Lesson 029 - Accounting for Merchandising Operations 3: Income Statement

Summary

TLDRThis educational video script covers the fundamentals of preparing an income statement for merchandising operations. It introduces an additional adjusting entry for merchandise inventory, explains the process of adjusting entries, and outlines the steps to calculate net sales and cost of goods sold. The script also discusses two methods of presenting the income statement: the functional expense method and the nature of expense method. It concludes with a walkthrough of preparing an income statement using sample data, emphasizing the importance of understanding merchandising accounts and adjusting entries in financial reporting.

Takeaways

- 📊 The focus of the lesson is on preparing the income statement for merchandising operations.

- 🔧 A new adjusting entry is introduced for merchandise inventory, in addition to previous entries like prepaid expenses and depreciation.

- 💡 The adjusting entry involves debiting the profit or loss summary and crediting merchandise inventory at the beginning and end of the accounting period.

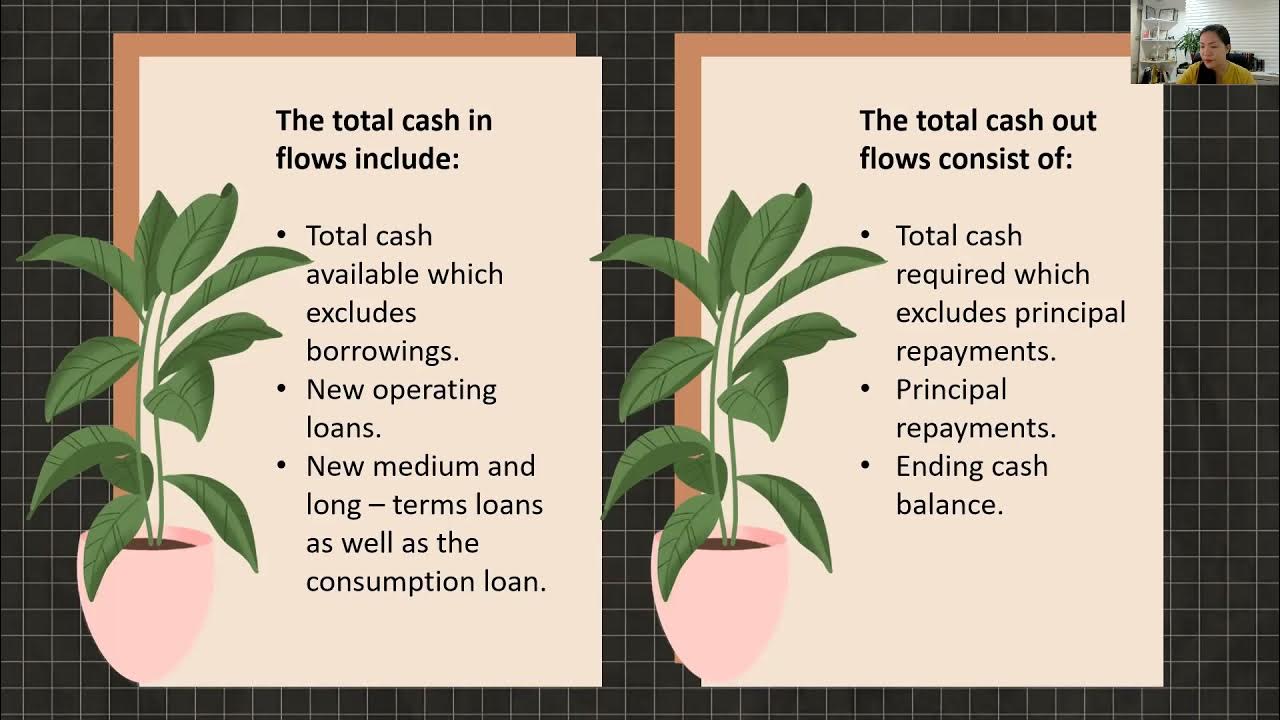

- 📈 The income statement for merchandising operations calculates net sales and gross profit, which is net sales minus cost of goods sold.

- 🛒 Net sales are determined by subtracting sales returns, allowances, and discounts from gross sales.

- 📦 The cost of goods sold is calculated by adding the beginning inventory to net purchases and subtracting the ending inventory.

- 🧾 There are two methods for presenting the income statement: the function of expense method and the nature of expense method.

- 📉 The function of expense method classifies expenses as cost of goods sold, while the nature of expense method aggregates them by nature.

- 📂 The pro forma calculation involves gross sales minus contra sales to obtain net sales, and a detailed calculation of cost of goods sold.

- 📝 In the example, the income statement shows total revenues minus operating expenses to derive net income, using the function of expense method.

Q & A

What is the main focus of the video script provided?

-The main focus of the video script is to discuss the preparation of the income statement for merchandising operations, including the necessary adjusting entries and the process of calculating net sales and cost of goods sold.

What is an adjusting entry and why is it necessary in merchandising operations?

-An adjusting entry is a journal entry made at the end of an accounting period to adjust revenues and expenses to reflect the actual financial performance of the company. In merchandising operations, it is necessary to make adjusting entries for merchandise inventory to ensure that the income statement accurately reflects the cost of goods sold and the ending inventory.

What is the difference between the periodic and perpetual inventory recording systems?

-The periodic inventory system records inventory transactions only at the end of an accounting period, while the perpetual inventory system records each inventory transaction as it occurs. The script mentions that the accounting process for adjusting entries is the same for both systems in merchandising companies.

How is net sales calculated in a merchandising income statement?

-Net sales are calculated by subtracting sales returns and allowances and sales discounts from gross sales. The formula provided in the script is: Net Sales = Gross Sales - Sales Returns and Allowances - Sales Discounts.

What is the formula to calculate cost of goods sold in a merchandising operation?

-The cost of goods sold is calculated using the formula: Cost of Goods Sold = Beginning Inventory + Net Purchases - Ending Inventory. Net Purchases are calculated by subtracting purchase returns and allowances and purchase discounts from gross purchases.

What are the two methods of presenting the income statement mentioned in the script?

-The two methods of presenting the income statement mentioned are the 'function of expense method' and the 'nature of expense method'. The former classifies expenses according to their function, while the latter aggregates expenses according to their nature.

What is the purpose of the handouts mentioned in the script?

-The handouts are meant to provide additional information and examples to help understand the concepts discussed in the video, such as the computation of net sales, net purchases, and the preparation of the income statement using the function of expense method and the nature of expense method.

How does the increase or decrease in merchandise inventory affect the income statement?

-An increase in merchandise inventory is shown as a negative figure in the income statement under the function of expense method, while a decrease is shown as positive. This reflects the impact of inventory changes on the cost of goods sold and, consequently, on the net income.

What are some of the operating expenses included in the income statement of a merchandising company?

-Some of the operating expenses mentioned in the script include salaries, utilities, rent, and depreciation. These expenses are subtracted from the total revenues to calculate the net income.

What is the closing entry process for a merchandising company as described in the script?

-The closing entry process for a merchandising company involves transferring the balances of certain accounts to the capital account. This includes sales returns and allowances, sales discounts, purchases, purchase returns and allowances, purchase discounts, freight in, operating expenses, and net income.

Outlines

このセクションは有料ユーザー限定です。 アクセスするには、アップグレードをお願いします。

今すぐアップグレードMindmap

このセクションは有料ユーザー限定です。 アクセスするには、アップグレードをお願いします。

今すぐアップグレードKeywords

このセクションは有料ユーザー限定です。 アクセスするには、アップグレードをお願いします。

今すぐアップグレードHighlights

このセクションは有料ユーザー限定です。 アクセスするには、アップグレードをお願いします。

今すぐアップグレードTranscripts

このセクションは有料ユーザー限定です。 アクセスするには、アップグレードをお願いします。

今すぐアップグレード関連動画をさらに表示

5.0 / 5 (0 votes)