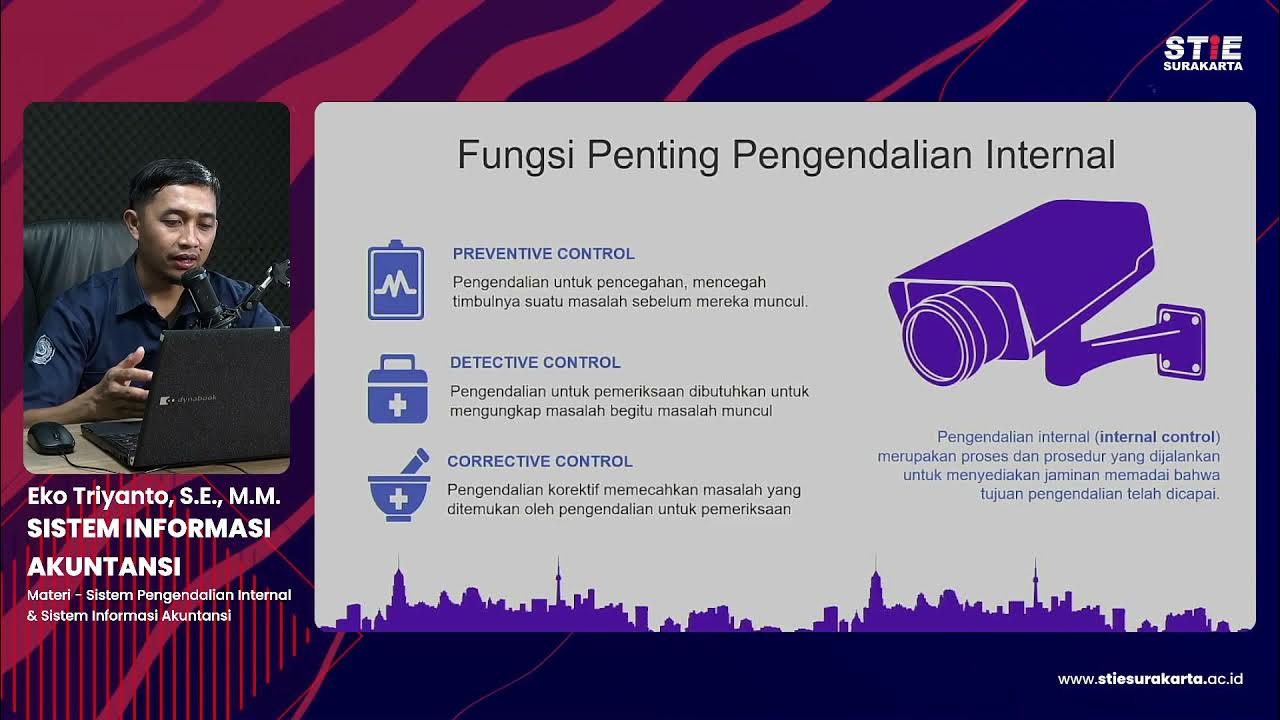

The 5 Components of Internal Control

Summary

TLDRThe video discusses the five key components of internal control as identified by the Committee of Sponsoring Organizations (COSO). These components include the control environment, emphasizing the importance of management's tone; risk assessment, which involves identifying potential financial risks; control activities, which are specific procedures to mitigate these risks; information and communication, highlighting the need for reliable financial data and clear responsibilities; and monitoring activities, focusing on the continuous evaluation of internal controls. Together, these elements create a robust framework to enhance accountability and safeguard financial integrity within organizations.

Takeaways

- 😀 The committee has identified five components of internal control: control environment, risk assessment process, internal controls, information quality, and monitoring effectiveness.

- 😀 The control environment sets the foundation for internal control within an organization, influenced heavily by the attitudes of top management.

- 😀 The 'tone at the top' reflects how seriously top management, like the CEO, views internal controls, impacting the entire organization's attitude toward them.

- 😀 A risk assessment process is crucial for identifying and managing risks, including financial statement fraud, which informs the implementation of internal controls.

- 😀 Internal controls include policies and procedures designed to address identified risks, such as segregation of duties and authorization of transactions.

- 😀 Effective internal controls require a reliable accounting system that produces quality financial information, ensuring data accuracy for decision-making.

- 😀 Communication of internal control responsibilities to employees is vital; formal policy manuals and emails can help convey these responsibilities clearly.

- 😀 Monitoring activities involve continuously evaluating the effectiveness of internal controls to ensure they are functioning as intended.

- 😀 Organizations must actively assess whether internal controls are catching mistakes or misstatements and take corrective actions when necessary.

- 😀 The overall effectiveness of internal controls is dependent on both their implementation and the continuous evaluation of their performance.

Q & A

What are the five components of internal control identified by the committee of sponsoring organizations?

-The five components are the control environment, risk assessment process, internal controls, quality of information, and monitoring activities.

What does the 'control environment' refer to in the context of internal control?

-The control environment refers to the standards, processes, and structures that form the foundation for internal control within an organization, including the tone set by top management.

How does the CEO's attitude towards internal control influence the organization?

-If the CEO views internal control as unimportant or merely a formality, it's unlikely that lower-level employees will take it seriously, thereby affecting the overall control environment.

Why is risk assessment important in the context of internal control?

-Risk assessment is crucial for identifying and managing risks that may affect the business, including financial statement fraud, and it informs the design of internal controls.

What are examples of internal controls that organizations might implement?

-Examples include segregation of duties, authorization of transactions, and reconciliation of cash accounts to ensure accuracy and prevent fraud.

How does the quality of information impact internal control?

-If the accounting system produces unreliable financial information, it complicates the assessment of transactions and internal control effectiveness, making it difficult to ensure accurate financial reporting.

What role does communication play in effective internal control?

-Effective communication ensures that employees understand their responsibilities regarding internal controls, which can be facilitated through emails or formal policy manuals.

What are monitoring activities in the context of internal control?

-Monitoring activities involve continuously evaluating the effectiveness of internal controls to ensure they are being applied correctly and are functioning as intended.

What should organizations do if they find their internal controls to be ineffective?

-Organizations should take action to address and rectify any issues identified with their internal controls to enhance effectiveness and ensure accurate financial reporting.

Why is it not enough for organizations to assume their internal controls are working?

-Organizations must actively evaluate their internal controls rather than just assuming they are effective, as this ensures ongoing reliability and helps catch any mistakes or misstatements.

Outlines

Dieser Bereich ist nur für Premium-Benutzer verfügbar. Bitte führen Sie ein Upgrade durch, um auf diesen Abschnitt zuzugreifen.

Upgrade durchführenMindmap

Dieser Bereich ist nur für Premium-Benutzer verfügbar. Bitte führen Sie ein Upgrade durch, um auf diesen Abschnitt zuzugreifen.

Upgrade durchführenKeywords

Dieser Bereich ist nur für Premium-Benutzer verfügbar. Bitte führen Sie ein Upgrade durch, um auf diesen Abschnitt zuzugreifen.

Upgrade durchführenHighlights

Dieser Bereich ist nur für Premium-Benutzer verfügbar. Bitte führen Sie ein Upgrade durch, um auf diesen Abschnitt zuzugreifen.

Upgrade durchführenTranscripts

Dieser Bereich ist nur für Premium-Benutzer verfügbar. Bitte führen Sie ein Upgrade durch, um auf diesen Abschnitt zuzugreifen.

Upgrade durchführenWeitere ähnliche Videos ansehen

Internal Controls Framework

Internal Control Basics | Principles of Accounting

Control Frameworks: COSO & COBIT | Fundamentals of Internal Auditing | Part 5 of 44

Sistem Informasi Akuntansi #8 Sistem pengendalian internal & Sistem Informasi Akuntansi-Eko Triyanto

All about the COSO framework

Komponen pengendalian internal COSO

5.0 / 5 (0 votes)