materi AP 2 Rekonsiliasi bank

Summary

TLDRThis video discusses the importance of internal control and cash accounting procedures within a company. It highlights how internal control ensures operational efficiency, asset security, and compliance with regulations. The key focus is on cash management, including safeguarding assets, preventing fraud, and ensuring accurate financial reporting. The video also covers practical examples of cash internal controls, such as segregation of duties, deposit procedures, and the use of checks. Additionally, it explains the process of bank reconciliation to adjust discrepancies between bank and company records, and how to make journal adjustments based on these findings.

Takeaways

- 😀 Internal control refers to a plan, method, and procedure designed by management to ensure operational efficiency, financial reliability, asset security, and compliance with laws and policies.

- 😀 The main objective of cash internal control is to protect company assets from misuse, prevent fraud, and ensure that accurate and trustworthy accounting data is maintained.

- 😀 Cash is highly liquid compared to other assets, making it vulnerable to fraud and theft, which is why a proper internal control system is crucial for cash management.

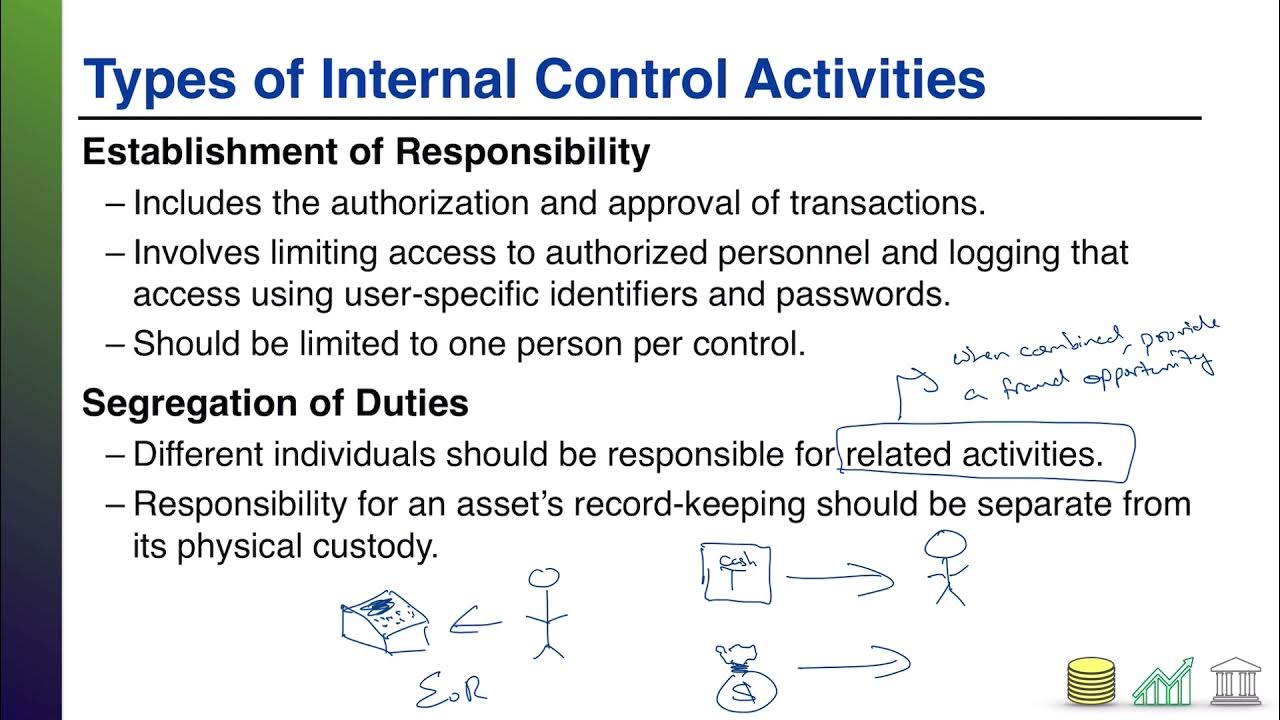

- 😀 Key examples of internal control for cash include clear responsibility assignment, task separation, cash deposit policies, and using checks for cash disbursements.

- 😀 Bank reconciliation is the process of matching the bank's records with the company's records to identify discrepancies and ensure accurate cash reporting.

- 😀 Differences between bank and company records can occur when transactions are not recorded at the same time by either party, such as deposit delays or outstanding checks.

- 😀 Companies should regularly deposit collected cash into the bank, ideally daily or at regular intervals, to maintain proper cash flow and internal control.

- 😀 Examples of bank reconciliation discrepancies include deposits in transit, checks that haven't been cashed, and unrecorded bank fees or interest income.

- 😀 Adjustments for bank reconciliation should include correcting errors made by the bank (e.g., misapplied checks) or by the company (e.g., unrecorded bank charges).

- 😀 Jurnal adjustments are necessary for correcting discrepancies and should be made by the company based on the identified causes of the mismatch between the bank and company's records.

Q & A

What is the primary purpose of internal control in cash management?

-The primary purpose of internal control in cash management is to protect company assets from misuse or loss, ensure accurate financial reporting, and prevent fraud or theft, given cash's highly liquid nature.

Why is cash considered a high-risk asset in terms of internal control?

-Cash is considered a high-risk asset because it is highly liquid and can be easily accessed or misappropriated compared to other types of assets, making it more susceptible to theft or fraud.

What are the key methods to implement internal control over cash?

-Key methods include assigning clear responsibilities for cash handling, segregating duties (e.g., separating cash handling, recording, and authorization), using insurance for valuable assets, and ensuring regular bank deposits and checks for payments.

What is bank reconciliation and why is it important?

-Bank reconciliation is the process of comparing the company's cash book with the bank's records to identify and correct any discrepancies. It is important to ensure that both records match and to detect errors or fraud.

What are some common causes of discrepancies during bank reconciliation?

-Common causes include deposits in transit (company deposits not yet recorded by the bank), outstanding checks (checks written but not yet cashed), bank errors (e.g., incorrect withdrawals), and unrecorded bank transactions (e.g., fees or interest income).

What is meant by 'deposits in transit' in the context of bank reconciliation?

-Deposits in transit refer to funds that the company has already deposited but the bank has not yet recorded. These are common at the end of an accounting period when deposits are made but not processed before the bank statement is issued.

How should a company handle uncleared checks during bank reconciliation?

-Uncleared checks, which are checks written by the company but not yet presented to the bank for payment, should be deducted from the bank’s records during reconciliation, as the bank has not yet processed them.

What role does 'segregation of duties' play in cash management?

-Segregation of duties ensures that no single individual is responsible for both handling cash and recording cash transactions. This reduces the risk of fraud or errors by providing checks and balances within the process.

When reconciling bank statements, what adjustments might a company need to make?

-Adjustments might include adding unrecorded bank deposits, deducting uncleared checks, adjusting for bank fees or interest, and correcting errors in the company's own records (e.g., overstated checks or transactions).

How are errors in bank transactions, such as incorrect withdrawals or failed deposits, handled during bank reconciliation?

-Errors in bank transactions are corrected by adjusting the bank's records or the company's records, depending on which party made the mistake. The company will adjust its records if the error was on its side, or the bank will correct its own records if it made the mistake.

Outlines

此内容仅限付费用户访问。 请升级后访问。

立即升级Mindmap

此内容仅限付费用户访问。 请升级后访问。

立即升级Keywords

此内容仅限付费用户访问。 请升级后访问。

立即升级Highlights

此内容仅限付费用户访问。 请升级后访问。

立即升级Transcripts

此内容仅限付费用户访问。 请升级后访问。

立即升级

5.0 / 5 (0 votes)