Anggaran Persediaan

Summary

TLDRIn this video, Pak Subhanallah discusses inventory management, focusing on budgeting for inventory. He explains the necessity of inventory budgets due to various associated costs and illustrates how to prepare inventory budgets for finished goods in a manufacturing company. Using PT Mutiara as an example, he details calculating inventory levels, stability of product output, and projecting inventory in financial terms. He also covers methods to account for variable and fixed costs, and concludes with a profit analysis for the first quarter of 2015.

Takeaways

- 📈 Management of inventory requires careful budgeting due to high associated costs.

- 📊 An inventory budget helps determine the necessary expenses for maintaining stock in a company.

- 🏭 In manufacturing companies, inventory includes finished products, products in process, raw materials, and supplies.

- 🔄 Inventory levels can be managed by determining the turnover rate and setting a budget.

- 📅 Example: PT Mutiara has data showing 1000 units in January and 3000 units in March, with 6000 units in three months.

- 🛠️ Stability in product inventory is crucial; the company plans to maintain consistent levels each month.

- 💡 The inventory at the end of January becomes the starting inventory for February, and so on.

- 💰 Budgeting in monetary terms involves knowing the cost per unit and accounting for variable and fixed expenses.

- 🧮 Example calculations show the total cost of inventory and the contribution margin for each month.

- 🔧 Inventory in process and finished products are budgeted separately, ensuring all stages of production are covered.

Q & A

What is the main topic discussed in the video?

-The main topic discussed in the video is inventory management, specifically focusing on inventory budgeting.

Why is an inventory budget necessary?

-An inventory budget is necessary because managing inventory involves many costs that need to be accounted for from the beginning.

What does the inventory budget include?

-The inventory budget includes costs for finished products, work-in-process inventory, raw materials, auxiliary materials, and supplies.

How can the budget for finished goods inventory be determined?

-The budget for finished goods inventory can be determined by either setting the inventory turnover rate or creating a budget based on inventory data.

What example is provided to illustrate inventory budgeting?

-The example provided is PT Mutiara's inventory data for January to March, illustrating the calculation of the budget for the ending inventory of finished goods.

How is the average monthly finished goods inventory calculated?

-The average monthly finished goods inventory is calculated by dividing the total finished goods inventory over three months by three.

What is the role of inventory stability in budgeting?

-Inventory stability is important in budgeting as it ensures that the production and inventory levels are evenly distributed over the period.

What are the components of the budget for finished goods in terms of costs?

-The components include the cost of goods sold, variable operating expenses, and fixed operating expenses.

How is the budget for work-in-process inventory calculated?

-The budget for work-in-process inventory is calculated using the initial inventory data, the cost of raw materials, direct labor costs, and overhead costs.

What conclusion is reached about PT Mutiara's performance in the first quarter?

-PT Mutiara broke even in the first quarter, with total sales matching total costs, resulting in no profit or loss.

Outlines

This section is available to paid users only. Please upgrade to access this part.

Upgrade NowMindmap

This section is available to paid users only. Please upgrade to access this part.

Upgrade NowKeywords

This section is available to paid users only. Please upgrade to access this part.

Upgrade NowHighlights

This section is available to paid users only. Please upgrade to access this part.

Upgrade NowTranscripts

This section is available to paid users only. Please upgrade to access this part.

Upgrade NowBrowse More Related Video

Audit atas Persediaan

3 Types of Inventory (Raw Materials, WIP, and Finished Goods)

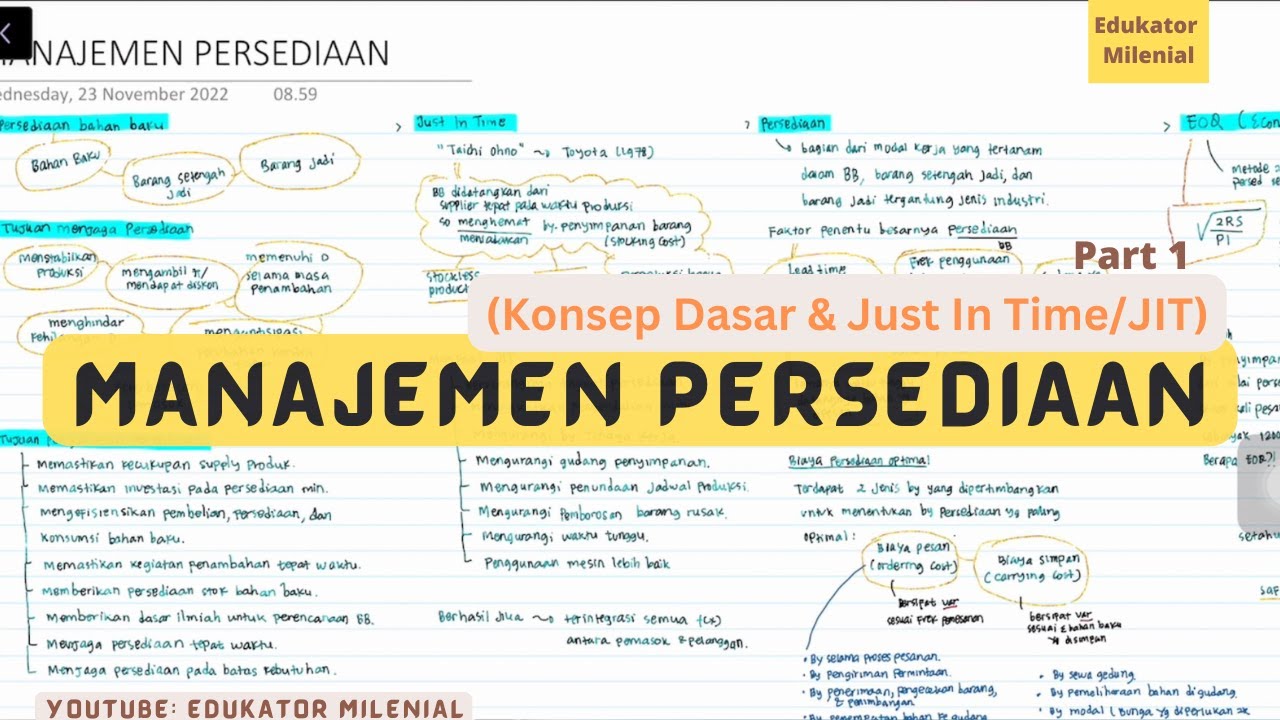

Manajemen Persediaan (Just In Time - JIT)

E learning : Manajemen Operasional - Sesi 8, Manajemen Persediaan | by Siti Mariam

AKM 1: 5-4 Goods and costs included in inventory

UAE VAT Complete Course | VAT Accounting Tutorial | Value Added Tax Training

5.0 / 5 (0 votes)