Laporan Keuangan Organisasi Non Laba Sesuai ISAK 35

Summary

TLDRIn this video, the speaker explains the financial reporting standards for non-profit organizations under ISAK 35, which replaces PSAK 45. The new standards, effective from January 2020, provide a clearer framework for reporting, emphasizing transparency in financial statements for entities like foundations, NGOs, and private universities. Key elements include five main reports: the statement of financial position, comprehensive income, changes in net assets, cash flows, and notes. The video guides viewers through these updates, showing how they ensure accurate, consistent financial reporting aligned with general accounting principles, and invites viewers for further insights in upcoming videos.

Takeaways

- 😀 ISAK 35 is an interpretation of accounting standards for non-profit organizations, effective from January 1, 2020, replacing PSAK 45.

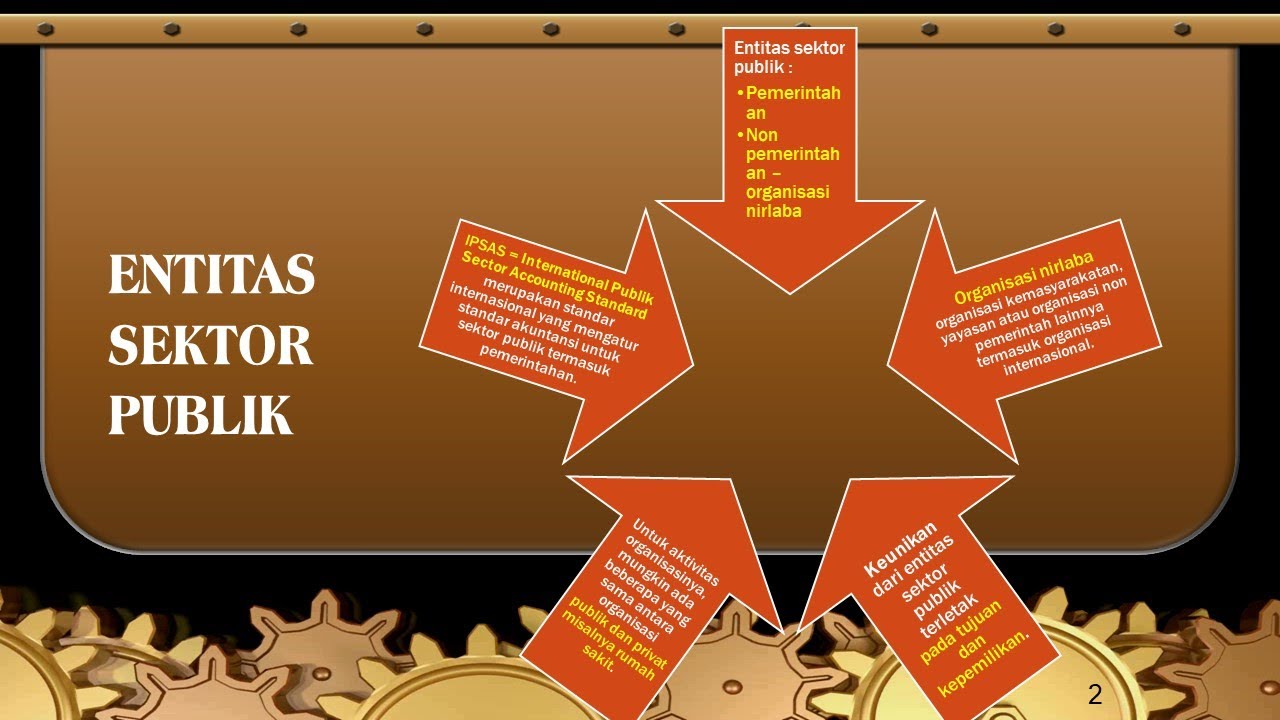

- 😀 Non-profit organizations such as foundations, hospitals, LSMs, and private universities must now follow ISAK 35 for financial reporting.

- 😀 ISAK 35 requires non-profit organizations to present financial statements that reflect their unique characteristics, including no profit distribution to owners.

- 😀 The key financial statements under ISAK 35 for non-profits include: Statement of Financial Position, Statement of Comprehensive Income, Statement of Changes in Net Assets, Statement of Cash Flows, and Notes to Financial Statements.

- 😀 ISAK 35 ensures that non-profit organizations follow PSAK 1 and other relevant PSAK guidelines for preparing financial statements.

- 😀 Non-profits are categorized based on the size of the organization, with larger entities required to use full PSAK and classify equity in financial statements.

- 😀 A fundamental difference from PSAK 45 is the number and type of reports: ISAK 35 requires five reports versus PSAK 45’s four reports.

- 😀 The Statement of Financial Position provides details on assets, liabilities, and net assets, giving a snapshot of the organization’s financial condition.

- 😀 The Statement of Comprehensive Income shows changes in net assets due to transactions and other events, helping to track resource use in various programs.

- 😀 The Statement of Changes in Net Assets classifies net assets into unrestricted and restricted categories, reflecting resource limitations imposed by donors.

- 😀 The Cash Flow Statement tracks the movement of cash in and out of the organization, classified by operating, investing, and financing activities.

- 😀 Notes to the Financial Statements include detailed disclosures about the accounting policies and any additional required information not presented in the main statements.

Q & A

What is ISAK 35 and when did it come into effect?

-ISAK 35 is the Indonesian Financial Accounting Standards Interpretation that governs the presentation of financial statements for non-profit entities. It was enacted in September 2018 and came into effect on January 1, 2020.

What non-profit organizations are impacted by ISAK 35?

-ISAK 35 applies to various non-profit organizations, including foundations, associations, schools, hospitals, NGOs, and private universities.

What are the key characteristics of non-profit entities according to ISAK 35?

-Non-profit entities are characterized by receiving resources from donors without the expectation of repayment or economic benefits, generating goods or services without a profit motive, and not distributing profits to founders or owners.

How does ownership differ in non-profit organizations compared to businesses?

-Non-profit organizations do not have ownership shares like businesses. Ownership cannot be sold or transferred, and it does not entitle anyone to a share of the organization's assets upon liquidation.

What were the challenges with PSAK 45 before the introduction of ISAK 35?

-PSAK 45 was confusing because it had different financial reporting formats for non-profit entities within the same tier of standards, leading to inconsistencies in how financial statements were prepared.

What is the main change introduced by ISAK 35 compared to PSAK 45?

-ISAK 35 introduces a more structured and standardized format for non-profit financial statements, replacing PSAK 45. It includes five key financial statements instead of the previous four.

What are the five financial statements required under ISAK 35?

-The five financial statements under ISAK 35 are: 1) Statement of Financial Position, 2) Statement of Comprehensive Income, 3) Statement of Changes in Net Assets, 4) Statement of Cash Flows, and 5) Notes to Financial Statements.

What is the purpose of the Statement of Financial Position in ISAK 35?

-The Statement of Financial Position presents information about an organization's assets, liabilities, and net assets at a specific point in time, helping assess the financial health of the organization.

What is the role of the Statement of Comprehensive Income?

-The Statement of Comprehensive Income reports on the impact of transactions and events on the net assets of a non-profit entity, showing changes in the value of assets and liabilities.

How does ISAK 35 treat net assets in non-profit organizations?

-ISAK 35 classifies net assets into two categories: 1) net assets without donor restrictions and 2) net assets with donor restrictions. This classification helps track the usage of funds in different programs and services.

Outlines

Этот раздел доступен только подписчикам платных тарифов. Пожалуйста, перейдите на платный тариф для доступа.

Перейти на платный тарифMindmap

Этот раздел доступен только подписчикам платных тарифов. Пожалуйста, перейдите на платный тариф для доступа.

Перейти на платный тарифKeywords

Этот раздел доступен только подписчикам платных тарифов. Пожалуйста, перейдите на платный тариф для доступа.

Перейти на платный тарифHighlights

Этот раздел доступен только подписчикам платных тарифов. Пожалуйста, перейдите на платный тариф для доступа.

Перейти на платный тарифTranscripts

Этот раздел доступен только подписчикам платных тарифов. Пожалуйста, перейдите на платный тариф для доступа.

Перейти на платный тарифПосмотреть больше похожих видео

5.0 / 5 (0 votes)