Masuk Kelas | AUDIT SALDO KAS

Summary

TLDRThis video provides an in-depth guide to auditing cash and cash balances, focusing on kas kecil and kas besar used directly in company operations. It explains cash definitions, exclusions, and the importance of internal controls, including documentation, authorization, and bookkeeping. Common cash frauds such as check kiting and lapping are illustrated with practical examples. The video also outlines essential audit procedures, including preliminary analysis, substantive testing, bank confirmations, reconciliations, and proper financial reporting. Emphasizing accuracy, transparency, and fraud prevention, the session equips auditors with the knowledge to ensure cash is properly managed, reported, and safeguarded within a company's financial ecosystem.

Takeaways

- 😀 Cash is a critical company asset, easily misused due to its flexibility and direct involvement in company operations.

- 😀 The focus of this audit discussion is on cash that is immediately usable by the company, such as petty cash and main cash, not restricted or special-purpose cash.

- 😀 All business cycles—revenue, expenses, investments, payroll—ultimately involve cash, making its audit essential.

- 😀 Proper internal controls for cash include authorization, documentation, recording, bank deposit procedures, and maintenance of accurate financial reports.

- 😀 Common cash frauds include 'check kiting' (manipulating interbank transfers to inflate balances) and 'lapping' (using incoming cash to cover previous misappropriations).

- 😀 The auditor’s goal is to assess the valuation, allocation, presentation, and disclosure of cash in accordance with accounting standards.

- 😀 Effective audit requires understanding the client’s business, cash flow sources, internal control policies, and identifying unusual or high-risk transactions.

- 😀 Substantive testing involves procedures like reviewing documents, reconciling bank accounts, confirming balances with banks, and sampling transactions for verification.

- 😀 Analyzing ratios, comparing current period data to budgets or previous periods, and identifying anomalies helps auditors detect potential errors or fraud.

- 😀 Audit findings should result in proper reporting, adjustments, or disclosure recommendations to ensure accurate presentation of cash and financial health of the company.

- 😀 Maintaining accurate cash flow is a key indicator of a company’s financial health, and mismanagement can significantly impact operations.

Q & A

What is the primary focus of the video transcript?

-The primary focus is on auditing cash and cash balances, specifically understanding cash types, internal controls, common frauds, and procedures auditors follow to ensure accurate financial reporting.

Which types of cash are discussed in the transcript?

-The transcript discusses operational cash, which includes petty cash, cash on hand, and bank accounts like checking accounts. It excludes restricted cash like deposits, foreign currency cash with limitations, and cash reserved for obligations.

Why is cash considered a high-risk asset in companies?

-Cash is highly flexible and easily misused. It flows through all company activities, making it prone to errors or intentional fraud if internal controls are weak.

What are the main forms of cash fraud mentioned in the transcript?

-Two main forms are highlighted: Check Kiting, which involves manipulating interbank transfers to inflate balances temporarily, and Lapping, where cash receipts are misused and covered by subsequent receipts to hide shortages.

What are the key documents required for effective internal control of cash?

-Key documents include authorization forms for receipts and disbursements, execution evidence, bank deposit slips, journals, cash books, and cash flow statements, whether in manual or electronic form.

What steps should an auditor take in the preliminary phase of auditing cash?

-The auditor should understand the client’s business and industry, analyze cash flow points, assess internal controls, review relevant documents, compare current and prior periods, and identify unusual transactions.

How does an auditor perform substantive testing on cash transactions?

-Substantive testing involves sampling high-risk transactions, tracing transactions to supporting documentation, checking dates, performing bank reconciliations, and verifying the existence and accuracy of balances through confirmations.

What is the purpose of bank confirmations in cash auditing?

-Bank confirmations verify that the cash balances recorded by the company match the bank’s records, helping detect errors, fraud, or discrepancies in reported cash balances.

How does an auditor detect Check Kiting?

-By analyzing interbank transfers near period-end dates, the auditor checks for mismatches where funds are recorded in one bank but not deducted from the originating bank, which artificially inflates balances.

How is Lapping typically uncovered during an audit?

-Lapping is uncovered by comparing cash receipts against bank deposits over time, identifying discrepancies where earlier cash shortages are covered by subsequent receipts, often revealed through detailed tracing and analysis.

Why is proper classification and disclosure of cash important in financial reporting?

-Proper classification and disclosure ensure that financial statements comply with accounting standards, provide accurate information to stakeholders, and reflect the true liquidity and financial health of the company.

Why is auditing cash considered essential for assessing a company's financial health?

-Because cash is central to a company's operations and liquidity, auditing it ensures that cash flows are accurate, fraud is minimized, and the company’s ability to meet obligations and operate efficiently is accurately represented.

Outlines

Dieser Bereich ist nur für Premium-Benutzer verfügbar. Bitte führen Sie ein Upgrade durch, um auf diesen Abschnitt zuzugreifen.

Upgrade durchführenMindmap

Dieser Bereich ist nur für Premium-Benutzer verfügbar. Bitte führen Sie ein Upgrade durch, um auf diesen Abschnitt zuzugreifen.

Upgrade durchführenKeywords

Dieser Bereich ist nur für Premium-Benutzer verfügbar. Bitte führen Sie ein Upgrade durch, um auf diesen Abschnitt zuzugreifen.

Upgrade durchführenHighlights

Dieser Bereich ist nur für Premium-Benutzer verfügbar. Bitte führen Sie ein Upgrade durch, um auf diesen Abschnitt zuzugreifen.

Upgrade durchführenTranscripts

Dieser Bereich ist nur für Premium-Benutzer verfügbar. Bitte führen Sie ein Upgrade durch, um auf diesen Abschnitt zuzugreifen.

Upgrade durchführenWeitere ähnliche Videos ansehen

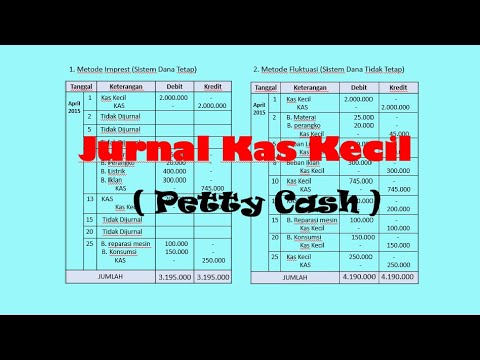

Kas kecil Metode Imprest dan Fluktuasi

SISTEM AKUNTANSI PENGELUARAN KAS || DAFS OFFICIAL

AKUNTANSI KEUANGAN MENENGAH - Bagian 2

Vid 04 Dokumen Transaksi 1

Auditing the CASH account - tests of controls and substantive testing

Bagaimana Cara Input Kas Masuk & Keluar di IPOS Laundry?? Cek Caranya di Sini! #laundry #tutorial

5.0 / 5 (0 votes)