AKM1 M02 KB1 Part 3 Komponen Laporan Laba Rugi

Summary

TLDRThis video explains the key components of an income statement, breaking down the 15 essential line items in a clear, step-by-step journey. It starts with total sales and adjusts for costs like the cost of goods sold, operational expenses, and other non-operational income and expenses. Key concepts such as gross profit, operating profit, extraordinary items, and net income are covered, along with unique accounting practices like equity method and deferred tax. The video also highlights the impact of accounting method changes and the significance of earnings per share, making it a crucial guide for understanding company financials.

Takeaways

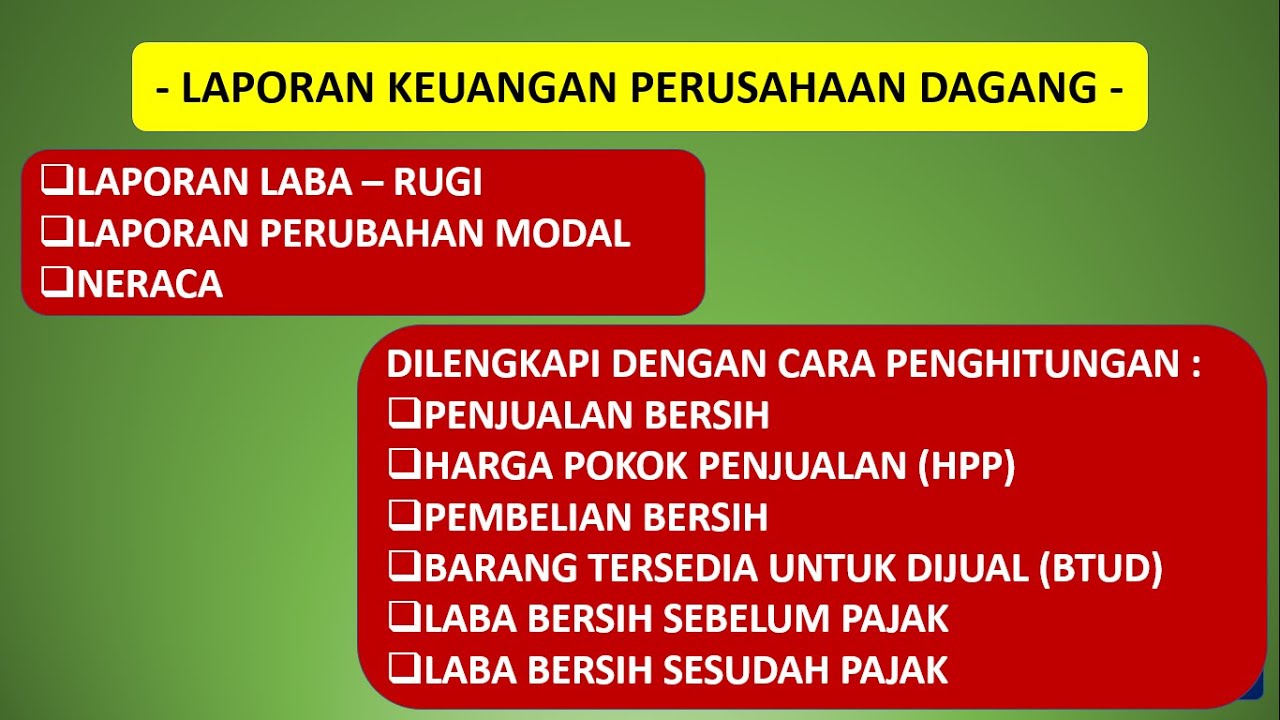

- 😀 The income statement consists of 15 essential items, divided into two main sections: operating income and extraordinary items.

- 😀 The first item, 'Revenue', refers to net sales after accounting for taxes, returns, discounts, and shipping costs.

- 😀 The second item, 'Cost of Goods Sold (COGS)', reflects the cost of goods or services provided, with different calculations for trading and manufacturing companies.

- 😀 Gross profit is the result of subtracting the COGS from total revenue, but it is not yet 'clean' as it doesn't include operating expenses.

- 😀 Operating expenses, or 'Beban Usaha', are split into two categories: selling expenses (marketing) and general & administrative expenses (company management).

- 😀 Operating profit, calculated after deducting operating expenses, shows how efficiently the business runs its core operations.

- 😀 Non-operating income and expenses are recorded separately, including gains or losses from investments, interest, or currency fluctuations.

- 😀 Equity method is used when a company holds 20-50% of another company’s shares. The investor records a share of the affiliate's profit or loss.

- 😀 Extraordinary items are rare and abnormal events that are reported separately to avoid misleading impressions about operational performance.

- 😀 Income tax is calculated based on taxable income, which may differ from accounting profits. Deferred taxes reflect timing differences in the recognition of revenue or expense items.

Q & A

What are the mandatory components in an income statement?

-An income statement must include 15 components, which provide a complete financial journey of a company from its gross sales to net income, including both operational and non-operational costs.

How is 'net sales' calculated in an income statement?

-Net sales are calculated by subtracting sales taxes (such as VAT or PPN), sales returns, discounts, and sales allowances from the gross sales figure. It's the amount the company actually retains from the sale.

What is the significance of the 'cost of goods sold' (COGS) in the income statement?

-COGS is crucial because it represents the direct costs of producing or purchasing the goods that were sold during the period. For retail businesses, it includes the cost of purchasing goods, while for manufacturers, it includes the cost of production.

What is the difference between 'operating expenses' and 'non-operating expenses'?

-Operating expenses include all costs associated with running the business, such as marketing and administrative costs, while non-operating expenses include items like interest or gains from non-core activities like the sale of assets.

What does 'gross profit' signify in an income statement?

-Gross profit is the difference between net sales and the cost of goods sold. It measures the profitability of the company’s core business activities before accounting for other operational expenses.

How are extraordinary items treated in the income statement?

-Extraordinary items are rare and unusual events, such as natural disasters or unexpected legal settlements. They are reported separately in the income statement to avoid misleading readers about the company’s regular operational performance.

What is the role of 'equity method' in accounting for affiliate companies?

-The equity method applies when a company owns between 20% and 50% of another company. The investor company must report its share of the affiliate's profits or losses in its income statement, reflecting its significant influence without full ownership.

Why is 'income tax expense' often different from the 'taxable income'?

-Income tax expense is calculated based on accounting principles, while taxable income is determined by tax laws. These two figures often differ due to temporary or permanent differences in the recognition of revenue or expenses, which are reconciled through deferred taxes.

What is the 'minority interest' in an income statement?

-Minority interest represents the portion of net income attributable to shareholders who do not own a controlling stake in a subsidiary. It is deducted from the parent company's net income in consolidated financial reports.

How is 'earnings per share' (EPS) calculated and why is it important?

-EPS is calculated by dividing net income by the weighted average number of outstanding shares during the period. It helps investors assess the profitability of a company on a per-share basis, making it easier to compare companies of different sizes.

Outlines

This section is available to paid users only. Please upgrade to access this part.

Upgrade NowMindmap

This section is available to paid users only. Please upgrade to access this part.

Upgrade NowKeywords

This section is available to paid users only. Please upgrade to access this part.

Upgrade NowHighlights

This section is available to paid users only. Please upgrade to access this part.

Upgrade NowTranscripts

This section is available to paid users only. Please upgrade to access this part.

Upgrade NowBrowse More Related Video

5.0 / 5 (0 votes)