Internal Controls Explained

Summary

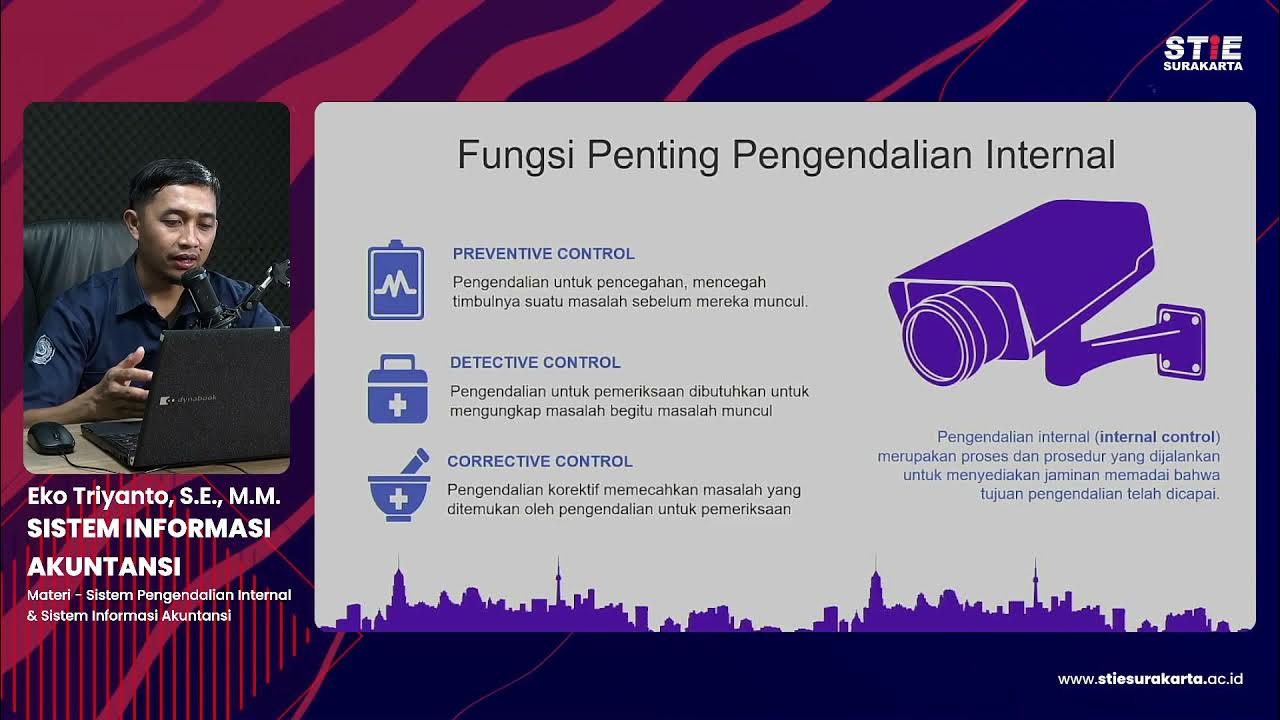

TLDRThis video script delves into the critical role of internal controls in ensuring business efficiency, reliable reporting, and compliance with laws. It outlines the five key components: control environment, risk assessment, monitoring, information and communication, and control activities. The script emphasizes the importance of a proper control environment as the foundation, continuous risk assessments to manage threats, and the necessity of open information flow. It also discusses control activities like establishing responsibility, segregation of duties, physical securities, and independent verification to minimize errors and maintain reliable records.

Takeaways

- 🏢 **Internal Controls Importance**: Every company needs internal controls to ensure operations are efficient, reporting is reliable, and laws and regulations are followed.

- 🌐 **Control Environment**: It's the foundation of internal control and sets the tone for how employees work within the company.

- 🔍 **Risk Assessment**: Companies implement risk assessments to identify and manage threats both internally and externally.

- 🔁 **Continuous Monitoring**: Monitoring is ongoing, ensuring the quality of business operations through supervisory checks or separate evaluations.

- 📢 **Information and Communication**: Open flow of relevant information is necessary for employees and employers to fulfill their responsibilities effectively.

- 🚫 **Risk Management**: After risks are identified, control activities are established to manage them, including estimating impact and likelihood.

- 👥 **Establishing Responsibility**: Knowing who is accountable for what task is critical for good internal control.

- 🔄 **Segregation of Duties**: It limits one person's control over certain tasks, reducing the risk of errors by cross-checking employees' work.

- 🔒 **Physical Securities**: Measures like computer passwords and surveillance cameras protect the business from physical threats.

- 📑 **Adequate Documentation**: Maintaining error-free records through documentation practices is essential for reliable accounting.

- 🔎 **Independent Verification**: Third-party verifications ensure an objective account of the company's performance.

Q & A

What are internal controls and why are they important for a business?

-Internal controls are the policies and procedures that a company uses to ensure that its operations are efficient and effective, its reporting is reliable, and it complies with laws and regulations. They are important because they help to reduce risks, ensure the accuracy of financial reporting, and promote accountability within the organization.

What are the five components of internal controls mentioned in the script?

-The five components of internal controls mentioned are the control environment, risk assessment, monitoring, information and communication, and control activities.

How is the control environment described in the script?

-The control environment is described as the foundation of internal control and is likened to the atmosphere of a business where members work. It is emphasized that without a proper control environment, all other internal controls suffer.

What role does monitoring play in internal controls?

-Monitoring in internal controls involves the assessment of a business's quality and can be done through ongoing activities like supervisors checking or through separate evaluations. It helps to ensure that the internal controls are functioning effectively.

Why is information and communication important in internal controls?

-Information and communication are important because they ensure an open flow of information relevant to the company. This allows employers and employees to communicate effectively within a time frame that enables them to carry out their responsibilities.

What are the steps involved in assessing risks within a business?

-Assessing risks in a business involves three steps: estimating the impact of the risk, determining the likelihood of it occurring, and identifying actions to minimize its impact.

How do control activities help manage identified risks?

-Control activities help manage identified risks by establishing responsibility, segregating duties, implementing physical securities, maintaining adequate documentation, and performing independent verification.

What does it mean to establish responsibility in internal controls?

-Establishing responsibility means defining who is accountable for what tasks within the organization. This is critical for good internal control as it ensures that management knows who to contact if things go wrong and employees are clear on their responsibilities.

What is the purpose of segregation of duties in internal controls?

-The purpose of segregation of duties is to limit one person's control over certain tasks within a business. By distributing responsibilities among multiple employees, it allows for checks and balances, reducing the risk of errors and fraud.

Why is independent verification important in internal controls?

-Independent verification is important because it involves third-party individuals spontaneously conducting verifications on a business. This helps ensure an objective account of the company's performance and adds an extra layer of assurance to the internal control system.

What are the limitations of internal controls as mentioned in the script?

-The script mentions that internal controls have limitations because they are designed and operated by humans who can make mistakes. This acknowledges that despite the best efforts, there can still be errors in the internal control system.

Outlines

此内容仅限付费用户访问。 请升级后访问。

立即升级Mindmap

此内容仅限付费用户访问。 请升级后访问。

立即升级Keywords

此内容仅限付费用户访问。 请升级后访问。

立即升级Highlights

此内容仅限付费用户访问。 请升级后访问。

立即升级Transcripts

此内容仅限付费用户访问。 请升级后访问。

立即升级浏览更多相关视频

Auditing: Internal Controls and Risk Assessment

Sistem Informasi Akuntansi #8 Sistem pengendalian internal & Sistem Informasi Akuntansi-Eko Triyanto

Internal Controls Implementation

Internal Control Basics | Principles of Accounting

Sistem Informasi Akuntansi_Romney_Pengendalian&Sistem Informasi Akuntansi.

Video en Español: “Auditoría Interna: Una Carrera para Hoy, Una Carrera para Mañana”

5.0 / 5 (0 votes)