Konsep Biaya ..... #AkuntansiBiaya

Summary

TLDRThis lecture on cost accounting covers fundamental concepts such as the distinction between cost and expense, cost objects, and various cost classifications. It delves into how costs are assigned to specific activities or items, including direct and indirect costs, and variable, fixed, and semi-variable costs. The session highlights the importance of accurate cost information for decision-making and performance evaluation. Real-world examples and calculations are provided to illustrate how to determine costs like raw materials, labor, and overhead. The lecture emphasizes the role of cost accounting systems in helping businesses achieve strategic goals and financial effectiveness.

Takeaways

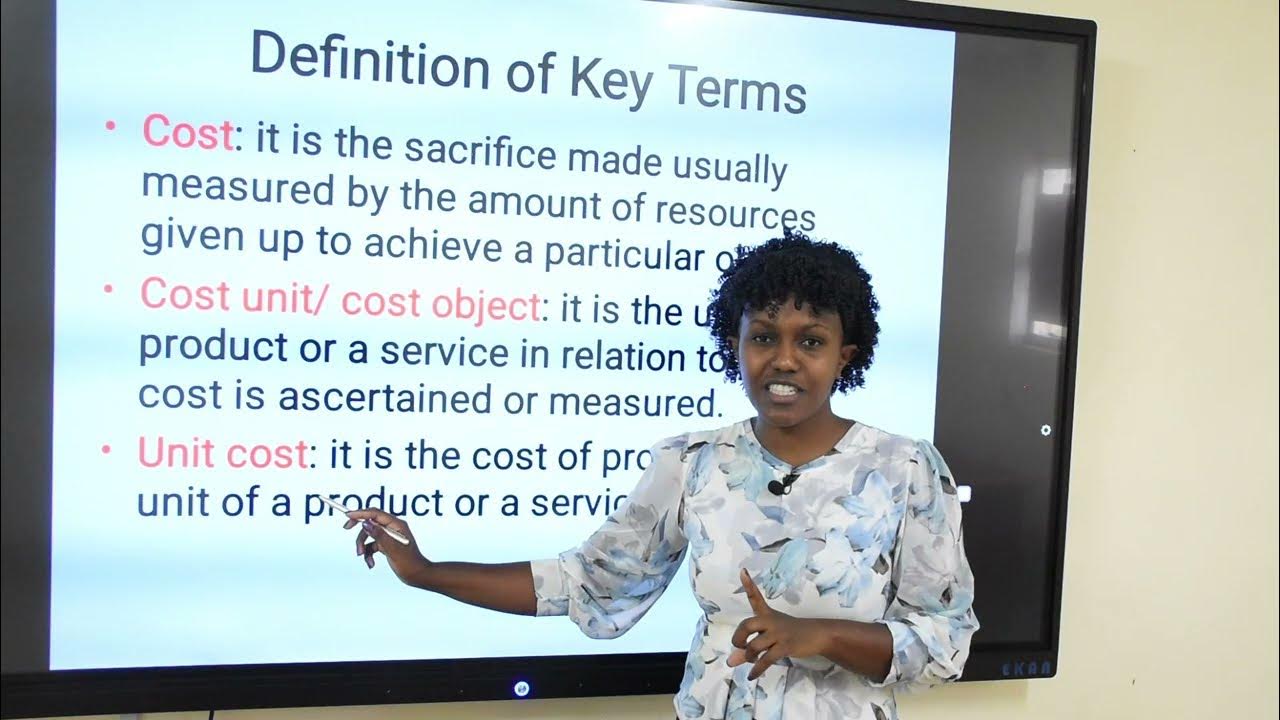

- 😀 Cost and Expense are different concepts: Cost refers to economic resource expenditure recorded as assets, while Expense refers to costs that have been consumed and are recorded in the income statement.

- 😀 A cost object is any item or activity to which costs are assigned, such as products, departments, or projects.

- 😀 Direct costs can be directly traced to cost objects, whereas indirect costs are allocated based on various methods.

- 😀 Variable costs change proportionally with production activity, while fixed costs remain constant regardless of activity level.

- 😀 Semi-variable costs vary with activity, but not in a direct or proportional way (e.g., utility bills with fixed and variable components).

- 😀 Production costs include direct materials, direct labor, and manufacturing overhead, while non-production costs encompass selling, administrative, and general expenses.

- 😀 Costs are classified into capital expenditure (benefiting multiple periods) and revenue expenditure (benefiting only the current period).

- 😀 A cost accounting system must include a chart of accounts, data processing systems, and performance measures to ensure accurate reporting.

- 😀 Direct costs, such as materials and labor, are traced directly to a product, whereas indirect costs, like factory overhead, are allocated to products.

- 😀 Understanding cost behavior helps businesses predict financial outcomes and make informed decisions about pricing, budgeting, and resource allocation.

- 😀 Accurate cost information enables management to set profit targets, evaluate departmental performance, and identify areas of improvement or failure.

Q & A

What is the difference between cost and expense in accounting?

-Cost refers to the expenditure of economic resources measured in monetary terms, while expense refers to costs that have provided benefits and are now considered consumed. Costs are recorded as assets, whereas expenses are recorded in the profit and loss statement to reduce revenue.

How are costs classified in terms of direct and indirect?

-Direct costs can be traced directly to a specific object or activity, such as raw materials or direct labor. Indirect costs, on the other hand, cannot be traced directly to a specific object or activity, and are typically allocated across various objects or activities.

What is the role of cost objects in cost accounting?

-A cost object is defined as an item or activity where costs are accumulated and calculated. These objects can include products, product lines, projects, contracts, departments, or even customer orders.

What is the purpose of tracing costs to cost objects?

-Tracing costs to cost objects allows businesses to reliably allocate costs, which can then serve as a basis for predicting future expenses and making informed decisions regarding pricing, budgeting, and performance evaluation.

What is the difference between variable costs, fixed costs, and semi-variable costs?

-Variable costs fluctuate in direct proportion to business activity, such as raw materials and direct labor. Fixed costs remain constant regardless of activity levels, like salaries or rent. Semi-variable costs change with business activity but not in direct proportion, such as utilities or maintenance costs.

How are direct materials and direct labor related to the concept of prime costs?

-Direct materials and direct labor are combined to form prime costs. Prime costs are the fundamental expenses directly associated with producing a product, excluding other indirect expenses like overhead.

What are manufacturing costs and how are they classified?

-Manufacturing costs consist of direct materials, direct labor, and factory overhead. Factory overhead includes indirect materials, indirect labor, and other indirect costs necessary for production, such as utilities or factory maintenance.

How do overhead costs relate to production and non-production activities?

-Overhead costs are typically part of manufacturing or production activities and include indirect costs like factory rent, utilities, and machine maintenance. Non-production overheads include costs such as administrative expenses and marketing.

What are the main types of costs when classified by the relationship with production volume?

-The main types of costs classified by production volume are variable costs, fixed costs, and semi-variable costs. Variable costs change with the level of production, fixed costs remain constant regardless of production volume, and semi-variable costs vary but not proportionally with production.

How do you calculate the cost per unit for a product?

-To calculate the cost per unit, divide the total cost of materials, labor, and overhead by the number of units produced. This allows businesses to determine the cost per product, which is essential for pricing and profitability analysis.

Outlines

此内容仅限付费用户访问。 请升级后访问。

立即升级Mindmap

此内容仅限付费用户访问。 请升级后访问。

立即升级Keywords

此内容仅限付费用户访问。 请升级后访问。

立即升级Highlights

此内容仅限付费用户访问。 请升级后访问。

立即升级Transcripts

此内容仅限付费用户访问。 请升级后访问。

立即升级浏览更多相关视频

5.0 / 5 (0 votes)