D-III AKUNTANSI_SEKTOR PUBLIK Pertemuan 1(Konsep Dasar Dan Karakteristik Lingkungan Sektor Publik)

Summary

TLDRIn this session on public sector accounting, Ibu Nesya introduces key concepts including the role of public sector accounting in managing resources for public goods and services. She highlights the unique characteristics of the public sector, such as its non-profit goals, reliance on taxes and bonds for funding, and its bureaucratic organizational structure. The session contrasts the public and private sectors, explaining similarities in resource management and legal frameworks while focusing on differences in objectives, funding sources, accountability, and accounting systems. The session concludes with a discussion on the importance of public sector accounting for efficient governance and management.

Takeaways

- 😀 The course being discussed is Public Sector Accounting, focusing on basic concepts and the characteristics of the public sector environment.

- 😀 The learning objectives for the first meeting include understanding the basics of the public sector and public sector accounting, and identifying the differences and similarities between the public and private sectors.

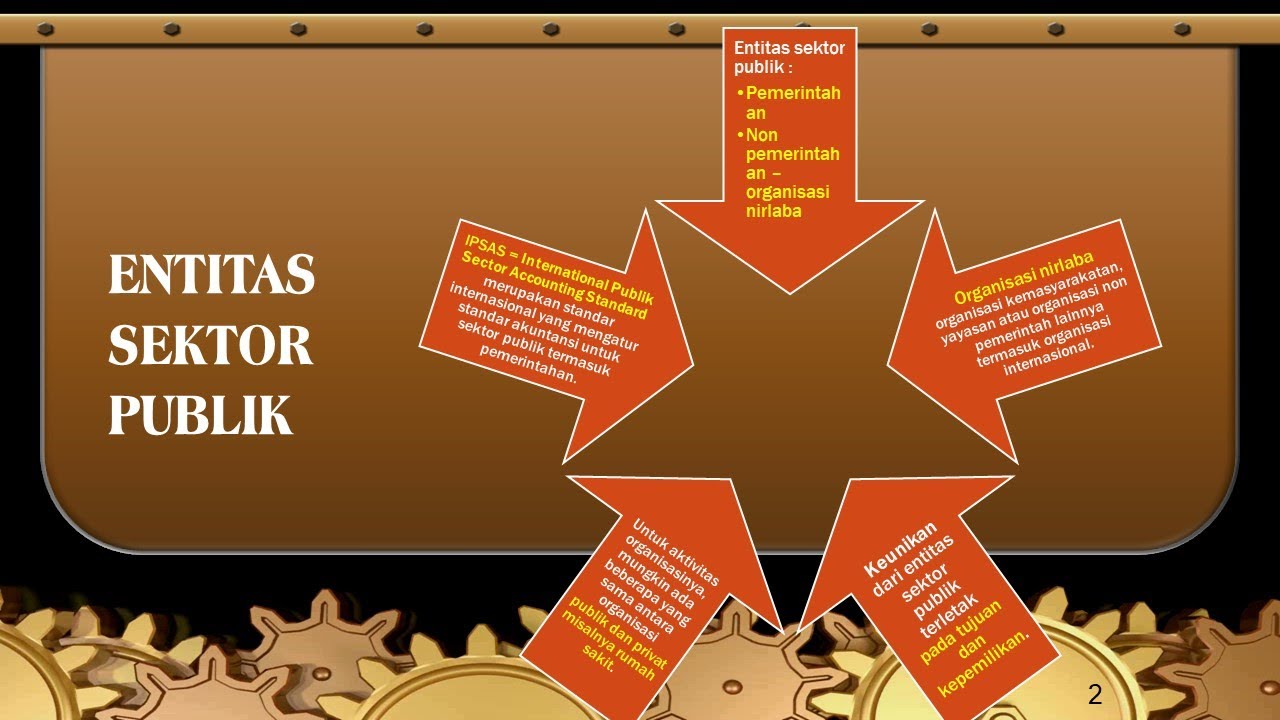

- 😀 Public sector accounting involves recording, classifying, and reporting financial information related to the production of public goods and services to meet public needs.

- 😀 Public sector accounting is different from private sector accounting in that it is often used by government agencies at both the regional and national levels.

- 😀 Both the public and private sectors share common characteristics such as being integral parts of the economy, facing resource scarcity, and requiring efficient and effective resource management.

- 😀 The management control process is similar in both sectors, requiring reliable and relevant financial information for decision-making.

- 😀 Both sectors are bound by legal regulations and rules, and they must adhere to laws governing their operations.

- 😀 The key difference between the public and private sectors lies in their goals—public sector entities are non-profit, while private sector organizations focus on maximizing profit.

- 😀 Public sector funding comes from taxes, government bonds, and public assets, while private sector financing comes from internal funds, retained earnings, and external sources like bank loans and stock issuance.

- 😀 Accountability in the public sector is to the public and parliament, while in the private sector, accountability is to shareholders and creditors.

Q & A

What is the main objective of public sector accounting?

-The main objective of public sector accounting is to record, classify, and report financial information related to the provision of goods and services for public needs, ensuring efficient use of public resources.

How does public sector accounting differ from private sector accounting?

-Public sector accounting differs from private sector accounting primarily in that the public sector is non-profit and focuses on fulfilling public needs, while the private sector is profit-driven and aims to maximize earnings.

What are some key characteristics of public sector accounting?

-Key characteristics of public sector accounting include its application within government entities, its non-profit nature, and its reliance on public funding sources like taxes, retributions, and government bonds.

What are the similarities between the public and private sectors?

-Both the public and private sectors are integral to the economy, face challenges of resource scarcity, and must manage resources effectively. They also both follow legal frameworks and regulations to ensure accountability.

What are the main sources of funding for the public sector?

-The public sector is funded through taxes, retributions, government debt (like bonds), profits from state-owned enterprises (BUMN/BUMD), and the sale of state assets.

How is accountability structured in the public sector compared to the private sector?

-In the public sector, accountability is directed towards the public and legislative bodies such as the parliament (DPR or MPR), while in the private sector, accountability is to shareholders, creditors, and stakeholders involved in the business.

What is the typical structure of organizations in the public and private sectors?

-Public sector organizations typically have a bureaucratic, hierarchical structure, while private sector organizations often have more flexible structures, such as flat or pyramid-shaped hierarchies.

What is the key difference in the budget transparency between the public and private sectors?

-Public sector budgets are generally open and available to the public for scrutiny, while private sector budgets are more restricted and are only shared with relevant stakeholders, such as shareholders or regulatory bodies.

What is the accounting method used in the public sector?

-The public sector typically uses cash accounting, where transactions are recorded when cash is received or paid, whereas the private sector uses accrual accounting, recognizing transactions when they occur, regardless of cash flow.

What are the external stakeholders in the public sector?

-External stakeholders in the public sector include the general public, taxpayers, businesses and organizations that use public services, international bodies like the IMF or World Bank, and future generations.

Outlines

This section is available to paid users only. Please upgrade to access this part.

Upgrade NowMindmap

This section is available to paid users only. Please upgrade to access this part.

Upgrade NowKeywords

This section is available to paid users only. Please upgrade to access this part.

Upgrade NowHighlights

This section is available to paid users only. Please upgrade to access this part.

Upgrade NowTranscripts

This section is available to paid users only. Please upgrade to access this part.

Upgrade NowBrowse More Related Video

Akuntansi Sektor Publik Sesi 1

[MEET 10-1] AKUNTANSI SEKTOR PUBLIK - AKUNTANSI ASET & KEWAJIBAN

RESUMÃO CONTABILIDADE PÚBLICA: TUDO O QUE VOCÊ PRECISA SABER

Akuntansi Sektor Publik (Karakteristik dan Ruang Lingkup)

PENGANTAR AKUNTANSI SEKTOR PUBLIK

CONTABILIDADE PÚBLICA PARA CONCURSOS - AULA 02 - PARTE 02/03 - NOÇÕES DE PCASP

5.0 / 5 (0 votes)