Ekuitas

Summary

TLDRThis video provides a comprehensive explanation of equity in financial accounting, covering its definition, recognition, measurement, components, presentation, and changes within financial statements. The speakers explain how equity represents the residual interest of owners after liabilities are deducted from assets, along with the criteria and timing for equity recognition. The discussion also explores measurement methods under PSAK and IFRS, including historical cost and fair value approaches. In addition, the video details major equity components such as share capital, retained earnings, OCI, and non-controlling interests. It concludes with insights into equity presentation in financial reports and contemporary accounting issues related to financial instruments, share-based compensation, and IFRS convergence.

Takeaways

- 😀 Equity represents the residual interest of owners in a company's assets after deducting liabilities, calculated as Assets minus Liabilities.

- 📊 Recognition of equity is the process of recording changes in owners' rights in financial statements, triggered by transactions affecting the company.

- 📝 Equity is recognized when owners contribute capital, the company earns profit, dividends are distributed, new shares are issued, or changes occur in Other Comprehensive Income (OCI).

- 💰 Measurement of equity determines its monetary value in financial statements, using historical cost, current value, or residual methods.

- 🏛️ Components of equity include share capital, additional paid-in capital (agio), retained earnings, other comprehensive income (OCI), and non-controlling interest.

- 📈 Share capital reflects direct investment from shareholders and can consist of ordinary, preferred, and treasury shares.

- 📉 Retained earnings are accumulated net profits not yet distributed as dividends and can be influenced by profits, corrections, policy changes, and dividend payments.

- 🌐 OCI captures changes in value not recognized in profit or loss, including actuarial gains/losses, currency translation differences, fair value investments, cash flow hedges, and asset revaluations.

- 📑 Equity is presented in the statement of financial position after assets and liabilities, with separate disclosure for components like share capital, agio, treasury shares, OCI, retained earnings, and non-controlling interests.

- 🔄 Equity changes through owner transactions (share issuance, dividends, treasury shares) and comprehensive income, affecting retained earnings and OCI directly.

- ⚖️ Contemporary issues in equity reporting include classification of financial instruments (PSAK 50), share-based compensation (PSAK 53), business acquisitions and goodwill (PSAK 22), and convergence with IFRS standards like PSAK 71.

Q & A

What is the definition of equity in financial reporting?

-Equity is the residual interest of the owners in the assets of a company after deducting liabilities. It represents the owners' claim on the company's net assets.

How is equity calculated according to accounting standards?

-Equity is calculated as the difference between total assets and total liabilities: Equity = Assets - Liabilities.

What is the concept of equity recognition?

-Equity recognition is the process of recording changes in owners' interests in financial statements when transactions or events affect the company's equity.

What criteria must be met for equity components to be recognized?

-Equity components can be recognized if they are relevant (useful for decision-making) and faithfully represented (complete, honest, and free from material errors).

What are the main components of equity?

-The main components of equity are: 1) Share capital, 2) Additional paid-in capital (agio saham), 3) Retained earnings, 4) Other comprehensive income (OCI), and 5) Non-controlling interests.

How is share capital measured?

-Share capital is measured at the nominal value of shares. Additional paid-in capital (agio saham) represents the difference between the issue price and nominal value of shares.

What is Other Comprehensive Income (OCI) and how does it affect equity?

-OCI records gains and losses not recognized in the income statement but directly in equity. Components include actuarial gains/losses, foreign currency translation differences, revaluation surpluses, and certain investment gains/losses.

How are equity changes from owner transactions recorded?

-Changes from owner transactions, such as issuing new shares, paying dividends, buying back treasury shares, or issuing employee stock options, are recorded directly in equity and do not affect the income statement.

What are some contemporary issues affecting equity recognition and measurement?

-Contemporary issues include: 1) Classification of financial instruments as equity or liability (PSAK 50), 2) Share-based payment transactions (PSAK 53), 3) Business combinations and goodwill allocation (PSAK 22), and 4) IFRS convergence affecting equity reporting, such as PSAK 71.

Why is the measurement of equity important in financial reporting?

-Measurement ensures that equity is presented at a relevant and accurate monetary value, reflecting the true financial position of the company and aiding in decision-making for stakeholders.

How is equity presented in the financial statements?

-Equity is presented in the statement of financial position (balance sheet) as the third element after assets and liabilities. It is also detailed in the statement of changes in equity and disclosed in the notes to the financial statements.

What are the levels of fair value measurement for equity under PSAK 68?

-Level 1: based on active market prices; Level 2: based on observable data; Level 3: based on valuation techniques such as discounted cash flows.

Outlines

このセクションは有料ユーザー限定です。 アクセスするには、アップグレードをお願いします。

今すぐアップグレードMindmap

このセクションは有料ユーザー限定です。 アクセスするには、アップグレードをお願いします。

今すぐアップグレードKeywords

このセクションは有料ユーザー限定です。 アクセスするには、アップグレードをお願いします。

今すぐアップグレードHighlights

このセクションは有料ユーザー限定です。 アクセスするには、アップグレードをお願いします。

今すぐアップグレードTranscripts

このセクションは有料ユーザー限定です。 アクセスするには、アップグレードをお願いします。

今すぐアップグレード関連動画をさらに表示

AKM 1: 1-5 Pelaporan Keuangan & Standar Akuntansi (Laporan Keuangan)

UNNES Laporan Keuangan Konsolidasi pada Akuisisi Metode Biaya Perolehan 3

Assets, Liabilities & Equity: Made Easy!

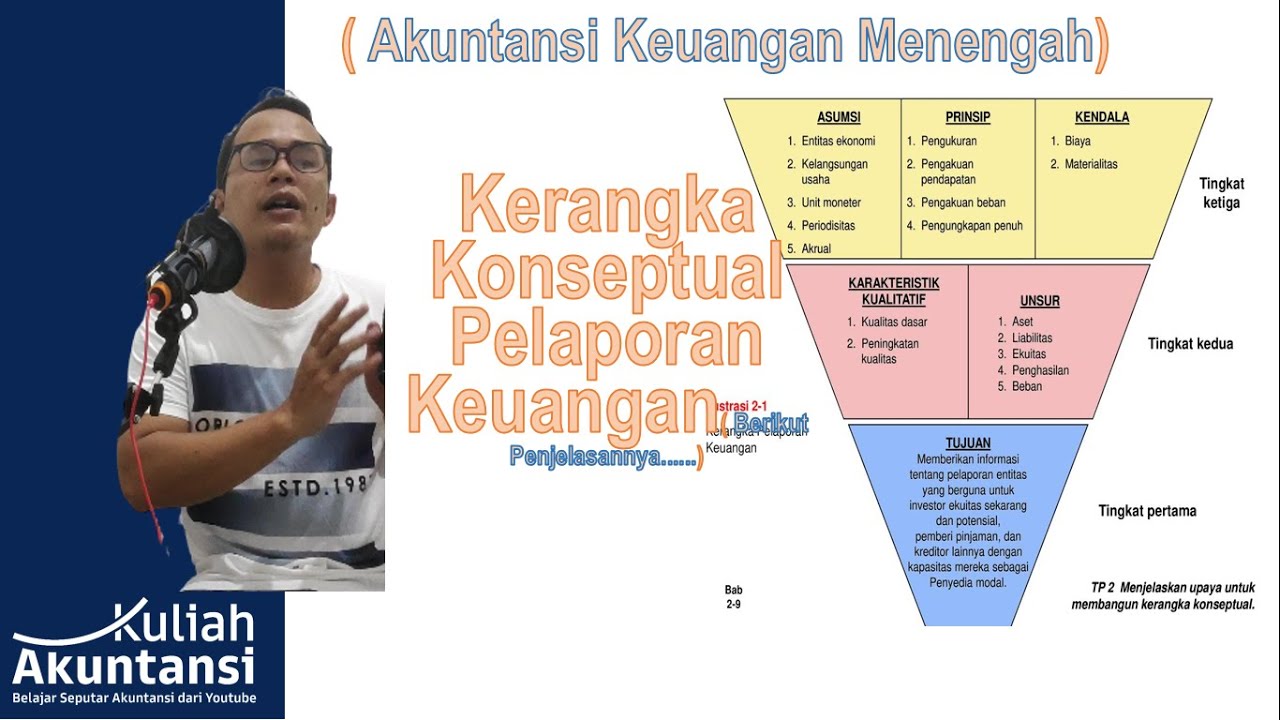

Akuntansi Keuangan Menengah : Kerangka Konseptual Pelaporan Keuangan

Chapter 5: Recognition and Derecognition

MENTORING - Akuntansi Keuangan Menengah 1 (Semester 2)

5.0 / 5 (0 votes)