Biaya Tenaga Kerja

Summary

TLDRThis video script delves into the concept of labor costs in manufacturing, focusing on the classification and accounting treatment of direct and indirect labor. It outlines the distinction between production, marketing, and administrative labor costs, explaining how each category is recorded in financial accounts. The script further discusses the journal entries required for recording wages, tax payments, and the allocation of labor costs across departments. Aimed at educating viewers on cost management, it provides clear examples and practical steps for accurate financial reporting in manufacturing companies.

Takeaways

- 😀 Labor costs are divided into direct labor (BTKL) and indirect labor (PTKL) based on their involvement in production.

- 😀 Direct labor (BTKL) includes employees who directly transform raw materials into finished goods.

- 😀 Indirect labor (PTKL) consists of employees who do not directly participate in production, such as supervisors or foremen.

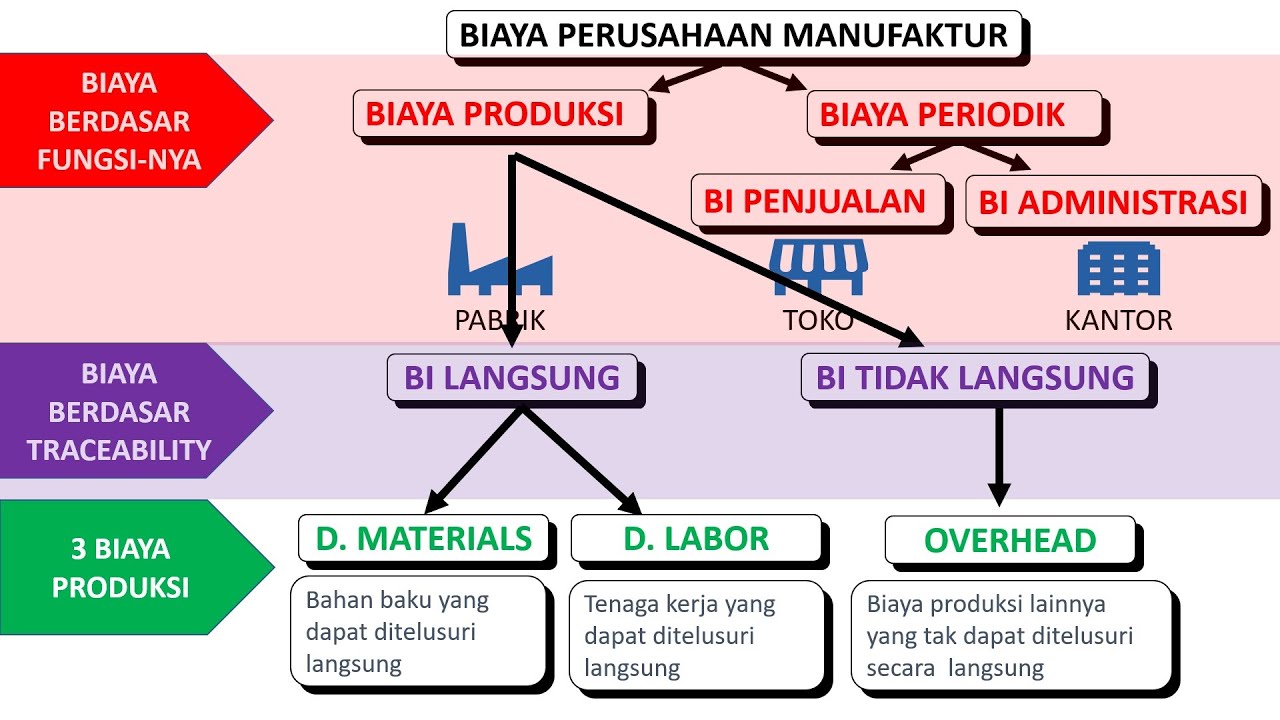

- 😀 Labor costs are classified by company function into production, marketing, and administration & general expenses.

- 😀 Components of labor costs include basic salary, overtime, and allowances related to work performance.

- 😀 Recording labor costs involves four key steps: recording wages, paying wages, remitting employee taxes, and allocating costs appropriately.

- 😀 Wages and salaries are initially recorded as liabilities (payable) before payment is made.

- 😀 Employee income tax (PPH 21) may either be borne by the company (added to overhead) or deducted from employees’ salaries.

- 😀 Proper allocation of labor costs ensures that direct labor goes to production cost, indirect labor goes to factory overhead, and other labor costs go to marketing or administration expenses.

- 😀 The ultimate goal of labor cost recording and allocation is to reduce wage and salary balances to zero for accurate posting to the general ledger.

Q & A

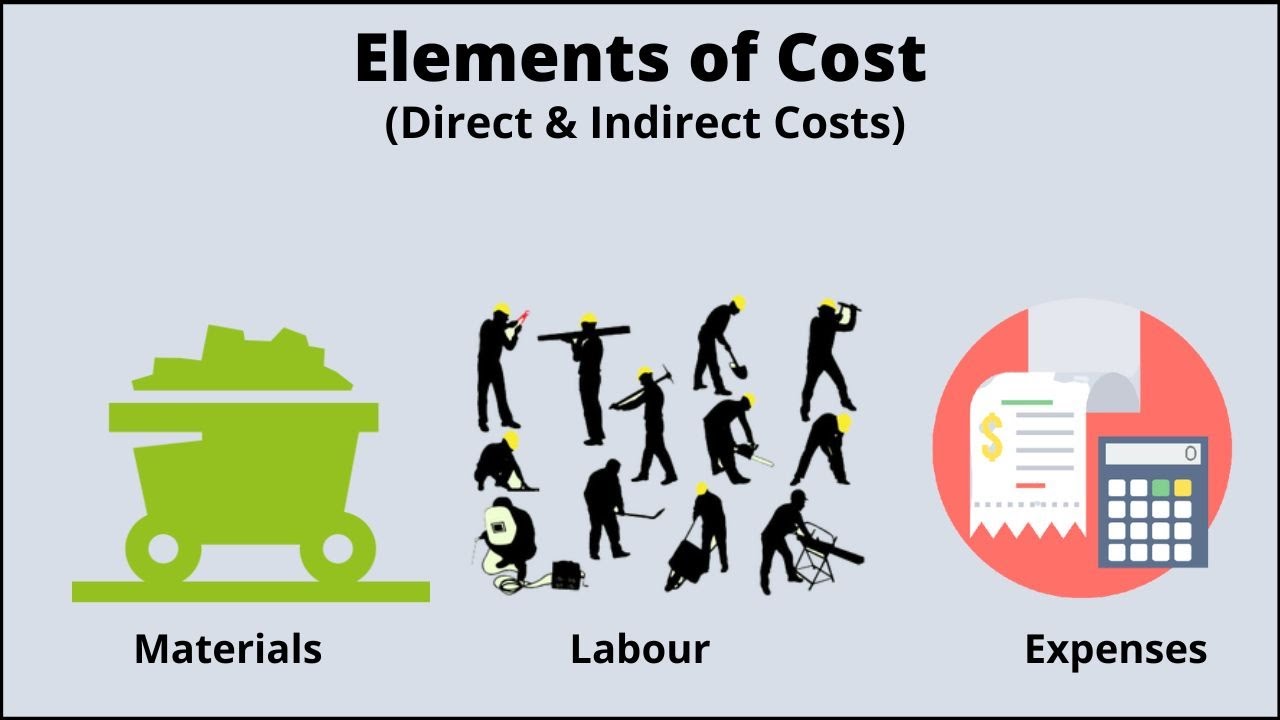

What are the three main components of production costs discussed in the video?

-The three main components are: 1) Raw material costs, 2) Labor costs, and 3) Factory overhead costs.

How is 'labor' defined in the context of production?

-Labor refers to the physical employees who directly work on transforming raw materials into finished goods.

What is meant by 'labor cost'?

-Labor cost is the monetary cost associated with labor, usually calculated based on direct working hours multiplied by the wage rate.

What is the difference between direct labor (BTKL) and indirect labor (PTK)?

-Direct labor (BTKL) involves employees directly handling the production process, while indirect labor (PTK) includes employees who do not directly engage in production, such as supervisors or maintenance staff.

How are labor costs categorized based on company functions?

-Labor costs are categorized into three main functions: production, marketing, and administrative/general functions.

What are the four steps in recording labor costs according to the video?

-1) Record salaries and wages in a journal, 2) Pay salaries and wages, 3) Pay employee income tax (PPh), 4) Classify labor costs into direct labor, indirect labor, administrative, and marketing costs.

How is PPh (employee income tax) treated in labor cost accounting?

-If the company does not pay PPh, it is deducted from employees’ salaries. If the company pays PPh, it is included in factory overhead costs (BOP).

What are the components included in labor cost calculation?

-Components include base salary, overtime pay, and allowances or benefits related to work.

Why is it important to differentiate BTKL from PTK when calculating production costs?

-Differentiating BTKL from PTK ensures accurate cost allocation: BTKL is included in production cost, while PTK is part of overhead, which affects product costing and pricing decisions.

What happens to labor cost balances after journal entries are recorded and classified?

-After proper journal entries and classification, the balances for salaries and wages accounts should be zero, indicating all costs have been allocated appropriately.

How are labor costs allocated for departments like production, services, marketing, and administration?

-Direct labor (BTKL) is allocated to production or service departments. Indirect labor (PTK) is allocated to factory overhead. Salaries for marketing and administrative staff are allocated to marketing costs and administrative/general expenses, respectively.

What practical examples were used in the video to illustrate labor cost recording?

-The video used data from PT X and PT Wijaya, showing the breakdown of salaries and wages for production, marketing, and administration departments, as well as handling of PPh 21 taxes.

Outlines

Этот раздел доступен только подписчикам платных тарифов. Пожалуйста, перейдите на платный тариф для доступа.

Перейти на платный тарифMindmap

Этот раздел доступен только подписчикам платных тарифов. Пожалуйста, перейдите на платный тариф для доступа.

Перейти на платный тарифKeywords

Этот раздел доступен только подписчикам платных тарифов. Пожалуйста, перейдите на платный тариф для доступа.

Перейти на платный тарифHighlights

Этот раздел доступен только подписчикам платных тарифов. Пожалуйста, перейдите на платный тариф для доступа.

Перейти на платный тарифTranscripts

Этот раздел доступен только подписчикам платных тарифов. Пожалуйста, перейдите на платный тариф для доступа.

Перейти на платный тарифПосмотреть больше похожих видео

Biaya Tenaga Kerja Dlm Akuntansi Biaya

Konsep Dasar Akuntansi Biaya dan Akuntansi Manajerial

(FACIL) Materiales Directos, Mano de Obra Directa, Costos Indirectos de Fábrica

Akuntansi untuk Tenaga Kerja part 1

1. Gr 11 Accounting - Manufacturing - Activity 1

Elements of cost | Direct and Indirect: Material, Labor, & Expenses

5.0 / 5 (0 votes)