What is Monte Carlo Simulation?

Summary

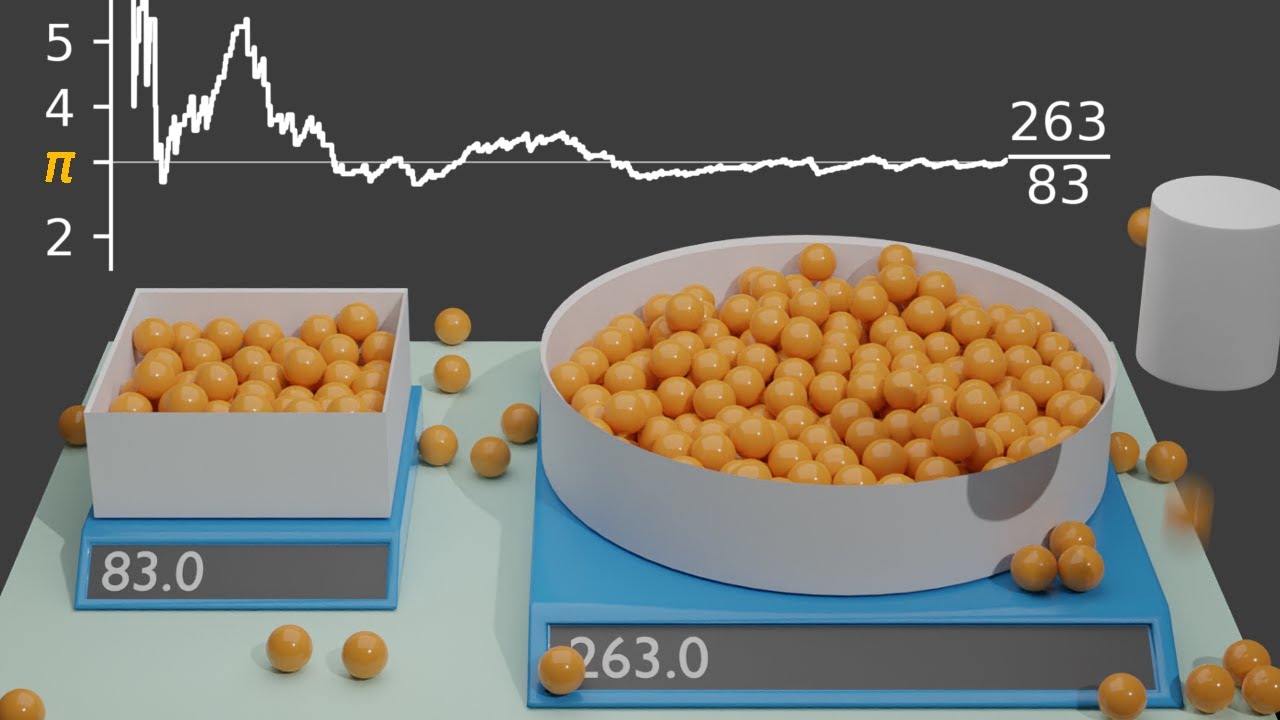

TLDRMonte Carlo simulations, a mathematical technique for predicting uncertain outcomes, are explored in this script. It explains how they model probabilities through random sampling, reducing the need for extensive manual calculations. The video highlights their use in portfolio management, investment planning, and various other fields. It outlines the three-step process of running a simulation: setting up a predictive model, specifying probability distributions, and running simulations to gather a representative sample. By calculating variance and standard deviation, Monte Carlo simulations offer insights into future possibilities without actual time travel.

Takeaways

- 🔮 Monte Carlo simulations are a mathematical technique used to estimate outcomes of uncertain events by modeling probabilities and using random sampling.

- 🎲 The process involves generating multiple outcomes to calculate an average result, like estimating the probability of rolling certain numbers on dice.

- 💼 Monte Carlo simulations are widely used in fields such as portfolio management and investment planning to understand potential performance under various conditions.

- 📊 They are also used for risk analysis, option pricing, and planning for spare capacity, showcasing their versatility in different applications.

- 🌐 The technique is not limited to finance; it's applied across various fields including medicine, astrophysics, and even in solving puzzles like Wordle.

- 🛠️ Running a Monte Carlo simulation involves three steps: setting up a predictive model, specifying the probability distribution of variables, and running simulations to generate random values.

- 📈 The predictive model identifies dependent and independent variables, which are the inputs that drive the predictions.

- 📊 Probability distribution is defined using historical data or expert judgment, assigning likely values and their probability weights.

- 🔁 Simulations are run repeatedly until a representative sample is gathered, which helps in understanding the range of possible outcomes.

- 📊 Variance and standard deviation are calculated to measure the spread within the sample, indicating the accuracy of the Monte Carlo estimation.

- 🚀 While Monte Carlo simulations don't offer actual time travel, they provide a clearer picture of future possibilities and help in making informed decisions.

Q & A

What is Monte Carlo simulation?

-Monte Carlo simulation is a mathematical technique used to estimate possible outcomes of uncertain events by modeling the probability of different outcomes using random sampling.

How does Monte Carlo simulation provide insights into the future?

-It simulates multiple possible outcomes by randomly sampling the range of potential results, allowing for an estimation of the average result and a better understanding of future possibilities.

What is an example of using Monte Carlo simulation to calculate probabilities?

-The script provides the example of calculating the probability of rolling a seven with two standard dice by randomly sampling the 36 possible outcomes and determining the percentage of times a seven is rolled.

Who are the typical users of Monte Carlo simulations?

-Monte Carlo simulations are commonly used by investors for portfolio management and investment planning, as well as in various fields such as risk analysis, option pricing, spare capacity planning, medicine, and astrophysics.

What are the three basic steps involved in running a Monte Carlo simulation?

-The steps are: 1) Setting up the predictive model by identifying dependent and independent variables, 2) Specifying the probability distribution for the independent variables, and 3) Running simulations by repeatedly generating random values of the independent variables until a representative sample is gathered.

Why is random sampling important in a Monte Carlo simulation?

-Random sampling is crucial as it allows for the generation of multiple possible outcomes, which are then used to calculate average results and understand the range of potential outcomes.

How can investors benefit from Monte Carlo simulations in portfolio management?

-Investors can gain insights into how their portfolio might perform under different market conditions by running thousands or millions of simulations, thus making more informed decisions.

What is the purpose of calculating variance and standard deviation in Monte Carlo simulations?

-Variance and standard deviation are measures of spread used to compute the range of variation within a sample, which helps in understanding the accuracy and reliability of the simulation results.

How does the number of simulations affect the accuracy of Monte Carlo results?

-The more simulations run, the larger the sample size, which in turn increases the accuracy of the estimation by providing a more representative view of the possible outcomes.

Can Monte Carlo simulations predict the exact future outcomes?

-No, Monte Carlo simulations do not predict exact future outcomes but provide a range of possible outcomes and their probabilities, offering a better understanding of potential future scenarios.

What is the significance of modifying underlying parameters in Monte Carlo simulations?

-Modifying the underlying parameters allows for the exploration of different scenarios and conditions, thus providing a more comprehensive analysis of the system or process being studied.

Outlines

Esta sección está disponible solo para usuarios con suscripción. Por favor, mejora tu plan para acceder a esta parte.

Mejorar ahoraMindmap

Esta sección está disponible solo para usuarios con suscripción. Por favor, mejora tu plan para acceder a esta parte.

Mejorar ahoraKeywords

Esta sección está disponible solo para usuarios con suscripción. Por favor, mejora tu plan para acceder a esta parte.

Mejorar ahoraHighlights

Esta sección está disponible solo para usuarios con suscripción. Por favor, mejora tu plan para acceder a esta parte.

Mejorar ahoraTranscripts

Esta sección está disponible solo para usuarios con suscripción. Por favor, mejora tu plan para acceder a esta parte.

Mejorar ahora

5.0 / 5 (0 votes)