Metode Asinkronus P-11: Pemajakan Atas Laba Penerbangan dan Pelayaran MK Perpajakan Internasional

Summary

TLDRIn this video, Ibu Ida discusses international tax regulations related to shipping and aviation companies, focusing on income tax (PPh Pasal 15). She explains the complexities of tax rates, the determination of taxable income, and the specific treatments for foreign shipping and airline companies. The presentation covers various scenarios including joint ventures, ticket sales, cargo transport, and charter services, offering insights into the taxation of companies engaged in international transportation. Ibu Ida also highlights various models like the OECD and UN tax models, providing clarity on tax rights for countries involved in cross-border operations.

Takeaways

- 😀 The video discusses international tax rules regarding income from shipping and aviation companies operating in Indonesia.

- 😀 Corporate tax (PPh) for international shipping and aviation companies is governed by specific agreements between countries, such as Indonesia's treaties with other nations.

- 😀 International traffic taxation involves determining how taxes are split between the country of domicile and the country of origin of the transport services.

- 😀 There are two main types of international transport routes: regular (fixed schedules) and free (irregular routes with flexible destinations).

- 😀 The tax rate for foreign shipping and aviation companies operating in Indonesia is 2.4% of gross revenue, and this is considered a final tax.

- 😀 The process for withholding tax involves the charterer (payer) deducting the tax before payment, issuing a tax slip, and depositing the tax with the relevant tax authority.

- 😀 In certain international agreements, such as the Indonesia-Singapore agreement, the country of domicile has the right to tax air transport, while sea transport is taxed by the country of origin.

- 😀 Tax laws related to international transport services differentiate between types of transport contracts, including time charter, voyage charter, and bareboat charter.

- 😀 International tax treaties typically offer tax reductions for shipping and aviation services, with reductions such as 50% of the tax applied for sea transport in certain cases.

- 😀 The lecture also discusses the importance of clear agreements between parties in the shipping industry, including terms like cargo volume, loading/unloading schedules, and rental fees.

- 😀 Students are encouraged to summarize the lecture's key points and engage by commenting on a dedicated platform, demonstrating their understanding of the material.

Q & A

What is the focus of the script in terms of international taxation?

-The script primarily focuses on the taxation of companies involved in international maritime and aviation operations, discussing tax rules for shipping and air transport companies under Indonesian law, specifically Article 15 of the tax code (PPh Pasal 15).

What are the key areas covered regarding international shipping and aviation taxation?

-The script covers taxation on the profits of international shipping and aviation companies, including tax rates, operational rules for international transport, and specific tax treatment for companies operating under different types of charter agreements.

What is Article 15 of the Indonesian tax code about?

-Article 15 of the Indonesian tax code deals with the taxation of income from the operation of ships and aircraft involved in international transport, specifically outlining the rights of taxation between the country of domicile and the source country.

What is the significance of the term 'international traffic' in the context of the script?

-'International traffic' refers to the transportation of goods or passengers by ships or aircraft between countries, which determines how income from these operations is taxed under international agreements between countries, such as the agreement between Indonesia and other nations.

How is tax applied differently to air transport and maritime transport?

-For air transport, taxes are typically imposed by the country of domicile of the airline, whereas maritime transport taxes are imposed by the source country of the shipping operation. However, tax rates can be adjusted based on international agreements.

What are the different types of charter agreements discussed in the script?

-The script mentions three types of charter agreements: time charter, voyage charter, and bareboat charter. Each type varies in the terms of ship rental, with time charter based on a fixed duration, voyage charter on a specific journey, and bareboat charter involving renting the vessel without crew or supplies.

What is the tax rate applied to international shipping and aviation companies in Indonesia?

-The tax rate applied to international shipping and aviation companies in Indonesia is 2.6% of the gross income, which is considered final tax, meaning it is a one-time tax payment upon earnings.

How should a charterer handle tax deductions and payments?

-A charterer must withhold the tax at the time of payment for the charter service, provide a tax deduction certificate to the service provider, deposit the tax to the relevant bank or post office by the 10th of the following month, and report it to the tax office by the 20th.

What is the role of international agreements in the taxation of maritime and air transport companies?

-International agreements, such as the agreements between Indonesia and other countries, determine the allocation of tax rights between countries for income derived from international transport operations. These agreements often include provisions for tax reductions or exemptions, such as the 50% reduction in tax for maritime transport income in some cases.

What are the main points in the OECD and UN models for taxing international transport companies?

-Under the OECD model, income from international transport operations is generally taxed only in the country where the company’s management is effectively located. The UN model offers two options: tax can be imposed either by the source country or the country of domicile, allowing more flexibility in tax jurisdiction.

Outlines

This section is available to paid users only. Please upgrade to access this part.

Upgrade NowMindmap

This section is available to paid users only. Please upgrade to access this part.

Upgrade NowKeywords

This section is available to paid users only. Please upgrade to access this part.

Upgrade NowHighlights

This section is available to paid users only. Please upgrade to access this part.

Upgrade NowTranscripts

This section is available to paid users only. Please upgrade to access this part.

Upgrade NowBrowse More Related Video

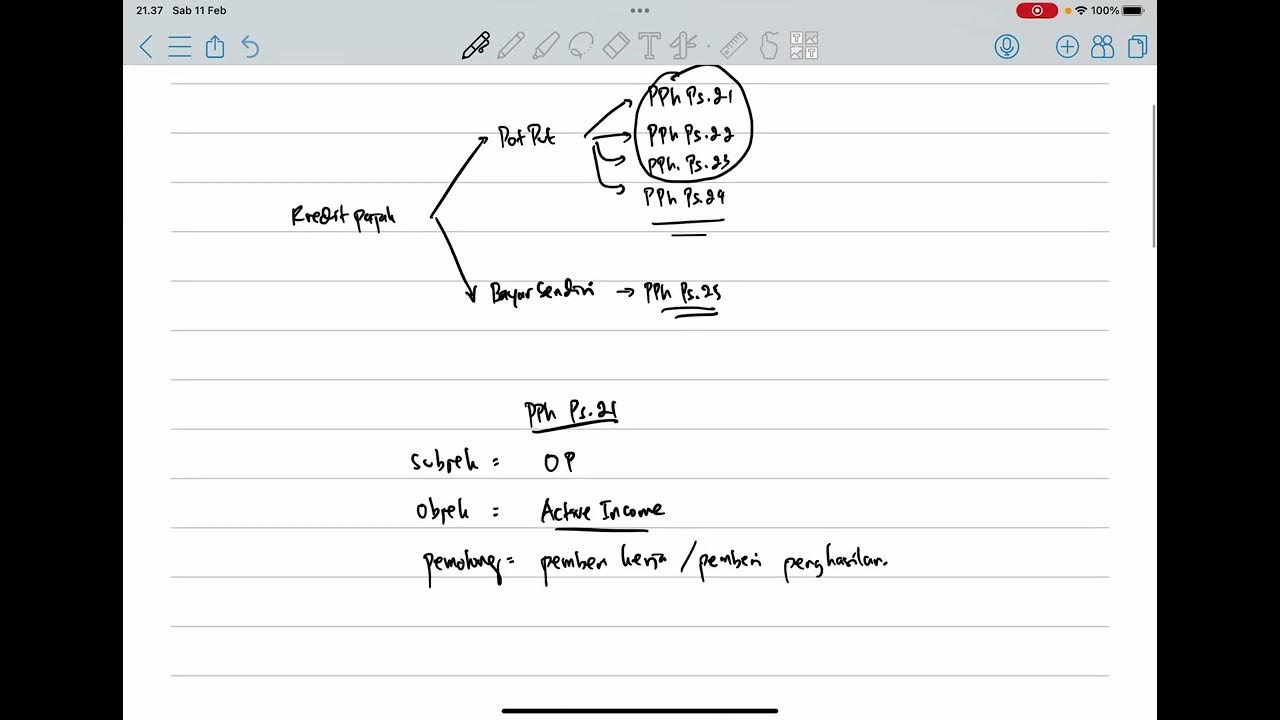

PPh Orang Pribadi (Update 2023) - 5. Kredit Pajak

2 PPh Pasal 4 ayat 2 : Objek, Pelunasan, Pelaporan

E-FUNLEARNING HMAK: PERPAJAKAN PPH PASAL 28 DAN 29

Konsep dan Penghitungan PPh Pasal 23

Menghitung Pajak Penghasilan Pasal 21 || Materi Ekonomi Kelas XI

MENGENAL PPH 21 LEBIH DEKAT AGAR TIDAK SALAH PAHAM DENGAN PERUSAHAAN ANDA

5.0 / 5 (0 votes)