Materi Akuntasi Pemerintah Daerah Kelas 11 Praktikum Akuntansi Lembaga

Summary

TLDRThe video covers the topic of Government Accounting, specifically focusing on regional government accounting structures. It explains the relationship between the central government and regional offices, including the roles of the PPKD (Regional Finance Manager) and SKPD (Regional Work Units). The video delves into cash flow transactions, the two accounting methods used in government (cash-based and accrual-based), and introduces key government financial reports. The video also highlights the accounting principles, account types, and the accounting cycle for government institutions, aimed at providing a comprehensive understanding of government accounting practices.

Takeaways

- 😀 The video focuses on the topic of Government Accounting, particularly in local government entities like provinces, cities, and districts.

- 😀 It discusses the structure of accounting in local government, comparing it to private sector organizations with concepts like Head Office and Branch Office.

- 😀 In local government accounting, 'PKKD' refers to the regional financial management officer, and 'SKPD' refers to the regional government work units.

- 😀 The cash flow system in local government is explained with two types of payments: LS (Direct Payment) and UP (Advance Payments for Expenditures).

- 😀 For cash inflows, the script emphasizes the process of revenue collection and how local governments deposit these funds into central government accounts.

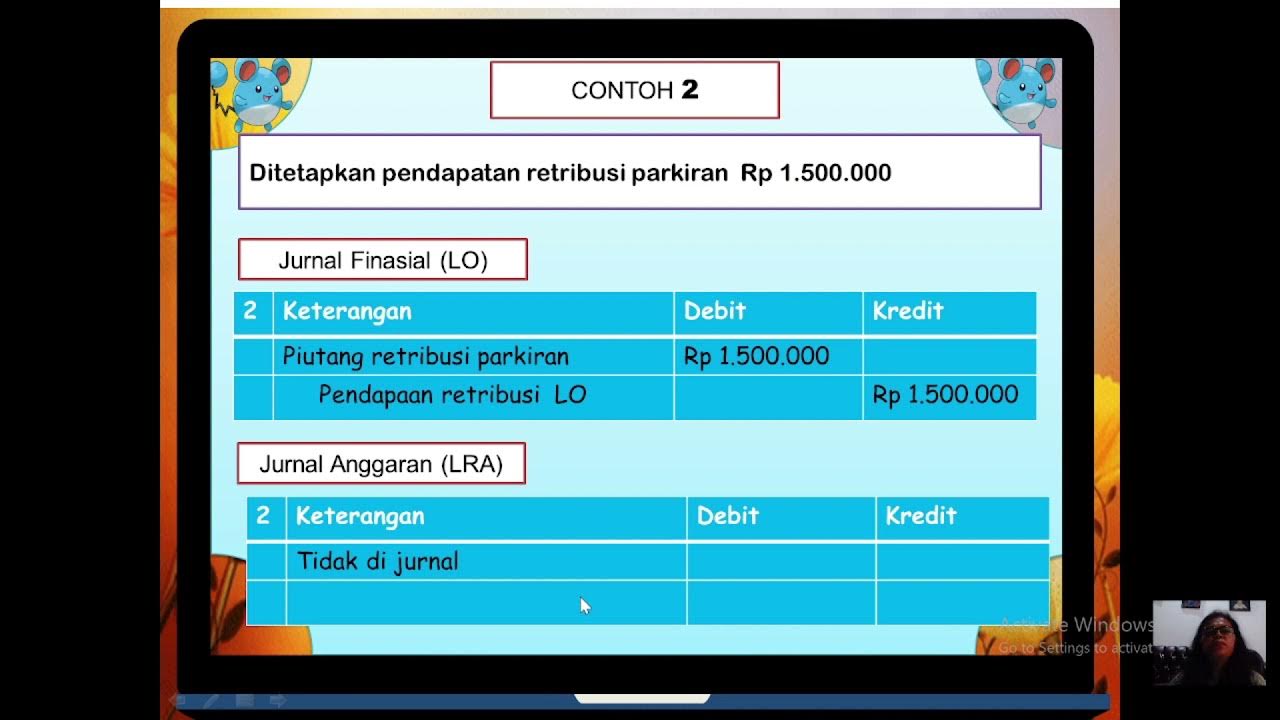

- 😀 Local governments use two accounting bases: cash basis for transactions related to cash inflows and outflows, and accrual basis for operational and balance sheet transactions.

- 😀 Cash basis accounting records all transactions related to cash movements, while accrual accounting includes broader financial transactions, affecting operational reports and balance sheets.

- 😀 Government accounting produces several financial reports, including the Realization Budget Report, Operational Report, Equity Changes Report, Balance Sheet, and Notes to Financial Statements.

- 😀 The script introduces 9 types of accounts used in government accounting: assets, liabilities, equity, revenues, expenses, transfers, financing, income tax, and operational expenses.

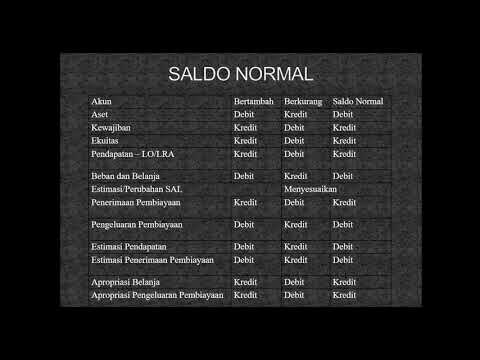

- 😀 The government accounting equation (Assets = Liabilities + Equity) is similar to the private sector, but it also includes the effects of both cash and accrual accounting, impacting the financial reporting process.

Q & A

What is the main focus of the video script?

-The video focuses on explaining the structure of accounting in local government institutions, specifically in Indonesia. It discusses topics such as the organizational structure, the flow of cash, accounting systems, and various financial reports.

What is the meaning of 'full book' or 'head office and branch office' in local government accounting?

-In local government accounting, the 'full book' refers to the main government body or central office (Head Office), while the 'branch office' represents the lower-level offices or entities like the Regional Work Units (SKPD) under the government.

How does the flow of cash work between PPKD and SKPD?

-Cash flows from the regional treasury (PPKD) to the SKPD through two types of systems: direct payments (LS) or cash advances (UP, Ganti Uang, and Tambah Uang). These cash flows are part of the budget management between the central government and local offices.

What are the two accounting bases used in local government accounting?

-Local government accounting uses both cash-based accounting and accrual-based accounting. Cash-based accounting records only cash inflows and outflows, while accrual accounting records all transactions, including those not yet involving cash.

What are the five types of financial reports in local government accounting?

-The five types of financial reports in local government accounting are: 1) Budget Realization Report, 2) Operational Report, 3) Equity Change Report, 4) Balance Sheet, and 5) Notes to Financial Statements.

What is the purpose of the 'Dokumen Pelaksanaan Anggaran' (DPA)?

-The 'Dokumen Pelaksanaan Anggaran' (DPA) serves as the basis for recording financial transactions in local government accounting. It is created as part of the preparation for the Regional Budget (APBD), guiding the subsequent transaction documentation and journal entries.

What is the relationship between SKPD and PPKD in local government accounting?

-The relationship between SKPD (Regional Work Units) and PPKD (Regional Treasury) is hierarchical and functional. SKPD handles operational tasks, while PPKD manages the financial resources and ensures the flow of funds to the SKPD for expenditure.

How does the accounting system in local government differ from private sector accounting?

-The main difference is that local government accounting uses two accounting systems simultaneously: cash-based and accrual-based. In contrast, private sector accounting typically uses only accrual-based accounting.

What are the nine types of accounts in local government accounting?

-The nine types of accounts in local government accounting are: 1) Assets, 2) Liabilities, 3) Equity, 4) Revenues, 5) Expenditures, 6) Transfers, 7) Financing, 8) Revenues from non-operating activities, and 9) Expenses.

What is the role of the 'Bendahara' in local government accounting?

-The 'Bendahara' (Treasurer) in local government accounting is responsible for managing cash flow within different units. There are two types of Bendahara: Bendahara Pengeluaran (Expenditure Treasurer) and Bendahara Penerimaan (Revenue Treasurer), each managing different aspects of the government's finances.

Outlines

This section is available to paid users only. Please upgrade to access this part.

Upgrade NowMindmap

This section is available to paid users only. Please upgrade to access this part.

Upgrade NowKeywords

This section is available to paid users only. Please upgrade to access this part.

Upgrade NowHighlights

This section is available to paid users only. Please upgrade to access this part.

Upgrade NowTranscripts

This section is available to paid users only. Please upgrade to access this part.

Upgrade NowBrowse More Related Video

Akuntansi Pemerintahan Daerah (gambaran umum)

Pengantar Akuntansi Pemerintah Kelas XI SMK

JURNAL SKPD AKUNTANSI PEMERINTAHAN

KD 3.2 Bidang , profesi dan etika profesi akuntansi

JURNAL PENCATATAN AKUNTANSI PEMERINTAH

Materi Siklus Akuntansi Pemerintah Daerah ~ Kelas 11 ~ Praktikum Akuntansi Lembaga (Part 2)

5.0 / 5 (0 votes)