverse order, and submitting it online. The rectification must be completed by the officer within three months. The video also discusses benefits for cancelled registrations and provides guidance on the process.

Takeaways

- 😀 The GST portal now offers functionality for filing rectification applications for wrongly availed credit due to time limitations under Section 16(4).

- 😀 Taxpayers need to file the rectification application within six months from October 8, 2024, as per Notification 22/2024-Central Tax.

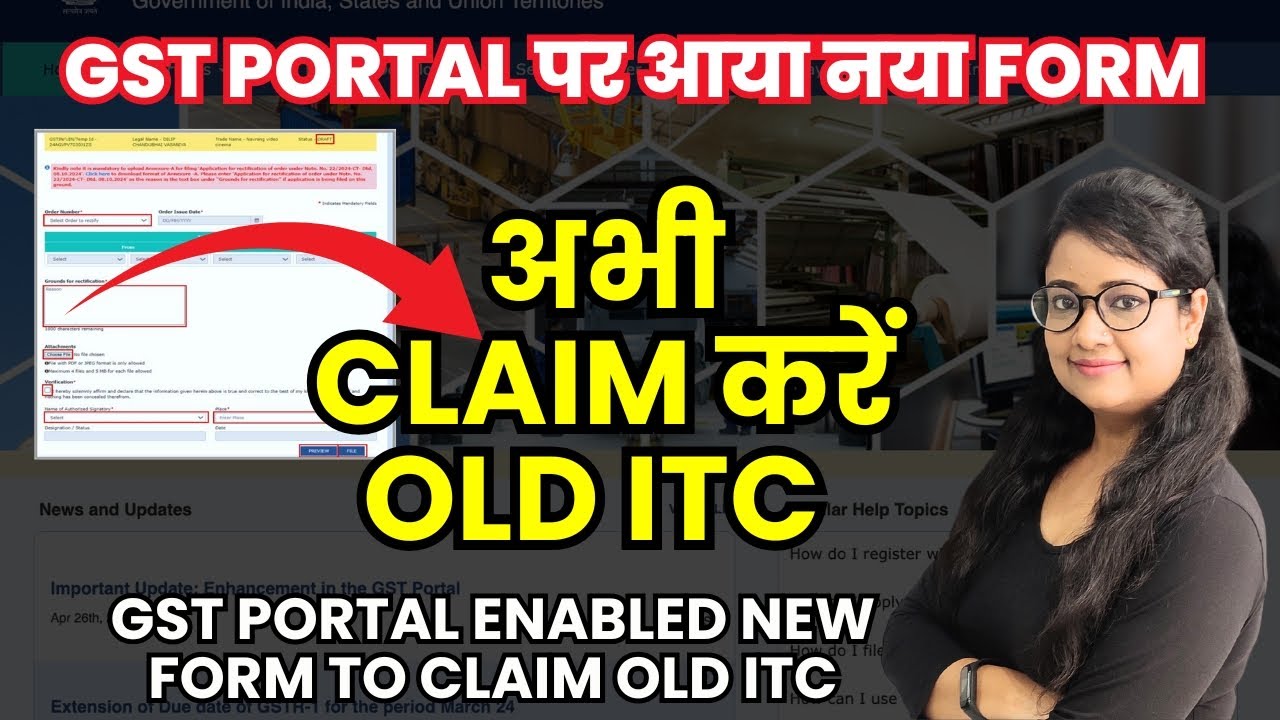

- 😀 To file the rectification, taxpayers must go to 'Services > User Services > My Application' on the GST portal and download Annexure A.

- 😀 Annexure A must be filled with details about the adverse order passed under Section 73, 74, or 107, and uploaded on the GST portal.

- 😀 A rectification application must be filed by the taxpayer who has not filed an appeal for wrongly availed credit due to the time limitation under Section 16(4).

- 😀 The concerned officer will rectify the adverse order within three months of receiving the rectification application.

- 😀 Section 16(5) provides relief for wrongly availed credit for financial years 2017-2021, subject to certain conditions such as timely filing of GSTR 3B.

- 😀 If taxpayers have not filed GSTR 3B correctly but reported credit in GSTR 9C, they may still be eligible for benefits, although this is subject to litigation.

- 😀 Canceled taxpayers who could not file returns due to registration cancellation can also benefit from Section 16(6) if they file returns within specific timelines.

- 😀 Taxpayers who have already paid or reversed the wrongly claimed ITC might not be eligible for the benefits provided in this notification, though this is a subject of legal debate.

- 😀 Detailed guidelines and step-by-step instructions, including a tutorial video, are available to help taxpayers complete the rectification application process efficiently.

Q & A

What is the main purpose of the new functionality on the GST portal?

-The new functionality allows taxpayers to file rectification applications for adverse orders related to wrongly availed credits due to the limitation period under Section 16(4) of the GST Act.

What sections of the GST Act are relevant for filing the rectification application?

-Sections 16(4), 16(5), and 16(6) of the GST Act are relevant. Section 16(4) addresses the time limitation for claiming credits, Section 16(5) provides one-time relief, and Section 16(6) gives relief for taxpayers whose registration has been canceled.

What is the deadline for filing the rectification application?

-The rectification application must be filed within 6 months from October 8, 2024, which is the date of the notification.

How should a taxpayer file a rectification application on the GST portal?

-A taxpayer needs to log in to the GST portal, navigate to 'Services > User Services > My Applications', select 'New Application', download Annexure A, fill in the required details, and upload it within 6 months.

What is Annexure A, and how is it used in the rectification process?

-Annexure A is a form that needs to be downloaded from the GST portal, filled with details about the adverse order, and uploaded as part of the rectification application process.

Who processes the rectification application once submitted?

-The rectification application is sent to the relevant officer who passed the adverse order, and they are required to rectify the order within 3 months of receiving the application.

What benefit does Section 16(5) provide for taxpayers?

-Section 16(5) provides one-time relief for rectifying wrongly availed credits due to the time limitation, specifically for the initial four financial years (2017-2021), provided certain conditions are met.

Can taxpayers avail the benefits of Section 16(5) if they missed showing credit in GSTR-3B?

-According to the provisions, if credit was missed in GSTR-3B but correctly reported in the relevant annual return (GSTR-9), taxpayers should still be able to avail the benefit, though this may be subject to litigation.

What should taxpayers do if they are involved in litigation regarding an adverse order?

-Taxpayers involved in litigation should reply to the notice or adjudication authority, referencing Section 16(5). The authority will then process the matter and pass an order according to the provisions.

Why are taxpayers who have reversed or paid the wrongly availed ITC excluded from receiving the benefit?

-The current provisions under Section 150 of the Finance Act, 2024 exclude taxpayers who have already reversed or paid the amount due to the alleged wrongly availed ITC. However, there is an argument that such taxpayers should also be eligible for the benefit, as they have paid the amount under valid authority.

Outlines

Esta sección está disponible solo para usuarios con suscripción. Por favor, mejora tu plan para acceder a esta parte.

Mejorar ahoraMindmap

Esta sección está disponible solo para usuarios con suscripción. Por favor, mejora tu plan para acceder a esta parte.

Mejorar ahoraKeywords

Esta sección está disponible solo para usuarios con suscripción. Por favor, mejora tu plan para acceder a esta parte.

Mejorar ahoraHighlights

Esta sección está disponible solo para usuarios con suscripción. Por favor, mejora tu plan para acceder a esta parte.

Mejorar ahoraTranscripts

Esta sección está disponible solo para usuarios con suscripción. Por favor, mejora tu plan para acceder a esta parte.

Mejorar ahoraVer Más Videos Relacionados

Implementation of new Section 16(5) & (6) for availment of GST Credit for FYs 2017-18 to 2020-21

All GST Returns Date extended | New Dates to file GST Returns |

Time Barred ITC Claim Big Relief section 16(4) gst New Section 16 (5) & 16 (6) Final Budget

GST ITC big update - Claim your Old ITC | File Application to claim Old Input Tax Credit under GST

GSTR 3B Feb 2026 से बदली | New GST ITC Set-Off Rule 2026 | How to file GST Returns 2026

When GST Credit availed in GSTR 3B is not Matching with GSTR 2A || CA (Adv) Bimal Jain

5.0 / 5 (0 votes)