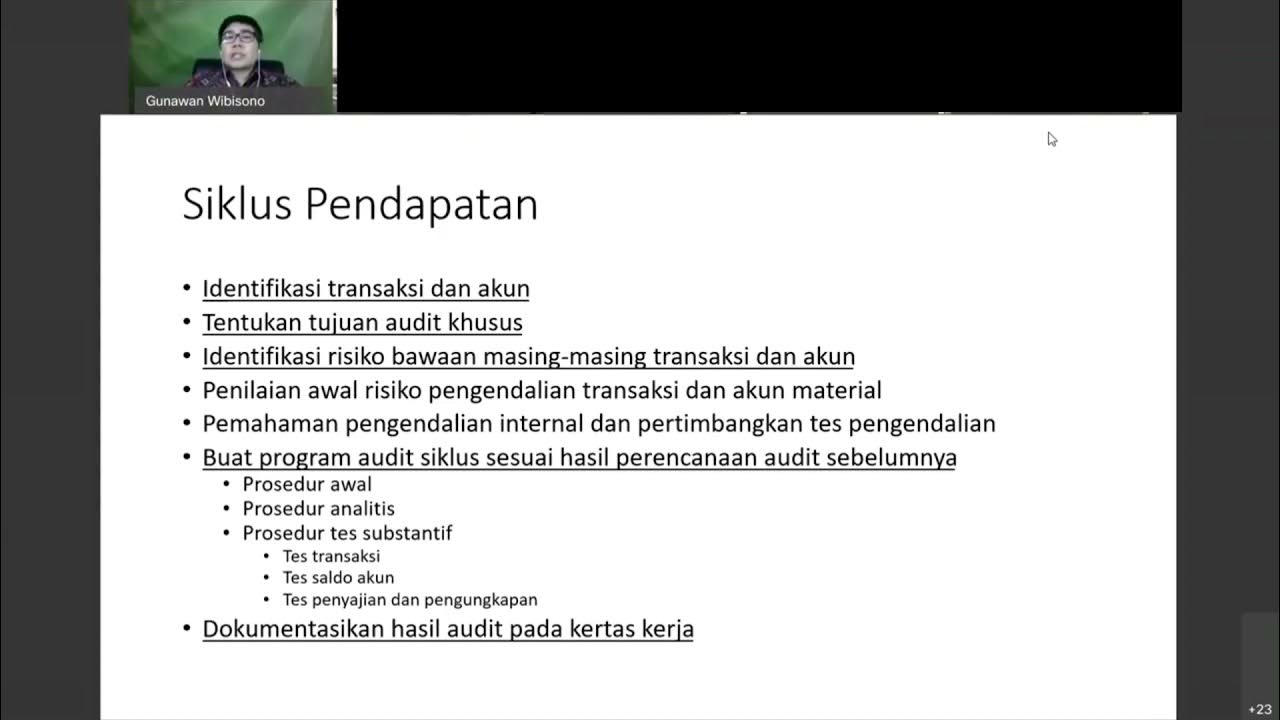

Auditing bank loans and borrowings

Summary

TLDRThis video provides a detailed guide on auditing long-term bank loans, focusing on both testing internal controls and gathering substantive evidence. Key areas include verifying loan existence, completeness, accuracy, classification, and ensuring proper interest expense recording. Auditors are advised to trace interest payments to journal entries and check for correct period reporting. It also emphasizes the importance of proper loan documentation, approval, and classification, ensuring accurate financial reporting. The content serves as a comprehensive resource for auditing bank loans, offering practical insights and tips for effective audits.

Takeaways

- 😀 Tracing involves moving forward in time, starting with bank documents and ensuring journal entries are recorded accurately.

- 😀 A missing interest payment can be identified during tracing, helping rectify discrepancies in the journal entries.

- 😀 Cutoff testing ensures that transactions are recorded in the correct accounting period, especially around the end of the financial year.

- 😀 Interest calculations for loans should be properly applied to the correct period, avoiding issues like pushing interest into the wrong month.

- 😀 Auditors should check journal entries for a month on either side of the financial year-end to ensure correct period classification.

- 😀 Classification testing ensures that the correct account codes are used in journal entries, based on the company's chart of accounts.

- 😀 The chart of accounts includes specific codes for subsidiaries and different loan types, helping ensure accurate classification of transactions.

- 😀 When tracing, auditors should confirm that the debit and credit amounts are posted to the correct accounts as per the chart of accounts.

- 😀 The script encourages viewers to contribute suggestions for additional testing methods or examples they would like analyzed.

- 😀 The video emphasizes the importance of auditing both controls and substantive testing to ensure accurate and complete financial reporting.

- 😀 The speaker invites viewers to subscribe for future content and engage by commenting with suggestions or questions on auditing processes.

Q & A

What is the primary purpose of auditing long-term bank loans and borrowings?

-The primary purpose is to assess whether the bank loans and borrowings are accurately recorded and classified in the financial statements, ensuring compliance with accounting principles and regulations.

What is the difference between testing controls and substantive testing in the context of bank loans?

-Testing controls involves evaluating the company's internal processes and checks to ensure proper recording of transactions, while substantive testing focuses on verifying the accuracy of specific journal entries and financial data related to loans.

Why is it important to trace interest payments to the journal entries during an audit?

-Tracing interest payments to journal entries helps ensure that all payments are accurately recorded, and identifies any discrepancies, such as missing entries, which need to be rectified.

How does the cutoff test impact the auditing of bank loans?

-The cutoff test ensures that interest expenses are recorded in the correct financial period. It helps verify that no interest payments are recorded in the wrong period, especially at the end of financial periods like June 30.

What is the role of the chart of accounts in classifying journal entries during an audit?

-The chart of accounts provides a master list of account codes used to classify transactions accurately. It helps ensure that journal entries are posted to the correct accounts, such as specific loans or subsidiaries, ensuring accurate financial reporting.

How does an auditor ensure the correct period is used for interest expenses?

-An auditor reviews journal entries around the end of the financial period to confirm that interest expenses are recorded in the correct period, ensuring no improper deferrals or adjustments are made.

What is meant by 'tracing' in auditing and how does it relate to bank loans?

-'Tracing' in auditing refers to following a transaction from its origin to its final accounting entry. In the context of bank loans, it involves following interest payments from bank documents to journal entries to ensure all transactions are correctly recorded.

What specific documents should be used when auditing bank loans?

-Bank statements are a key document to review when auditing bank loans. These statements are used to trace interest payments and validate that journal entries are accurately recorded.

How does an auditor identify missing or unrecorded interest payments?

-By tracing interest payments from bank statements to the journal entries, auditors can identify any discrepancies, such as missing interest payments, that need to be corrected.

What is the significance of testing substantive procedures for bank loans and borrowings?

-Testing substantively helps verify the accuracy and completeness of financial records by checking specific transactions, such as interest payments and journal entries, to ensure they align with the financial statements.

Outlines

This section is available to paid users only. Please upgrade to access this part.

Upgrade NowMindmap

This section is available to paid users only. Please upgrade to access this part.

Upgrade NowKeywords

This section is available to paid users only. Please upgrade to access this part.

Upgrade NowHighlights

This section is available to paid users only. Please upgrade to access this part.

Upgrade NowTranscripts

This section is available to paid users only. Please upgrade to access this part.

Upgrade Now

5.0 / 5 (0 votes)