Queuing theory and Poisson process

Summary

TLDRThis script explores queuing theory, focusing on the Poisson process to model customer arrivals in a queue. It simplifies the system by assuming independent arrivals and service completions, leading to the M/M/1 queue model. The script delves into the derivation of probability equations for queue states and their long-term behavior, highlighting the importance of the ratio of arrival to service rates. It concludes with the invariant distribution for stable queues and introduces more complex queuing models, providing a foundational understanding of real-life queue modeling.

Takeaways

- 📊 In real life, queues can be modeled by focusing on customer arrivals and service processes.

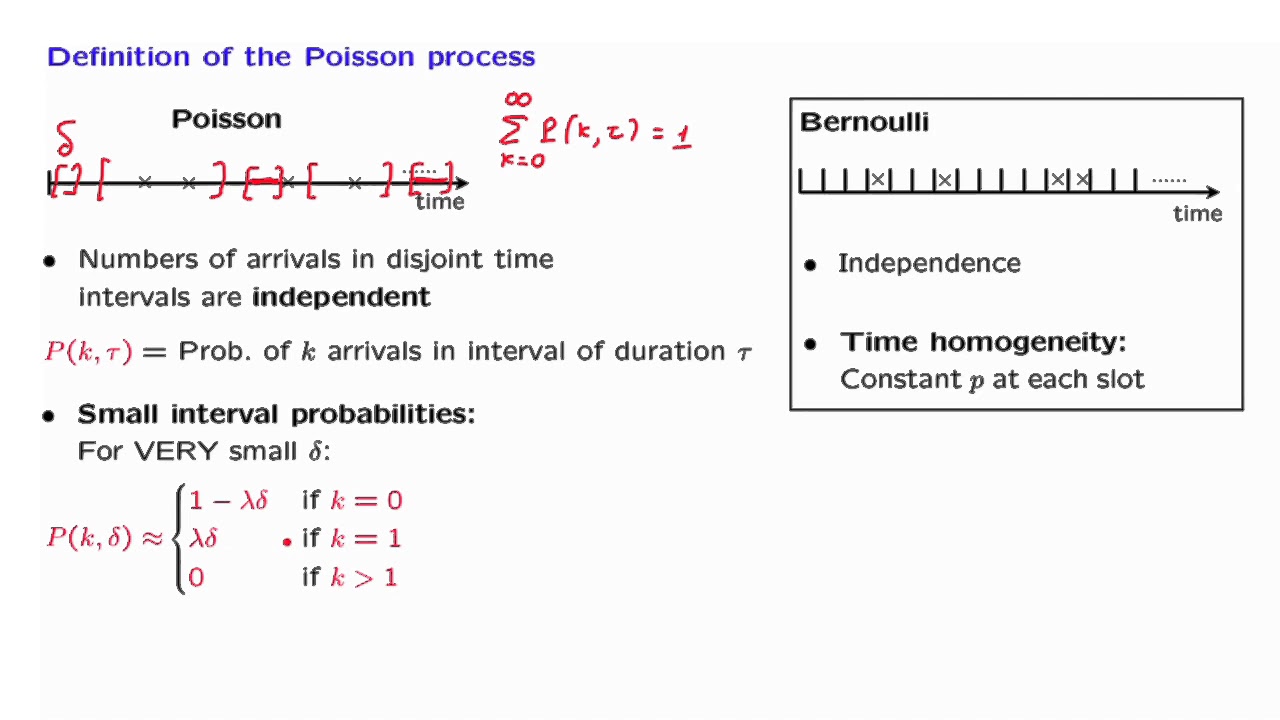

- 📅 Customer arrivals are assumed to be independent, arriving at random intervals.

- 🔢 The Poisson process is used to model customer arrivals, with the average rate of arrivals denoted as lambda.

- 🧮 The probability of having k customers arriving in a unit time follows a Poisson distribution.

- 🔄 The service process in a queue can also be modeled with a rate of service denoted as mu, which might differ from the arrival rate.

- 📈 The state of the queue is represented by the number of customers present, evolving over time based on arrival and departure rates.

- 🧩 Differential equations describe the evolution of queue states over time, though exact solutions can be complex.

- 📉 The long-term behavior of the queue can stabilize, leading to a constant distribution of state probabilities, known as the invariant distribution.

- 💡 The simplest queuing model, M/M/1, assumes memoryless arrival and service processes, but more complex models like M/M/c or M/G/k exist.

- 🌐 Networks of queues, such as Jackson networks, involve interactions between multiple queues, adding complexity to the model.

Q & A

What is the fundamental assumption made when modeling customer arrivals in a queue?

-The fundamental assumption is that the arrival times are independent from each other, meaning a customer arriving at a specific time has no knowledge about the other customers or their arrival times, essentially showing up at random.

How is the average number of customers arriving in a unit of time calculated?

-The average number of customers arriving in a unit of time is calculated by multiplying the probability of a customer arriving in a subinterval (lambda / n) by the number of subintervals (n), which simplifies to lambda.

What is the Poisson distribution and how is it related to the queuing model?

-The Poisson distribution is a probability distribution that expresses the probability of a given number of events occurring in a fixed interval of time. It is used in the queuing model to represent the distribution of the number of customers arriving during a unit time interval.

What is the M/M/1 queue model and what does each 'M' stand for?

-The M/M/1 queue model is a type of queuing model where 'M' stands for memoryless, indicating that both the arrival process and service times are memoryless (exhibiting the property of independence between inter-arrival and service times). The '1' indicates there is only one service counter.

What is the significance of the ratio lambda/mu in the M/M/1 queue model?

-The ratio lambda/mu is significant as it determines the stability of the queue. If lambda is less than mu, the queue is stable and probabilities tend to an invariant distribution. If lambda is greater than mu, the queue is unstable and tends to grow indefinitely.

What does the term 'memoryless' imply in the context of queuing theory?

-In queuing theory, 'memoryless' refers to the property where the probability of an event occurring in the next time interval is independent of the time since the last event occurred. This is a characteristic of both the arrival process and service times in the M/M/1 model.

How are the long-term probabilities of the queue being in different states calculated?

-The long-term probabilities are calculated by solving a set of recurrence relations derived from the differential equations governing the evolution of the probabilities. The sum of these probabilities must equal 1, which helps in finding the initial probability pi_0.

What is a Jackson network in the context of queuing theory?

-A Jackson network is a queuing network model where multiple individual queues (often M/M/1 queues) interact with each other. After service, a customer can either leave the system entirely or join the back of another queue in the network.

What are the modified Bessel functions of the first kind and why are they important in the M/M/1 queue model?

-The modified Bessel functions of the first kind are special functions that often appear in solutions to differential equations. In the M/M/1 queue model, they appear in the exact solution for the probabilities of the queue being in different states, making them important in the mathematical analysis of the queue.

What is the qualitative behavior of the M/M/1 queue model when lambda is greater than mu?

-When lambda is greater than mu, the queue model exhibits a qualitative behavior where the queue tends to grow over time. The probabilities shift towards more customers in the queue, and the system does not stabilize at a set of invariant probabilities.

Outlines

此内容仅限付费用户访问。 请升级后访问。

立即升级Mindmap

此内容仅限付费用户访问。 请升级后访问。

立即升级Keywords

此内容仅限付费用户访问。 请升级后访问。

立即升级Highlights

此内容仅限付费用户访问。 请升级后访问。

立即升级Transcripts

此内容仅限付费用户访问。 请升级后访问。

立即升级

5.0 / 5 (0 votes)