Benarkah Bank syariah hanya kedok? - Ustadz Dr Erwandi Tarmizi LC, MA

Summary

TLDRThe transcript discusses concerns about the authenticity of Islamic banking in Indonesia, questioning whether many Islamic banks are truly Sharia-compliant or just using the label. The speaker critiques the similarity between Islamic and conventional banks, pointing out how both often operate with similar financial models, such as home loans with added charges, disguised as 'margins' or 'delayed payment penalties.' The speaker advocates for a deeper understanding of Sharia principles, urging Muslims to seek genuine Sharia-compliant banking practices that focus on fairness, risk-sharing, and transparency.

Takeaways

- 😀 There is skepticism regarding the authenticity of many Islamic banks, with some questioning whether they genuinely operate according to Shariah principles or if they just use an Islamic label.

- 😀 A key concern is that Islamic banks often follow similar operational procedures as conventional banks, including charging margins instead of interest, which may still constitute riba (usury).

- 😀 The difference between Islamic and conventional banking often comes down to terminology, with terms like 'margin' used in place of 'interest,' but the underlying practices may still be the same.

- 😀 The speaker points out that some Islamic banking products, like home financing, work similarly to conventional mortgages, where the buyer still gets a house but with added costs, making the difference seem insignificant.

- 😀 There are concerns that penalties for late payments in Islamic banks, known as 'rahmatu takhir,' are essentially the same as late fees in conventional banking, further blurring the lines between the two systems.

- 😀 The speaker emphasizes the importance of understanding Islamic law (Syariah) in order to engage in truly Shariah-compliant financial transactions.

- 😀 Some individuals have attempted to design more authentic Shariah-compliant banking products, where transactions like home purchases are structured without any interest or penalties, ensuring they adhere to Islamic principles.

- 😀 Real-world examples of Shariah-compliant banking practices are shared, including cases of material purchasing and business ventures, which reveal inconsistencies in adherence to Shariah principles.

- 😀 A critical aspect of achieving truly Shariah-compliant banking is ensuring that the transactions are based on actual trade or ownership, as opposed to just money changing hands.

- 😀 The speaker concludes by stressing that if people understand and follow the requirements of Shariah, they can engage in financial transactions that are more in line with Islamic teachings, rather than simply relying on the labels or surface-level claims of banks.

Q & A

What is the main concern raised in the script about Islamic banking?

-The main concern is that many Islamic banks, despite claiming to be Shariah-compliant, often use practices similar to conventional banks, such as charging margins or penalties that resemble interest (riba). This raises doubts about the true adherence to Islamic principles.

How do Islamic banks and conventional banks appear similar, according to the speaker?

-According to the speaker, Islamic and conventional banks appear similar because both provide loans for home purchases, with the customer receiving either a product (a house) or money. Both systems also involve some form of financial increment, either through margin in Islamic banks or interest in conventional banks.

What example does the speaker give to illustrate the similarities between Islamic and conventional banks?

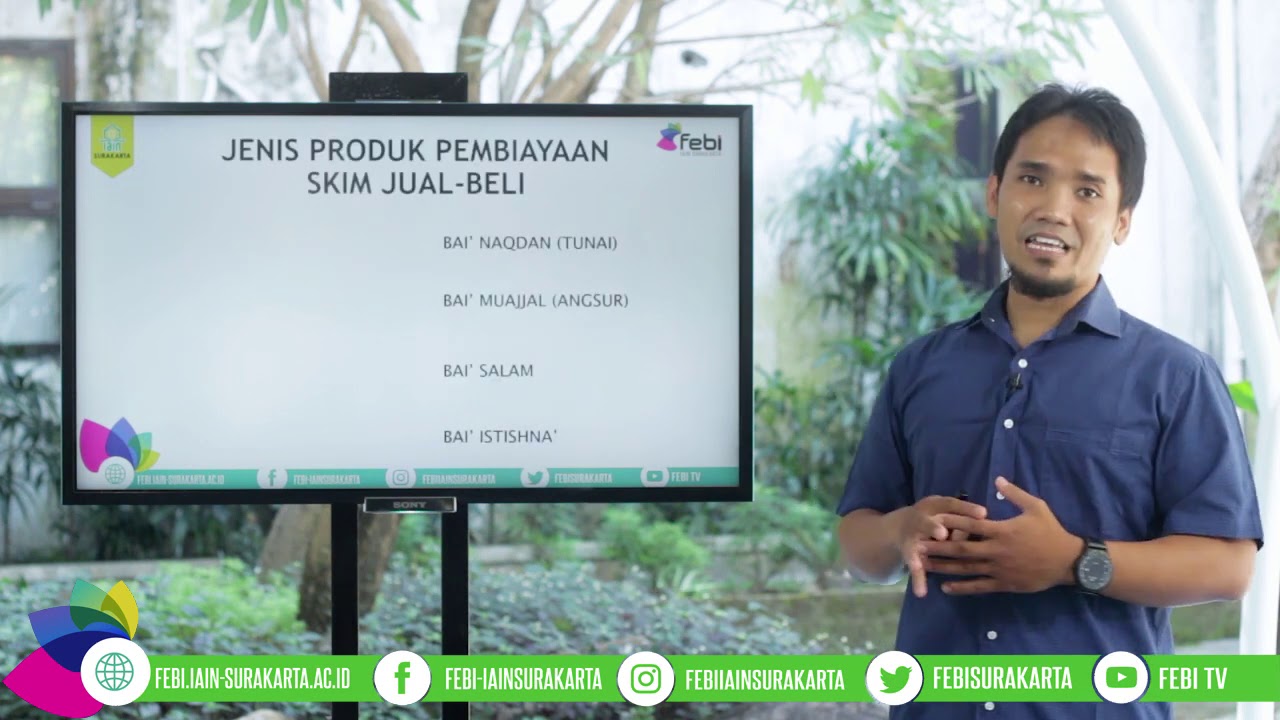

-The speaker explains that when purchasing a house, both Islamic and conventional banks provide the house with added costs. In conventional banks, this is called 'interest,' while in Islamic banks it is called 'margin,' but the concept and financial outcome are very similar.

What is the issue with the 'murabahah' contract offered by Islamic banks?

-The issue with the 'murabahah' contract is that while it is presented as Shariah-compliant, it often involves transactions that are not truly Islamic, such as the bank purchasing goods and reselling them at a markup, which can resemble interest-based transactions in practice.

Why does the speaker believe that the Muslim community may not fully understand the practices of Islamic banks?

-The speaker believes that many people in the Muslim community may not fully understand the true nature of Shariah-compliant banking and might simply accept the label 'Islamic' without questioning the practices behind it, which leads to a lack of proper scrutiny.

What does the speaker suggest as a solution for people who want to engage in genuine Shariah-compliant banking?

-The speaker suggests that individuals who want to engage in genuine Shariah-compliant banking should educate themselves about Islamic finance and consult with experts to ensure that the transactions align with Islamic principles, rather than just accepting superficial claims.

How does the speaker describe the relationship between Islamic and conventional banks in terms of penalties for late payments?

-The speaker explains that both Islamic and conventional banks charge penalties for late payments. In conventional banks, it is called a 'late fee' or 'interest,' whereas in Islamic banks, it is referred to as 'rahmatul takhir,' a term in Arabic that also implies a penalty for delay, making the distinction seem largely semantic.

What is the speaker’s stance on the legitimacy of 'margin' in Islamic banks?

-The speaker questions the legitimacy of 'margin' in Islamic banks, arguing that it functions very similarly to interest (riba) in conventional banking, thus undermining the claim of being genuinely Shariah-compliant.

What advice does the speaker give to someone wanting to follow a truly Shariah-compliant financial system?

-The speaker advises that one should seek out experts in Islamic finance and ask detailed questions about the financial practices being followed, ensuring that the transactions are truly Shariah-compliant and not just disguised as such for marketing purposes.

What personal experience does the speaker share involving Islamic banks and Shariah-compliant transactions?

-The speaker shares an experience where a friend was offered a 'murabahah' contract by an Islamic bank to purchase materials from Korea. Despite being labeled as Shariah-compliant, the transaction closely resembled conventional interest-based financing, leading the speaker to question the authenticity of such practices.

Outlines

Esta sección está disponible solo para usuarios con suscripción. Por favor, mejora tu plan para acceder a esta parte.

Mejorar ahoraMindmap

Esta sección está disponible solo para usuarios con suscripción. Por favor, mejora tu plan para acceder a esta parte.

Mejorar ahoraKeywords

Esta sección está disponible solo para usuarios con suscripción. Por favor, mejora tu plan para acceder a esta parte.

Mejorar ahoraHighlights

Esta sección está disponible solo para usuarios con suscripción. Por favor, mejora tu plan para acceder a esta parte.

Mejorar ahoraTranscripts

Esta sección está disponible solo para usuarios con suscripción. Por favor, mejora tu plan para acceder a esta parte.

Mejorar ahora

5.0 / 5 (0 votes)