AKM I.1. Kerangka Konseptual Pelaporan Keuangan

Summary

TLDRIn this video, Choirunnisa Arifa introduces the fundamental concepts of the conceptual framework for financial reporting. The lecture explains the purpose of financial reporting, the qualitative characteristics of accounting information, and the key elements in financial statements. It also covers the basic assumptions and principles of accounting, including recognition, measurement, and disclosure requirements. The video emphasizes the importance of consistency, relevance, and reliability in financial information for decision-making by investors, creditors, and other stakeholders. It serves as a foundational guide for understanding how financial statements are structured and analyzed.

Takeaways

- 😀 The conceptual framework of financial reporting is a fundamental guide for preparing consistent and useful financial statements.

- 😀 The main goal of financial reporting is to provide useful information for decision-making by investors, creditors, and other stakeholders.

- 😀 The financial statements should be accessible to the general public, ensuring that investors and creditors have equal access to useful information.

- 😀 Financial reporting is built on the concept of qualitative characteristics such as relevance, faithful representation, comparability, and understandability.

- 😀 Relevant financial information helps users make informed decisions, with key components including predictive value, confirmatory value, and materiality.

- 😀 Faithful representation requires financial data to be complete, neutral, and error-free to reflect the true financial condition of the company.

- 😀 Additional qualitative characteristics include verifiability, timeliness, and the ability to compare financial information across similar entities.

- 😀 The five key elements of financial statements are assets, liabilities, equity, revenue, and expenses, each playing a role in constructing the financial position and performance of the entity.

- 😀 Assumptions in financial reporting include economic entity assumption, going concern assumption, monetary unit assumption, periodicity assumption, and accrual basis assumption.

- 😀 The recognition and measurement principles include historical cost (for asset valuation), fair value (for market-based asset/liability values), and full disclosure of relevant information.

- 😀 Financial statements must disclose enough information for users to make well-informed decisions and assess the entity’s financial performance.

Q & A

What is the main purpose of the conceptual framework for financial reporting?

-The main purpose of the conceptual framework is to provide a foundation for the development and consistency of financial reporting standards. It helps ensure that financial reports are prepared using fundamental concepts that align with the needs of users, such as investors and creditors.

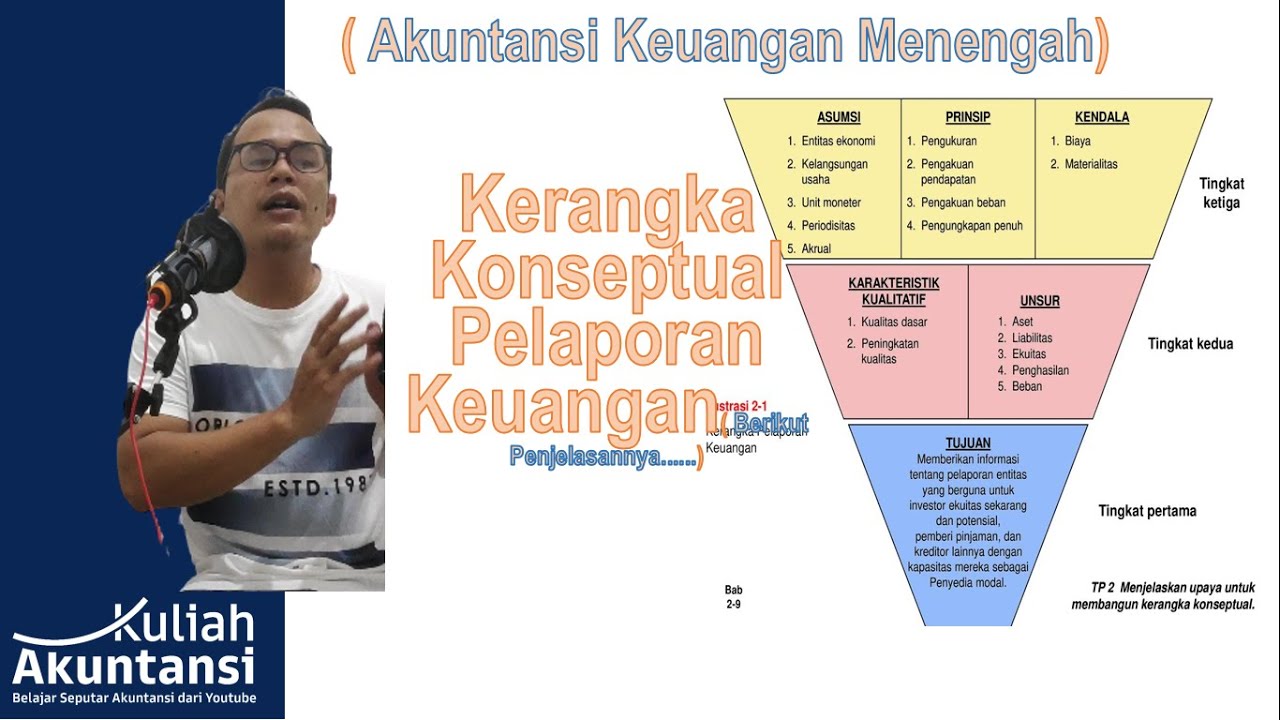

What are the three levels of the conceptual framework in financial reporting?

-The three levels of the conceptual framework are: (1) The basic objectives of financial reporting, (2) The characteristics and elements required for the financial statements, and (3) The assumptions, principles, and limitations involved in financial reporting implementation.

How does the conceptual framework relate to the preparation of financial statements?

-The conceptual framework provides the foundational concepts and guidelines that support the preparation of financial statements. It helps define the objectives of financial reporting, the qualitative characteristics of the information, and the recognition, measurement, and disclosure principles.

What is the primary goal of financial reporting according to the script?

-The primary goal of financial reporting is to provide useful financial information to investors, creditors, and other users that helps in making decisions related to the allocation of resources, particularly for investment and lending purposes.

What are the two main qualitative characteristics of financial information?

-The two main qualitative characteristics of financial information are relevance and faithful representation. Relevance means the information should be useful for decision-making, while faithful representation ensures that the information accurately reflects the economic reality.

What are the components that make up 'relevance' in financial reporting?

-Relevance in financial reporting is made up of three components: (1) Predictive value, where the information helps in forecasting future outcomes, (2) Confirmatory value, where the information verifies or corrects past expectations, and (3) Materiality, which means that the information is significant enough to affect decision-making.

What does 'faithful representation' mean in the context of financial reporting?

-Faithful representation refers to the requirement that financial information should be complete, neutral, and free from error. It ensures that the information presented reflects the true economic events and conditions of the entity.

What are the additional qualitative characteristics that enhance financial information?

-The additional qualitative characteristics are comparability, verifiability, timeliness, and understandability. These qualities improve the usability of financial information by allowing comparisons across entities, confirming its accuracy, ensuring it is available when needed, and ensuring it is easily understood by users.

What are the five elements that form the foundation of financial statements?

-The five elements are: (1) Assets, (2) Liabilities, (3) Equity, (4) Revenues, and (5) Expenses. These elements form the core components of the financial statements, with assets and liabilities making up the balance sheet, and revenues and expenses contributing to the income statement.

What are the basic assumptions used in financial reporting?

-The basic assumptions in financial reporting include: (1) The economic entity assumption, which separates the entity's activities from its owners; (2) The going concern assumption, which assumes the entity will continue operating; (3) The monetary unit assumption, which uses money as the common measure for transactions; (4) The periodicity assumption, which allows for the division of the entity’s activities into time periods; and (5) The accrual basis assumption, which records transactions when they occur, not when cash changes hands.

Outlines

Dieser Bereich ist nur für Premium-Benutzer verfügbar. Bitte führen Sie ein Upgrade durch, um auf diesen Abschnitt zuzugreifen.

Upgrade durchführenMindmap

Dieser Bereich ist nur für Premium-Benutzer verfügbar. Bitte führen Sie ein Upgrade durch, um auf diesen Abschnitt zuzugreifen.

Upgrade durchführenKeywords

Dieser Bereich ist nur für Premium-Benutzer verfügbar. Bitte führen Sie ein Upgrade durch, um auf diesen Abschnitt zuzugreifen.

Upgrade durchführenHighlights

Dieser Bereich ist nur für Premium-Benutzer verfügbar. Bitte führen Sie ein Upgrade durch, um auf diesen Abschnitt zuzugreifen.

Upgrade durchführenTranscripts

Dieser Bereich ist nur für Premium-Benutzer verfügbar. Bitte führen Sie ein Upgrade durch, um auf diesen Abschnitt zuzugreifen.

Upgrade durchführenWeitere ähnliche Videos ansehen

SBR Topic Explainer: Solving questions using the conceptual framework

Conceptual Framework for Financial Reporting 2018 (IFRS Framework) - still applies in 2024

Akuntansi Keuangan Menengah : Kerangka Konseptual Pelaporan Keuangan

Accounting Principles

MENTORING - Akuntansi Keuangan Menengah 1 (Semester 2)

Accounting Intermediate - Kieso : Chapter 1 (Financial Reporting & Accounting Standards)

5.0 / 5 (0 votes)