Kuliah Akuntansi Manajemen: Konsep dan Perilaku Biaya

Summary

TLDRThis video discusses key concepts in cost behavior and management accounting. It explains the definition of cost, opportunity cost, and the distinction between direct and indirect costs. The transcript highlights how costs can be traced to specific objects, illustrating examples from healthcare and manufacturing. It further elaborates on the unique characteristics of service products versus tangible goods, emphasizing the challenges in measuring and managing service quality. Additionally, the video explores the implications of cost definitions based on managerial objectives, demonstrating the importance of aligning costs with strategic decision-making.

Takeaways

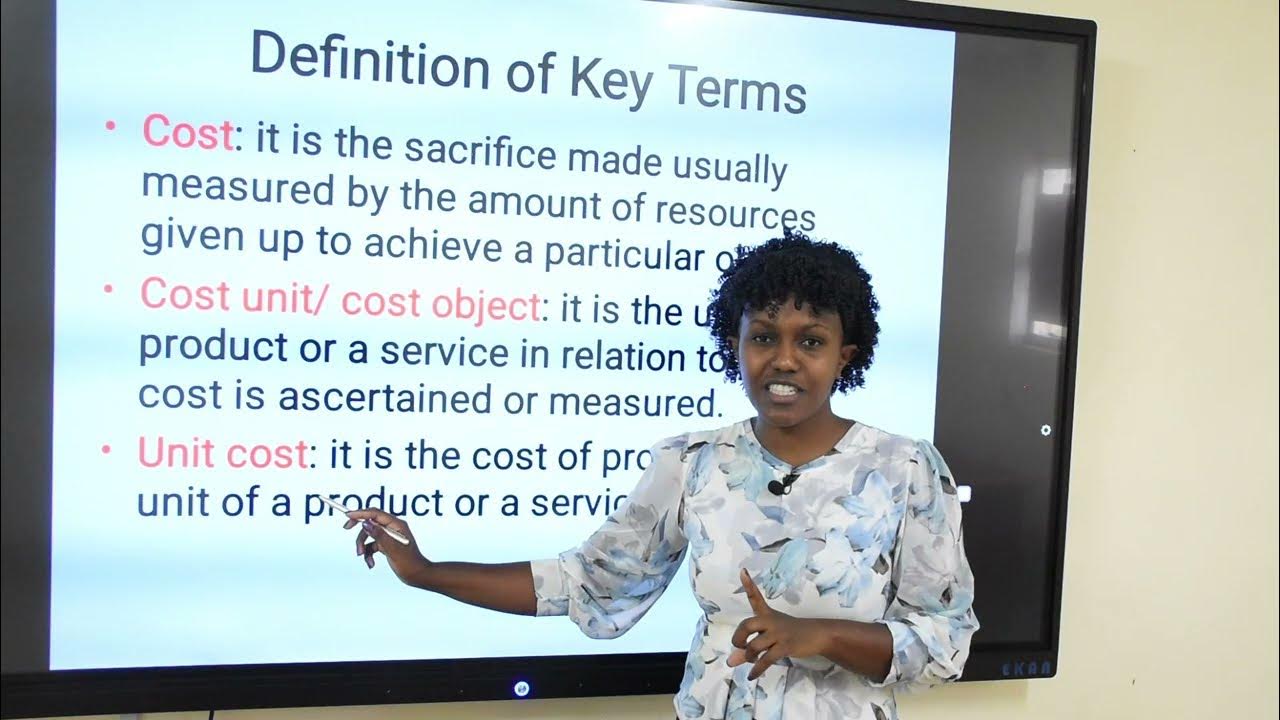

- 😀 Costs represent cash equivalents sacrificed to obtain goods or services, expected to provide future benefits to an organization.

- 😀 Opportunity cost is the benefit lost when one alternative is chosen over another, illustrating the trade-offs in investment decisions.

- 😀 Cost objects can include products, projects, customers, and activities used to measure and allocate costs accurately.

- 😀 Direct costs are easily traceable to a specific cost object, while indirect costs cannot be directly traced with accuracy.

- 😀 Traceability is crucial for accurate cost allocation, with greater traceability leading to more precise cost assignments.

- 😀 Different types of cost tracing methods include direct tracing, which links costs directly to cost objects, and driver tracing, which uses observable factors to allocate costs.

- 😀 Costs can be allocated based on resource consumption, such as tracking machine hours for multiple products to determine shared expenses.

- 😀 Tangible products are created through the transformation of raw materials using direct labor, while intangible products (services) involve customer participation in the production process.

- 😀 The nature of services being intangible means they cannot be stored or patented, leading to unique challenges in management accounting.

- 😀 The cost of goods sold varies depending on managerial objectives, influencing pricing strategies, product mix decisions, and profitability analysis.

Q & A

What is the definition of cost as mentioned in the transcript?

-Cost is defined as a cash equivalent sacrificed or incurred to obtain goods or services expected to benefit an organization now or in the future.

What is opportunity cost?

-Opportunity cost is the benefit that is foregone when one alternative is chosen over another, representing the potential return from the next best alternative.

How is opportunity cost calculated in the example provided?

-In the example, if a company invests 100,000 in inventory instead of stocks with a 12% return, the opportunity cost is 12% of 100,000, which amounts to 12,000.

What distinguishes direct costs from indirect costs?

-Direct costs can be easily and accurately traced to a cost object, while indirect costs cannot be easily traced and must be allocated using appropriate methods.

What is the significance of traceability in cost allocation?

-Traceability refers to the ability to assign costs to cost objects economically and accurately, with a strong causal relationship between costs and their respective objects.

Can you give an example of a direct cost and an indirect cost in a hospital?

-An example of a direct cost in a hospital is the heating and cooling of patient rooms, while an indirect cost would be the salaries of management staff.

What are the two methods of tracing costs mentioned in the transcript?

-The two methods of tracing costs are direct tracing, which involves physical identification of costs related to a cost object, and driver tracing, which uses observable factors to measure resource consumption.

How are costs allocated between different products in a shared production environment?

-Costs can be allocated based on the number of machine hours used for each product, allowing for a fair distribution of shared costs like utilities.

What are tangible and intangible products, and how are they related to management accounting?

-Tangible products are physical goods produced, while intangible products refer to services. Management accounting must consider the unique characteristics of services, such as their inability to be stored.

What factors complicate the accounting for services compared to tangible products?

-Services are intangible, cannot be patented, are perishable, and vary greatly between customers, making standardization and consistent quality challenging.

Outlines

هذا القسم متوفر فقط للمشتركين. يرجى الترقية للوصول إلى هذه الميزة.

قم بالترقية الآنMindmap

هذا القسم متوفر فقط للمشتركين. يرجى الترقية للوصول إلى هذه الميزة.

قم بالترقية الآنKeywords

هذا القسم متوفر فقط للمشتركين. يرجى الترقية للوصول إلى هذه الميزة.

قم بالترقية الآنHighlights

هذا القسم متوفر فقط للمشتركين. يرجى الترقية للوصول إلى هذه الميزة.

قم بالترقية الآنTranscripts

هذا القسم متوفر فقط للمشتركين. يرجى الترقية للوصول إلى هذه الميزة.

قم بالترقية الآنتصفح المزيد من مقاطع الفيديو ذات الصلة

[MEET 2] AKUNTANSI MANAJEMEN - KONSEP & PERILAKU BIAYA

Introduction to Cost and Management Accounting

2023 Meet 3 Akuntasi Manajemen : Konsep dan Prilaku Biaya

[Strategic Cost Management] General Subject Orientation

Akuntansi Biaya Bab 1: Manajemen, Controller, dan Akuntansi Biaya

2023 Meet 2 Akuntansi Manajemen : Konsep Dasar Akuntansi Manajemen

5.0 / 5 (0 votes)