PENGANTAR AKUNTANSI 1 - JURNAL

Summary

TLDRThis video introduces the basics of accounting, focusing on journals, which are crucial records of financial transactions within a company. It explains the different types of accounts such as assets, liabilities, equity, income, and expenses. The video also discusses how to record transactions like cash deposits, rent payments, and purchases using the general journal. Through various examples, including setting up a tutoring business, it shows how to log transactions properly and emphasizes the importance of understanding key accounting principles to ensure accurate financial reporting.

Takeaways

- 📚 The course covers 'Introduction to Accounting 1', focusing on financial journal entries.

- 📝 A journal is the first stage in the accounting process, recording a company's financial transactions.

- 🏢 Example journal entry: PT Musi Indah, with the report being a General Journal for the period ending December 31, 2000X.

- 💵 Major accounting categories include assets, liabilities, equity, revenue, and expenses.

- 🔑 Assets are divided into current and non-current; current assets include cash, receivables, and prepaid expenses, while non-current assets include equipment, buildings, and land.

- 🏦 Liabilities are split into short-term (due within a year) and long-term (due after a year), with examples like accrued liabilities, accounts payable, and bonds.

- 👥 Equity includes capital, retained earnings, and owner withdrawals (prive).

- 💼 Revenue is classified into operating (from core business) and non-operating (such as rental or interest income).

- ⚡ Expenses include regular outflows like rent, wages, utilities, and are reported in the income statement.

- 👩🏫 Students are tasked with creating a journal for a company named Selalu Dharma, covering transactions during May 1988.

Q & A

What is the purpose of a journal in accounting?

-A journal is used to record financial transactions in a company. It is the first step in the accounting process, where each transaction is systematically documented.

What are the five major types of accounts in accounting?

-The five major types of accounts are assets, liabilities, equity (capital), revenues, and expenses.

How are assets classified in accounting?

-Assets are classified into two types: current assets (such as cash, accounts receivable, and prepaid expenses) and non-current assets (such as equipment, accumulated depreciation, vehicles, and buildings).

What distinguishes short-term liabilities from long-term liabilities?

-Short-term liabilities are obligations due within one year (e.g., accrued liabilities, accounts payable), while long-term liabilities are due after one year (e.g., bank loans, mortgages).

What is a common example of a short-term liability?

-A common example of a short-term liability is accrued expenses, such as wages payable, tax payable, or rent payable.

What constitutes equity in accounting?

-Equity in accounting includes capital (initial investment), withdrawals by the owner (drawings or 'prive'), and retained earnings (profit kept in the business for future use).

What are operating and non-operating revenues?

-Operating revenues come from core business activities, such as sales, while non-operating revenues come from sources outside regular operations, like interest or rent income.

What types of expenses are commonly found in a business?

-Common expenses include rent, salaries, utilities (like electricity and water), and other routine operating expenses.

What is the journal entry when cash is contributed to a business as initial capital?

-The journal entry would be: Debit 'Cash' and Credit 'Capital' for the contributed amount.

How would you record an expense for prepaid rent in the journal?

-The journal entry for prepaid rent would be: Debit 'Prepaid Rent' and Credit 'Cash' for the rent amount.

Outlines

This section is available to paid users only. Please upgrade to access this part.

Upgrade NowMindmap

This section is available to paid users only. Please upgrade to access this part.

Upgrade NowKeywords

This section is available to paid users only. Please upgrade to access this part.

Upgrade NowHighlights

This section is available to paid users only. Please upgrade to access this part.

Upgrade NowTranscripts

This section is available to paid users only. Please upgrade to access this part.

Upgrade NowBrowse More Related Video

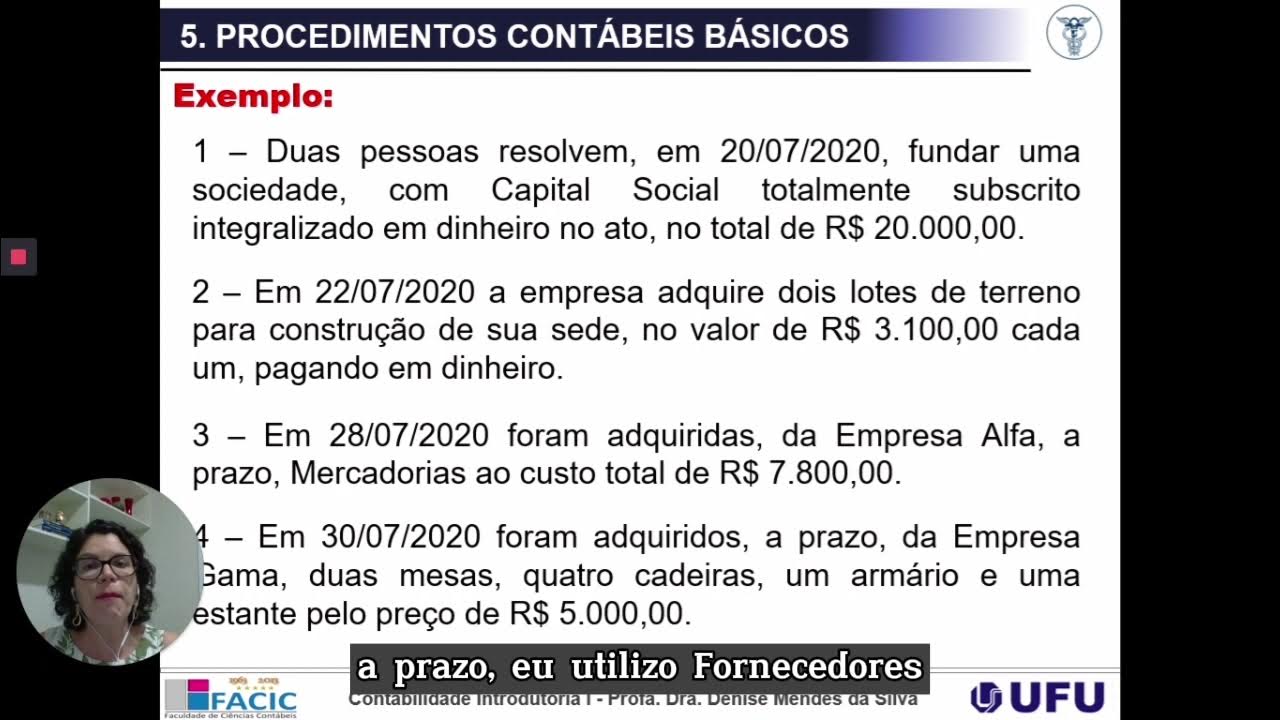

Vídeo Aula Exemplo Procedimentos Contábeis Básicos

Materi ke 1 Akuntansi Perusahaan Jasa (Kelas XI Akuntansi)

Apa Saja Tahap Pencatatan Akuntansi Perusahaan Jasa? | Ekonomi Kelas 12 | EDURAYA MENGAJAR

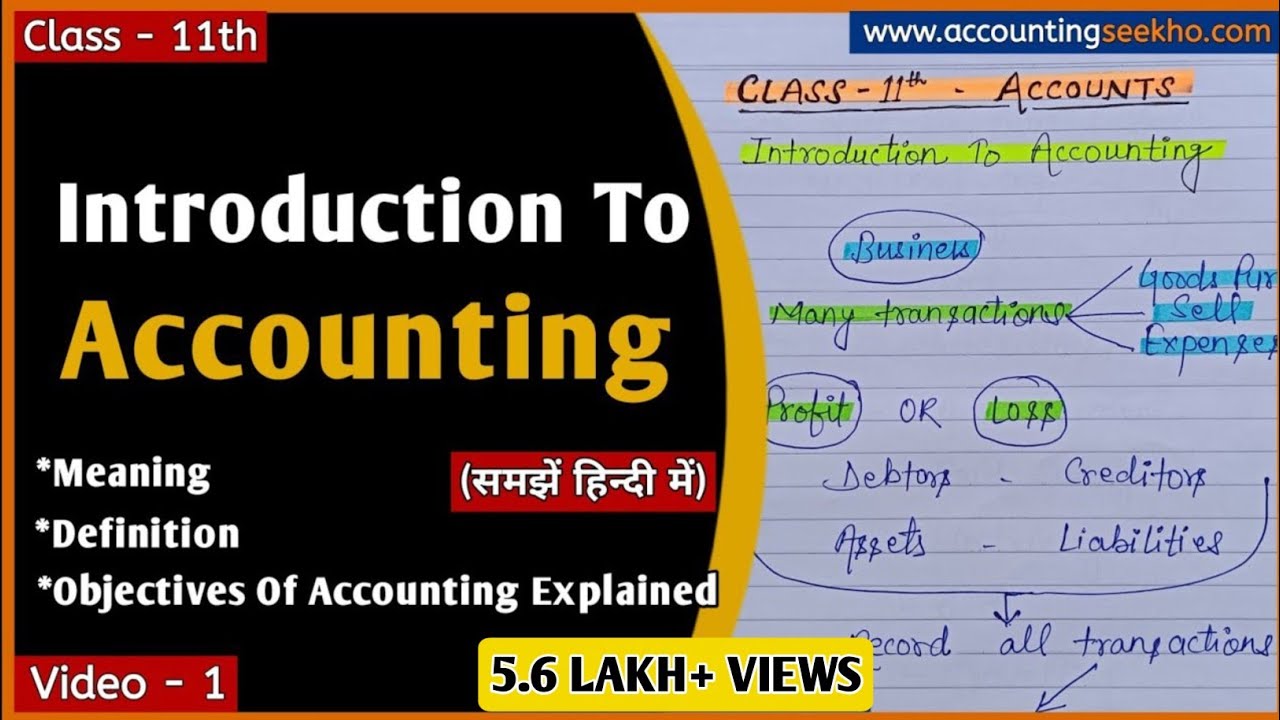

Introduction To Accounting | Meaning, Definition And Objectives Of Accounting | Class 11 Accounts |

T Accounts Explained SIMPLY (With 5 Examples)

86.Overviu PMK 212/2019 tentang Jurnal Akuntansi Pemerintah Pusat

5.0 / 5 (0 votes)