The $25B Day Trader that Even Warren Buffett Acknowledges

Summary

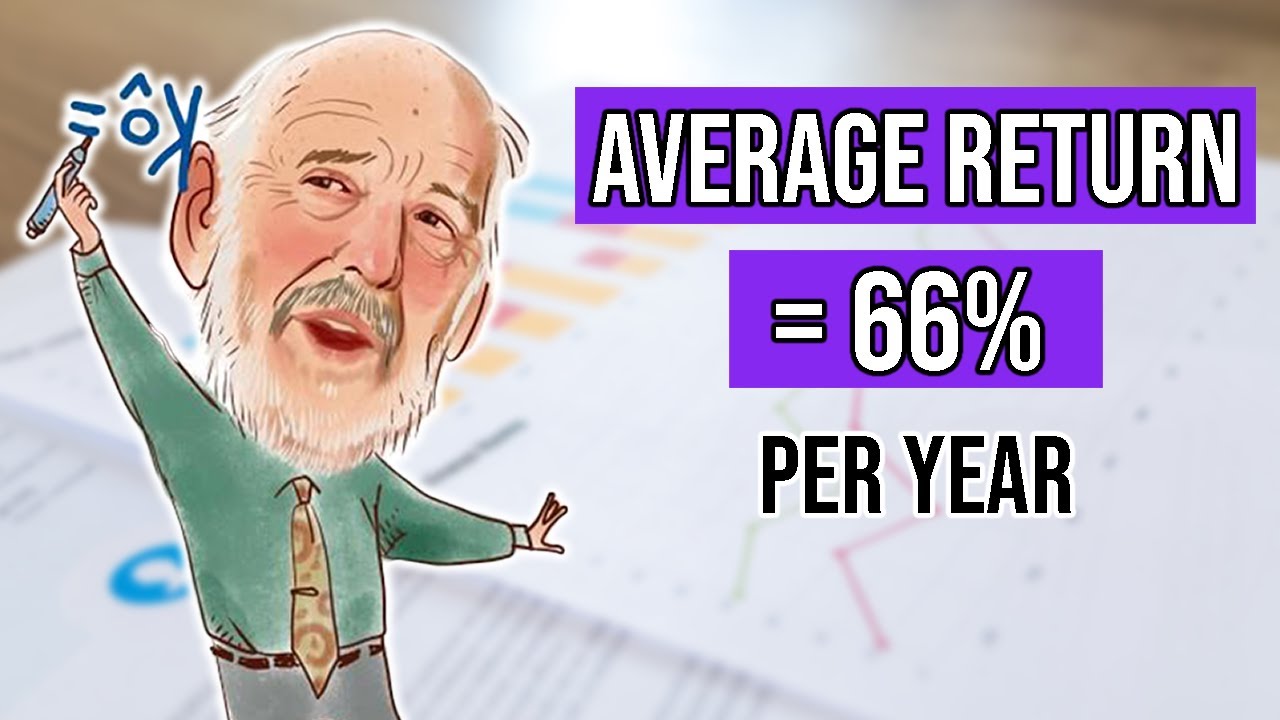

TLDRJim Simons utilized advanced mathematics and machine learning to achieve exceptional returns from short-term stock market predictions with his Medallion hedge fund. By gathering massive amounts of data and hiring brilliant mathematicians to uncover obscure patterns, Simons developed algorithms exploiting human biases. The fund averages nearly 40% annual returns, proving quant trading works yet is infeasible for regular investors. Simons suggests long-term value investing remains a sound approach.

Takeaways

- 😲 Jim Simons turned $0 into $25 billion through Renaissance Technologies and the Medallion hedge fund, which utilizes advanced mathematics and machine learning to make short-term stock market predictions

- 📈 The Medallion fund averages annual returns of 66% before fees by identifying patterns in massive amounts of market data that most investors miss

- 🤯 Medallion executes up to 300,000 trades per day, holding positions for only minutes or seconds, to capitalize on short-term inefficiencies

- 💡 The fund's edge comes from mathematics, data analysis and predictive modeling - areas where humans struggle to compete

- 📊 Simons and his team focus strictly on probabilities, not business fundamentals or qualitative analysis

- 🤠 Simons himself was critical for hiring creative thinkers from non-traditional backgrounds, not just Wall Street experts

- 👪 The Medallion fund has been closed to outside investors since 1993 - only Renaissance employees and family can invest

- 🤑 Medallion's profits likely come from other speculators and traders, not long-term investors or index funds

- ❌ Regular investors should not try to mimic Medallion's strategies from home

- 📚 Value investing still works for small investors - the machines have not yet caught up here

Q & A

What was the main secret behind the success of Renaissance Technologies' Medallion fund?

-The main secret was using tons of data and advanced mathematics to develop automated trading algorithms and machine learning models to predict short-term market movements.

What is statistical arbitrage and how did Medallion use it?

-Statistical arbitrage involves identifying market-wide factors that explain stock movements and betting on stocks that have moved the least in the direction predicted by the factors, while betting against those that have moved more than predicted. This is a form of mean reversion.

Who were some of the key mathematicians that contributed to Medallion's success?

-Some key mathematicians were Lenny Baum, James Ax, René Carmona, Elwyn Berlekamp, Robert Mercer and Peter Brown. Each specialized in different areas like Markov models, algebra, stochastic calculus, game theory and computer science.

What does the Kelly criterion determine?

-The Kelly criterion determines the optimal size of a trading position in order to maximize long-term growth of capital based on the win rate and payoff ratio.

Why hasn't Renaissance's long-term stock fund RIEF been as successful as Medallion?

-Medallion's forecasting methods work very well for short-term predictions like weather forecasts, but degrade over longer time periods. RIEF hasn't matched Medallion's performance since it aims for longer-term stock market forecasts.

Who are likely the counterparties providing profits for Medallion?

-It is likely short-term traders, both large and small, who provide profits for Medallion. These are speculators making emotional decisions without advanced algorithms.

What was Jim Simons' first hedge fund called and why?

-His first hedge fund launched in 1978 was called Monemetrics, combining the words money and econometrics, hinting that he would use math to analyze markets.

How has Medallion's trading volume and frequency changed over time?

-In 2000, Medallion executed 150,000-300,000 trades per day. Today with advances in technology, the volume is likely even higher, with average hold times as low as seconds or minutes.

What is Renaissance's motto that hints at their philosophy?

-Their motto is: "Bad ideas is good. Good ideas is terrific. No ideas is terrible." This shows their focus on creativity and idea generation.

What was the conclusion for individual investors regarding trading vs investing?

-The conclusion was that individuals should still opt for long-term value investing over short-term trading or technical analysis, since that is an area machines have yet to dominate.

Outlines

This section is available to paid users only. Please upgrade to access this part.

Upgrade NowMindmap

This section is available to paid users only. Please upgrade to access this part.

Upgrade NowKeywords

This section is available to paid users only. Please upgrade to access this part.

Upgrade NowHighlights

This section is available to paid users only. Please upgrade to access this part.

Upgrade NowTranscripts

This section is available to paid users only. Please upgrade to access this part.

Upgrade NowBrowse More Related Video

How A Mathematician Made WALL ST Look Stupid

The BEST Trader In History - Legend Jim Simons - Strategy/Style/Story

Jim Simons: How To Achieve a 66% Return Per Year (7 Strategies)

Wall Street’s Biggest Secret (The Medallion Fund)

Jim Simons Trading Secrets 1.1 MARKOV Process

The INSANE Story of the GREATEST TRADER of ALL TIME | Jim Simons

5.0 / 5 (0 votes)