Microeconomics Unit 3 COMPLETE Summary - Production & Perfect Competition

Summary

TLDRIn this microeconomics tutorial, Jer Breed explores production functions, marginal products, and costs for firms in perfectly competitive markets. The video covers the law of diminishing marginal returns, fixed and variable costs, and how they influence total costs. It explains the calculation of marginal cost, average costs, and how they intersect with marginal revenue for profit maximization. The tutorial also discusses long-term cost implications, economic vs. accounting profit, and how firms adjust to market changes to reach long-run equilibrium, emphasizing efficiency in perfectly competitive markets.

Takeaways

- 📊 The production function shows the relationship between the quantity of labor hired and the output produced, with diminishing marginal returns setting in as more workers are hired.

- 📈 Marginal product increases initially due to specialization, then decreases, and can eventually become negative as more workers are added.

- 💸 Fixed costs remain constant regardless of output, while variable costs increase as production increases; total costs are the sum of fixed and variable costs.

- 📉 Marginal cost is calculated as the change in total cost divided by the change in output and typically forms a U-shape on a graph.

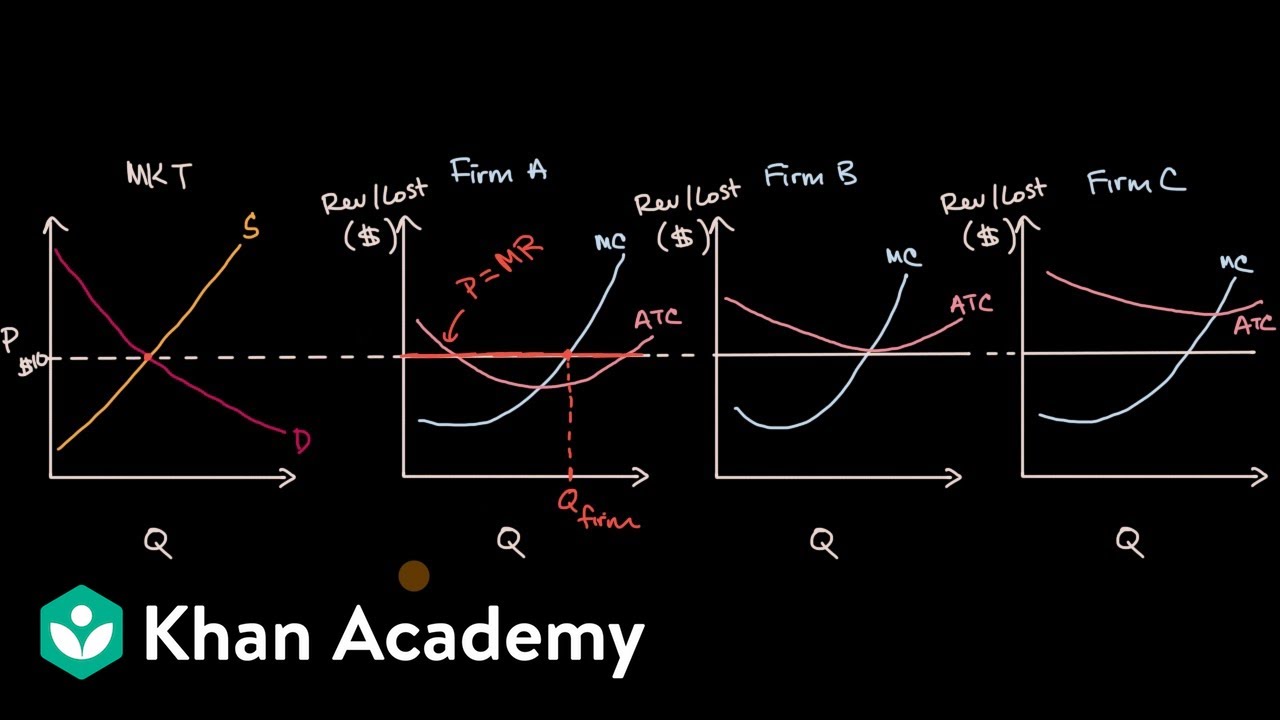

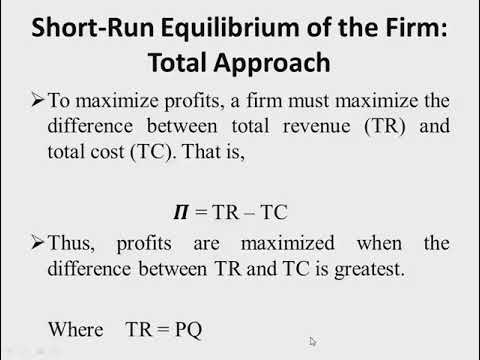

- ⚖️ Firms aim for profit maximization where marginal revenue equals marginal cost; this is the point at which producing more units is no longer profitable.

- 🏷️ In a perfectly competitive market, firms are price takers, selling identical products, with zero economic profit in the long run.

- 🔄 Long run costs involve all costs being variable, allowing businesses to change their production capacity by expanding factories or hiring more labor.

- 📉 Economies of scale allow firms to reduce average costs as they expand, while diseconomies of scale lead to higher costs as firms grow too large.

- 🧮 Economic profit considers both explicit and implicit costs, with zero economic profit known as normal profit.

- ⚙️ Perfectly competitive firms are both allocatively and productively efficient in the long run, producing at the lowest average total cost.

Q & A

What is the production function in microeconomics?

-A production function shows the relationship between the quantity of labor a firm hires and the quantity of output produced by that labor. It illustrates how changes in labor affect total output.

What are the three phases of the law of diminishing marginal returns?

-The three phases are: 1) Increasing returns: Marginal product rises as specialization occurs. 2) Diminishing returns: Marginal product falls but remains positive. 3) Negative returns: Marginal product becomes negative, decreasing total output.

How is marginal product calculated?

-Marginal product is calculated by taking the change in total product and dividing it by the change in labor quantity. Since the change in labor is usually one worker, it equals the change in total product due to hiring an additional worker.

What is the difference between fixed costs and variable costs?

-Fixed costs do not change with output, such as capital and land. Variable costs, like labor and electricity, change with the quantity of output produced.

What does the marginal cost curve represent, and how is it related to marginal product?

-The marginal cost curve shows the cost of producing one additional unit of output. It is inversely related to marginal product; when marginal product rises, marginal cost falls, and when marginal product falls, marginal cost rises.

What is the relationship between marginal cost and average cost curves?

-The marginal cost curve intersects the average variable cost and average total cost curves at their lowest points. When marginal cost is below the average cost, the average cost is falling. When it’s above, the average cost is rising.

What is the concept of productive efficiency?

-Productive efficiency occurs when a firm produces at the lowest possible average cost. This happens at the minimum point of the average total cost curve, known as the productively efficient quantity.

How are economic profit and accounting profit different?

-Accounting profit is calculated by subtracting explicit costs from total revenue. Economic profit also subtracts implicit costs (opportunity costs) from total revenue, making it a lower figure than accounting profit.

What is the profit-maximizing rule for firms?

-Firms maximize profit by producing at the quantity where marginal revenue equals marginal cost. This ensures that the firm is not producing too much (increasing costs) or too little (missing out on revenue).

What are the characteristics of a perfectly competitive market?

-In a perfectly competitive market, there are many firms selling identical products, with no influence on price (price takers), low barriers to entry, and zero economic profit in the long run due to competition.

Outlines

Этот раздел доступен только подписчикам платных тарифов. Пожалуйста, перейдите на платный тариф для доступа.

Перейти на платный тарифMindmap

Этот раздел доступен только подписчикам платных тарифов. Пожалуйста, перейдите на платный тариф для доступа.

Перейти на платный тарифKeywords

Этот раздел доступен только подписчикам платных тарифов. Пожалуйста, перейдите на платный тариф для доступа.

Перейти на платный тарифHighlights

Этот раздел доступен только подписчикам платных тарифов. Пожалуйста, перейдите на платный тариф для доступа.

Перейти на платный тарифTranscripts

Этот раздел доступен только подписчикам платных тарифов. Пожалуйста, перейдите на платный тариф для доступа.

Перейти на платный тарифПосмотреть больше похожих видео

Microeconomics Unit 5 COMPLETE Summary - Factor Markets

Long run supply when industry costs are increasing or decreasing | Microeconomics | Khan Academy

Perfect Competition- Microeconomics 3.7

Economic profit for firms in perfectly competitive markets | Microeconomics | Khan Academy

Market Structure Part 1: Introduction

Long-run economic profit for perfectly competitive firms | Microeconomics | Khan Academy

5.0 / 5 (0 votes)