How A Mathematician Made WALL ST Look Stupid

Summary

TLDRJim Simons, a math genius and former NSA codebreaker, revolutionized hedge fund trading with his Medallion Fund, achieving extraordinary returns. By using advanced mathematical models and machine learning, he discovered patterns in the stock market that others couldn't see. With his firm Renaissance Technologies, Simons built an algorithmic trading system that thrived through market crashes and made billionaires of its employees. Simons' approach was rooted in data, not intuition, and his success proves that small, consistent edges can compound into immense wealth.

Takeaways

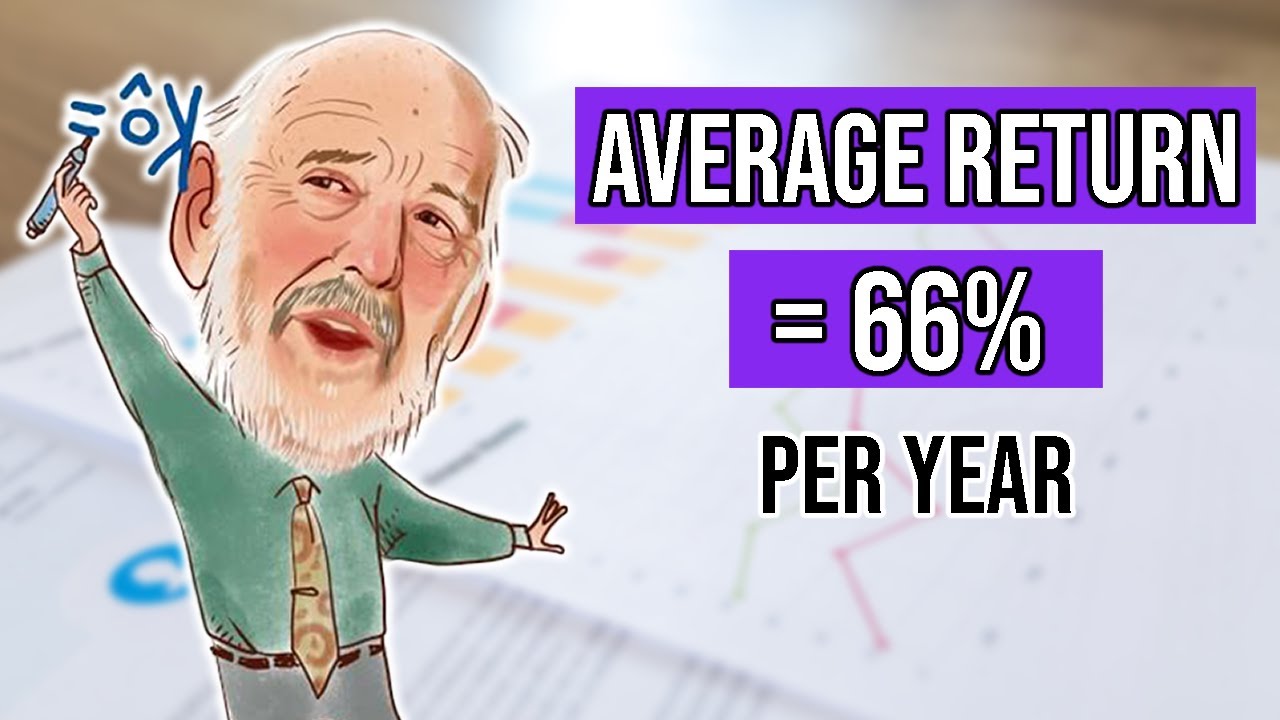

- 😀 Jim Simons, a math professor, was the best trader in the world, managing the Medallion Fund to an average annual return of 66% from 1988 to 2018, crushing the market over three decades.

- 😀 Despite having no finance background, Simons built the most successful hedge fund by applying advanced math and algorithms, treating the stock market as a mathematical problem to solve.

- 😀 If you invested $1,000 in Medallion Fund in 1988, it would have been worth $139 billion before fees, though after fees, it would have only been $195 million.

- 😀 Simons' approach was revolutionary. He believed that market price movements were not random but could be predicted using mathematical patterns, challenging traditional market theories.

- 😀 Unlike other hedge fund managers, Simons didn’t rely on earnings reports or geopolitical events; instead, he analyzed massive amounts of data and built algorithms to predict price movements.

- 😀 The core idea was that everything in the world is connected, and by analyzing vast amounts of data—from weather patterns to geopolitical events—Simons and his team could foresee market changes.

- 😀 Simons hired top mathematicians, statisticians, and computer scientists as partners to align everyone's interests, and they all worked together to crack the market's code.

- 😀 The Medallion Fund struggled initially, with poor returns in its first years, but after changes to the algorithm and strategy, it started delivering extraordinary returns, like 58% when the S&P lost 6.5% in 1991.

- 😀 In 1993, Simons brought in machine learning experts Robert Mercer and Peter Brown to further refine the algorithm, leading to breakthroughs that enabled the system to predict market movements by analyzing patterns in data.

- 😀 By the time Simons passed away in 2024, his wealth had reached $31.4 billion, making him the 55th richest person in the world and solidifying his position as the greatest hedge fund manager ever.

Q & A

Who was Jim Simons and what made him so successful?

-Jim Simons was a mathematician who became the most successful hedge fund manager of all time, running the Medallion Fund at Renaissance Technologies. He had no formal background in finance but applied mathematical models, algorithms, and machine learning to the stock market, achieving an extraordinary average annual return of 66% before fees over 30 years.

How did Jim Simons manage to outperform legendary investors like Warren Buffett?

-Jim Simons outperformed Warren Buffett by treating the stock market as a mathematical problem. Unlike Buffett, who focused on fundamental analysis of companies, Simons used data, statistics, and algorithms to identify patterns and predict market movements, which allowed him to generate high returns consistently.

What role did mathematics play in Simons' trading strategy?

-Mathematics was central to Simons' strategy. He used mathematical models to analyze vast amounts of data and identify patterns in the market. His approach was based on the idea that market movements weren’t random, and that complex relationships between various factors (like weather, crop yields, and currencies) could predict price changes.

Why did Simons treat the stock market as a math problem instead of focusing on traditional financial analysis?

-Simons believed that the stock market wasn’t just about company earnings or geopolitical events, as many traditional traders thought. He saw it as a complex system of interconnected variables that could be predicted using mathematical models, unlike the conventional buy-and-hold strategy that assumed randomness in market movements.

How did Simons’ background in mathematics influence his approach to trading?

-Simons' background in mathematics gave him the skills to develop algorithms capable of detecting hidden patterns in market data. His experience working as a codebreaker for the NSA also honed his ability to find patterns in seemingly random data, which he applied to financial markets.

What is the Medallion Fund, and how did it perform over the years?

-The Medallion Fund was a hedge fund run by Renaissance Technologies, which achieved average annual returns of 66% from 1988 to 2018 before fees. Despite a strong track record, after fees, it would still have delivered impressive returns, such as turning a $1,000 investment in 1988 into $195 million by 2024.

What was the 'aha' moment that led Jim Simons to pursue a career in trading?

-Simons had his 'aha' moment when he realized that market movements weren’t entirely random. By studying data, he noticed patterns emerging from the connections between real-world events, like weather patterns affecting commodities, which could influence stock prices.

Why did Simons focus on small, frequent trades instead of large, speculative ones?

-Simons' strategy involved making tiny profits on millions of small trades rather than large, speculative bets. This approach minimized risk and allowed the algorithm to exploit inefficiencies in the market repeatedly, without moving the market itself with large trades.

How did the introduction of machine learning improve the Medallion Fund's performance?

-The introduction of machine learning in the 1990s allowed the Medallion Fund’s algorithms to evolve continuously. By analyzing past patterns, the system could teach itself new strategies, making predictions more accurate and improving trading performance even further.

What was the role of Robert Mercer and Peter Brown in the development of Renaissance Technologies?

-Robert Mercer and Peter Brown were key figures in bringing machine learning to Renaissance Technologies. They applied their expertise in predicting human speech to the stock market, creating algorithms that could learn and improve their predictions based on historical data, which dramatically boosted the fund's performance.

Outlines

هذا القسم متوفر فقط للمشتركين. يرجى الترقية للوصول إلى هذه الميزة.

قم بالترقية الآنMindmap

هذا القسم متوفر فقط للمشتركين. يرجى الترقية للوصول إلى هذه الميزة.

قم بالترقية الآنKeywords

هذا القسم متوفر فقط للمشتركين. يرجى الترقية للوصول إلى هذه الميزة.

قم بالترقية الآنHighlights

هذا القسم متوفر فقط للمشتركين. يرجى الترقية للوصول إلى هذه الميزة.

قم بالترقية الآنTranscripts

هذا القسم متوفر فقط للمشتركين. يرجى الترقية للوصول إلى هذه الميزة.

قم بالترقية الآنتصفح المزيد من مقاطع الفيديو ذات الصلة

The BEST Trader In History - Legend Jim Simons - Strategy/Style/Story

The $25B Day Trader that Even Warren Buffett Acknowledges

The INSANE Story of the GREATEST TRADER of ALL TIME | Jim Simons

Jim Simons: How To Achieve a 66% Return Per Year (7 Strategies)

How a Mathematician Became the Greatest Trader of All Time

Wall Street’s Biggest Secret (The Medallion Fund)

5.0 / 5 (0 votes)