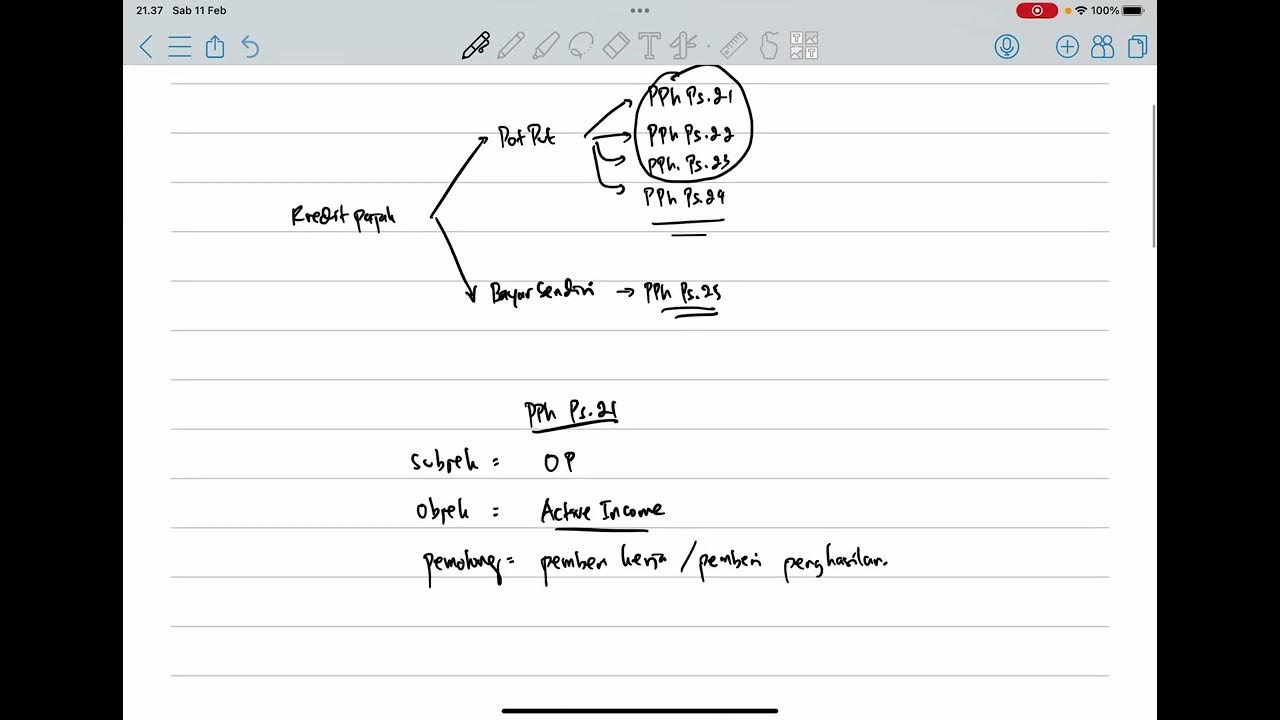

PPh Pasal 24: Pengertian, Subjek dan Objek, Cara Pelaksanaan Kredit, dan Studi Kasus

Summary

TLDRThis video explains Indonesia's PPh Pasal 24 tax regulation, which allows domestic taxpayers to claim a credit for foreign taxes paid on overseas income, thus reducing their domestic tax liability. The script covers key topics including the definition of tax, eligible foreign income, the process of applying for tax credits, and the calculation method. It also walks through a practical example of how to calculate the credit and the documentation required for the process. The video aims to help viewers understand how to leverage foreign tax credits to avoid double taxation.

Takeaways

- 😀 PPh Pasal 24 allows Indonesian taxpayers to credit foreign taxes paid against their domestic tax obligations.

- 😀 The goal of PPh Pasal 24 is to prevent double taxation on income earned abroad.

- 😀 Taxpayers must submit documents such as financial reports, foreign tax returns, and proof of tax payment to apply for the tax credit.

- 😀 The tax credit is limited to the lesser of the foreign taxes paid or a proportionate share of the total Indonesian tax owed.

- 😀 Eligible foreign income includes earnings from dividends, royalties, interest, rental income, and business operations abroad.

- 😀 The provision applies to Indonesian taxpayers earning income both within Indonesia and from foreign sources.

- 😀 To calculate the tax credit, the taxpayer’s foreign income is combined with domestic income, and the applicable tax rate is determined based on total income.

- 😀 If foreign taxes exceed the domestic tax liability, the excess cannot be credited in Indonesia, ensuring the credit doesn’t surpass the domestic tax amount.

- 😀 Taxpayers must report foreign tax payments during their annual tax filings, ensuring transparency and compliance with local tax authorities.

- 😀 By providing a foreign tax credit, PPh Pasal 24 encourages international business and helps make cross-border operations more tax-efficient.

Q & A

What is the purpose of taxes according to the script?

-Taxes are a source of state revenue used to finance government expenditures and operations. They are collected from the public and can be enforced without direct compensation.

What is PPh Pasal 24?

-PPh Pasal 24 is a regulation that allows taxpayers to use foreign tax credits to reduce the amount of tax payable in Indonesia on income earned abroad.

What does Article 24 of the Indonesian Tax Law state about foreign tax credits?

-Article 24 of the Indonesian Tax Law allows taxpayers to credit foreign taxes paid on income from abroad against their Indonesian tax liabilities, preventing double taxation.

Which income is eligible for foreign tax credit under PPh Pasal 24?

-Eligible income includes earnings from dividends, royalties, interest, rental income, business operations abroad, capital gains from asset transfers, and other forms of income derived from foreign sources.

How is the foreign tax credit calculated?

-The foreign tax credit is calculated based on the tax paid or owed abroad, up to a maximum of the Indonesian tax liability on the same foreign income.

What is the process for applying for a foreign tax credit?

-Taxpayers must submit an application to the Directorate General of Taxes, including financial reports of foreign income, a tax return filed abroad, and payment receipts for taxes paid outside Indonesia.

What is the maximum foreign tax credit that can be claimed?

-The maximum credit is the lower of the following: the foreign tax paid, the ratio of foreign income to total income multiplied by the total Indonesian tax, or the tax due on the total income at Indonesian rates.

What happens if the foreign tax credit exceeds the Indonesian tax due?

-The foreign tax credit cannot exceed the Indonesian tax payable on the total income. If it does, the excess credit will not be refunded.

What are the key requirements for reporting foreign income and taxes for a foreign tax credit claim?

-Taxpayers must report foreign income and taxes when filing their annual tax return, and they need to submit supporting documents such as foreign tax returns and payment receipts.

What is the case example used in the script to illustrate the foreign tax credit calculation?

-The example involves PT Kasturi, which earned 5 billion IDR from abroad with a tax rate of 40%. The total income was 9 billion IDR, and the creditable foreign tax was calculated based on the minimum of three factors: the foreign tax paid, the ratio of foreign income, and the tax payable at Indonesian rates.

Outlines

Этот раздел доступен только подписчикам платных тарифов. Пожалуйста, перейдите на платный тариф для доступа.

Перейти на платный тарифMindmap

Этот раздел доступен только подписчикам платных тарифов. Пожалуйста, перейдите на платный тариф для доступа.

Перейти на платный тарифKeywords

Этот раздел доступен только подписчикам платных тарифов. Пожалуйста, перейдите на платный тариф для доступа.

Перейти на платный тарифHighlights

Этот раздел доступен только подписчикам платных тарифов. Пожалуйста, перейдите на платный тариф для доступа.

Перейти на платный тарифTranscripts

Этот раздел доступен только подписчикам платных тарифов. Пожалуйста, перейдите на платный тариф для доступа.

Перейти на платный тарифПосмотреть больше похожих видео

PPh Orang Pribadi (Update 2023) - 5. Kredit Pajak

Perbedaan Pemotongan & Pemungutan Pajak || Withholding Tax #tutorialpajak

[PART 1- Watax] Pajak Penghasilan (PPh) Pasal 4 Ayat 2| Tax Center UIN Jakarta

PPh Pasal 25: Pengertian, Perhitungan, Penyetoran dan Pelaporan

Tips memahami apa saja jenis pajak perusahaan yang harus Anda laporkan

Dari Mana Saja Sumber Pemasukan Negara ?

5.0 / 5 (0 votes)