PPH PASAL 22 - PART 2

Summary

TLDRThis transcript provides a comprehensive explanation of the PPh Pasal 22 tax system, focusing on various provisions under the Minister of Finance Regulation No. 34/PMK.01/2017. It details the entities responsible for collecting the tax, the applicable rates, and special conditions such as exemptions for certain goods and transactions. Throughout the transcript, several case examples are used to illustrate how the tax is calculated in different scenarios, including imports, purchases by government entities, and sales of specific goods like fuel, automobiles, and gold. The content emphasizes understanding the legal framework and applying it to real-world tax situations.

Takeaways

- 😀 The PPH Pasal 22 tax collector includes entities such as banks, government treasurers, certain state-owned enterprises (SOEs), and producers of specific industries like cement, paper, automotive, and pharmaceuticals.

- 😀 PPH Pasal 22 is a tax levied on specific transactions, including sales by industries such as automotive and fuel, importers, and certain business sectors like mining and gold.

- 😀 The basic legal framework for PPH Pasal 22 is provided by Regulation No. 34/PMK.01/2017, which outlines the specific conditions and entities involved in tax collection.

- 😀 PPH Pasal 22 has a higher tax rate for individuals or entities without a Taxpayer Identification Number (NPWP), as in the case of Bu Tita’s purchase of gold bars.

- 😀 The standard tax rate for gold bar sales is 0.45%, but if the buyer does not have an NPWP, the tax rate doubles to 0.9%.

- 😀 For imports, the tax is applied based on the total cost, including the import cost, insurance, and freight charges. The applicable tax rate is 2.5% for importers with the appropriate permits (API, APIS, or APIT).

- 😀 There are exemptions to PPH Pasal 22, such as for government payments not exceeding Rp2 million or transactions involving certain goods, like museum artifacts or charitable donations.

- 😀 The tax on the sale of goods like automobiles or luxury items is subject to specific rates under PPH Pasal 22, such as 5% for high-value items like luxury apartments or cars.

- 😀 Transactions involving sales of chemical products or pharmaceuticals to companies like PT Petrokimia Gresik are also subject to PPH Pasal 22, depending on the value of the transaction.

- 😀 The timing for PPH Pasal 22 payments depends on the nature of the transaction, such as payment at the time of importation or when government-related purchases occur, as outlined in Regulation No. 34/PMK.01/2017.

Q & A

What is the basis for the collection of PPh Pasal 22 in Indonesia?

-The basis for the collection of PPh Pasal 22 is outlined in the Peraturan Menteri Keuangan (PMK) No. 34/PMK.01/2017, which defines various entities and situations that are required to collect this tax. These include certain government bodies, state-owned enterprises, and specific industries such as banking, automotive, and mining, among others.

Which entities are included as collectors of PPh Pasal 22 according to PMK No. 34/PMK.01/2017?

-Entities that collect PPh Pasal 22 include banks, the Directorate General of Customs and Excise (DJBC), government treasurers, state-owned enterprises (BUMN), certain industrial sectors (e.g., cement, paper, automotive), and fuel distributors, among others.

What happens if a taxpayer does not present a tax identification number (NPWP) when purchasing gold bullion?

-If a taxpayer does not present their NPWP when purchasing gold bullion, the applicable PPh Pasal 22 rate is doubled, as stated in PMK No. 34/PMK.01/2017, which specifies a 0.45% rate that becomes 0.90% for those without an NPWP.

How is the PPh Pasal 22 calculated when a taxpayer buys gold bullion worth IDR 5.6 million?

-The PPh Pasal 22 is calculated as follows: the standard rate is 0.45%, but since the buyer does not have an NPWP, the rate is doubled to 0.90%. Therefore, the tax is 0.90% of IDR 5.6 million, which equals IDR 5,400.

What are the key factors in calculating the PPh Pasal 22 for an importer?

-The key factors in calculating PPh Pasal 22 for imports include the cost of goods, shipping costs, insurance premiums, and other fees, all converted into Indonesian Rupiah based on the applicable exchange rate. Additionally, the tax rate for importers with a valid API (importer identification number) is 2.5%.

How is the PPh Pasal 22 calculated for imports when the cost of goods is USD 80,000 and other associated fees are considered?

-The calculation involves adding up the total value of the goods, shipping costs, insurance premiums, and other applicable fees. After converting all costs into IDR (based on an exchange rate of IDR 10,000 per USD), the total import value is IDR 910,200,000. With an API holder, the tax is 2.5% of this value, resulting in a tax of IDR 22,750,000.

Under what circumstances is PPh Pasal 22 not applied to transactions involving the government?

-PPh Pasal 22 is not applied to government payments for transactions under IDR 2 million, as outlined in PMK No. 34/PMK.01/2017. This applies to payments made by government treasurers or budget authorities, provided they are not part of larger transactions split into smaller payments.

What is the PPh Pasal 22 rate for sales of automotive products in Indonesia?

-The PPh Pasal 22 rate for sales of automotive products to domestic distributors is set at 0.45% of the selling price, as per PMK No. 34/PMK.01/2017.

How is the PPh Pasal 22 calculated for the sale of luxury goods like automobiles?

-For luxury goods like automobiles, if the vehicle's value exceeds IDR 5 billion or has an engine capacity above 3,000cc, the applicable PPh Pasal 22 rate is 5%, excluding value-added tax (VAT) and luxury goods tax (LGT).

What are the exemptions for PPh Pasal 22 on imported goods according to PMK No. 34/PMK.01/2017?

-Exemptions from PPh Pasal 22 on imported goods include items such as gifts for social, religious, or cultural purposes, items for museums or zoos, and goods imported by foreign diplomatic missions. These are outlined in PMK No. 34/PMK.01/2017, specifically in Article 3, which provides various exceptions.

Outlines

This section is available to paid users only. Please upgrade to access this part.

Upgrade NowMindmap

This section is available to paid users only. Please upgrade to access this part.

Upgrade NowKeywords

This section is available to paid users only. Please upgrade to access this part.

Upgrade NowHighlights

This section is available to paid users only. Please upgrade to access this part.

Upgrade NowTranscripts

This section is available to paid users only. Please upgrade to access this part.

Upgrade NowBrowse More Related Video

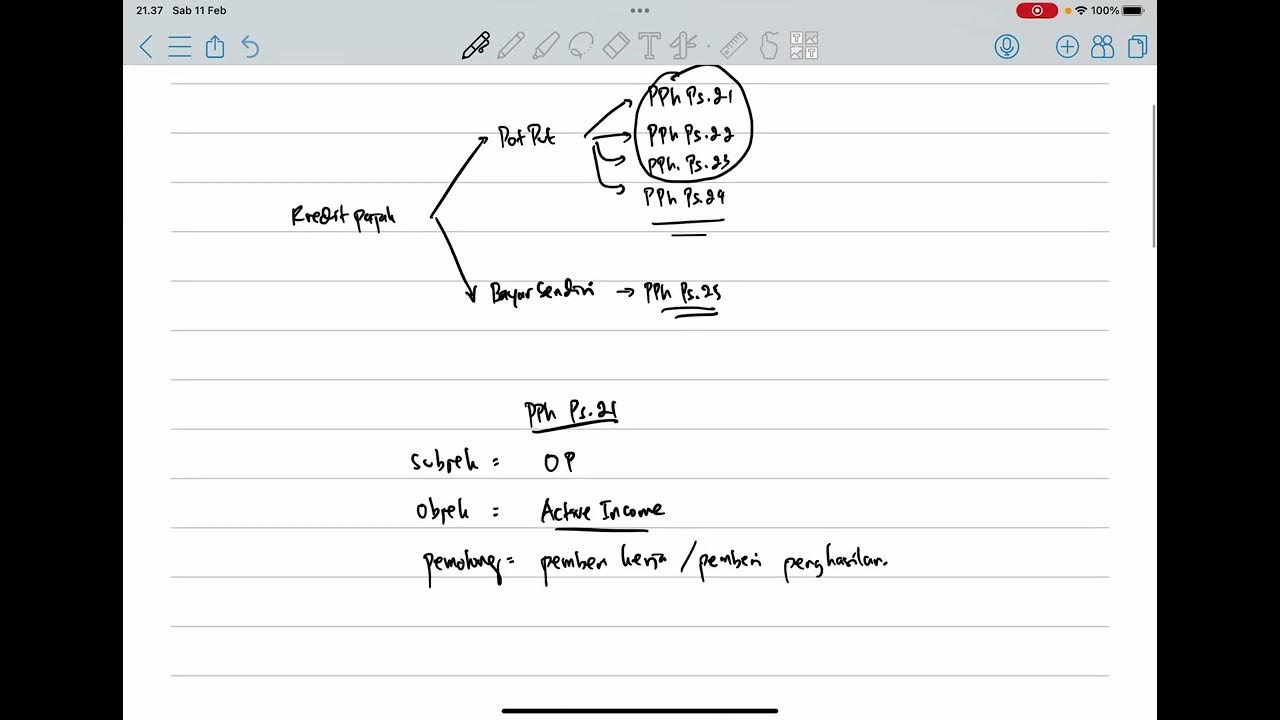

PPh Orang Pribadi (Update 2023) - 5. Kredit Pajak

Tips memahami apa saja jenis pajak perusahaan yang harus Anda laporkan

Perbedaan Pemotongan & Pemungutan Pajak || Withholding Tax #tutorialpajak

Pengenalan PPh Pasal 22, tarif PPh Pasal 22, dan Contoh Soal PPh Pasal 22

E-FUNLEARNING HMAK: PERPAJAKAN PPH PASAL 28 DAN 29

Cara Mudah Memahami PPh Pasal 22

5.0 / 5 (0 votes)