Regulasi Fintech di Indonesia

Summary

TLDRThe video script discusses the regulation of fintech, specifically vintage, in Indonesia. It highlights the role of the Financial Services Authority (OJK) and Bank Indonesia in creating regulations to oversee the industry, ensuring consumer protection, financial stability, and compliance with anti-money laundering and counter-terrorism financing measures. The script mentions specific regulations like OJK 77/78 for peer-to-peer lending and BI 18/40/PBI/2016 for payment system providers, emphasizing the need for a robust legal framework to support the rapid growth of Indonesia's fintech sector.

Takeaways

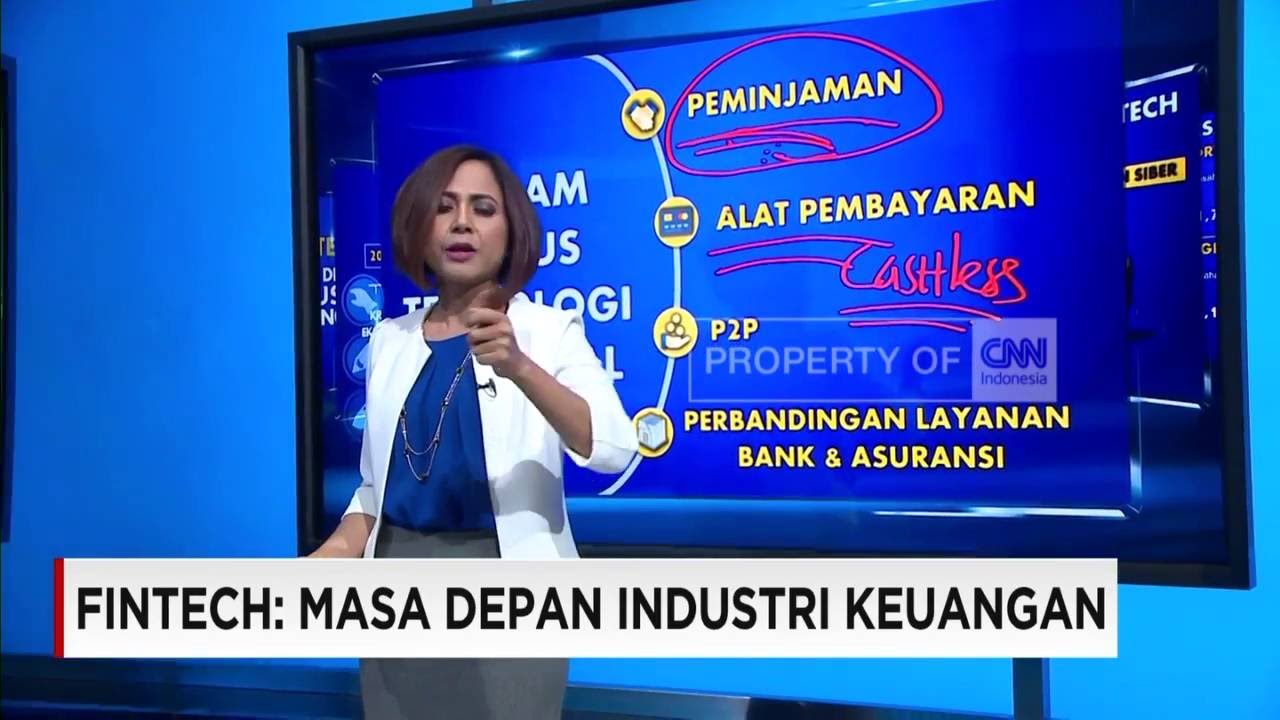

- 📜 The Indonesian financial technology (fintech) sector, known as 'vintage', is an innovation in finance combining financial services with information technology to increase efficiency and ease of use.

- 🇮🇩 Vintage in Indonesia represents a breakthrough in various business aspects, yet the regulatory framework concerning fintech is still underdeveloped and not comprehensively addressed from a legal perspective.

- 🏦 The Otoritas Jasa Keuangan (OJK) and Bank Indonesia have issued several regulations to oversee the financial services industry, including those specific to the vintage sector.

- 📝 OJK Regulation No. 77/2016 aims to regulate peer-to-peer lending services, focusing on consumer protection, fund and data security, money laundering prevention, and terrorism financing prevention.

- 💰 The aforementioned regulation sets standards for share ownership limits, minimum capital, maximum loan amounts, and interest rates, as well as the requirement for an escrow account and adherence to certain mandatory principles.

- 🔄 Bank Indonesia Regulation No. 18/14/PBI/2016 deals with payment transaction processing services and aims to meet the public's needs in the payment services sector, ensuring a broad and robust payment processing infrastructure.

- 🚀 Regulation No. 19/12/PBI/2017 supports the stability of the monetary system and the development of an efficient, smooth, secure, and resilient payment system to support sustainable and inclusive national economic growth.

- 🛡️ This regulation also emphasizes the protection of consumers, risk management, and due diligence principles, in addition to issuing provisions for the implementation of financial technology by the central bank of Indonesia.

- 📋 Regulation No. 16/1615 of the Central Board of Governors concerns the registration, information submission, and supervision of financial technology providers, ensuring a structured approach to monitoring the rapidly growing fintech sector.

Q & A

What does 'vintage' refer to in the context of financial technology in Indonesia?

-In the context of the script, 'vintage' refers to innovations in the financial sector that combine financial services with information technology, representing a breakthrough in Indonesian business aspects, making it more efficient and easier.

How comprehensive are the regulations regarding fintech in Indonesia?

-The regulations concerning fintech in Indonesia are still limited, with no specific laws or regulations fully addressing the fintech industry. However, some regulations have been introduced by the Financial Services Authority (Otoritas Jasa Keuangan) and Bank Indonesia to govern the emerging industry.

What is the main purpose of OJK Regulation No. 77/2016?

-The main purpose of OJK Regulation No. 77/2016 is to protect consumers regarding the safety of funds and data, prevent money laundering and terrorism financing, and ensure the stability of the financial system and the managers of peer-to-peer lending companies.

What are some of the requirements set by OJK Regulation No. 77/2016 for peer-to-peer lending businesses?

-The regulation sets requirements such as share ownership limits, minimum capital, maximum loan and interest rates, the necessity of creating an escrow account, and the implementation of certain mandatory principles by peer-to-peer lending business operators.

What is the aim of Bank Indonesia Regulation No. 18/2016 on payment system providers?

-Bank Indonesia Regulation No. 18/2016 aims to meet the public's needs in the field of payment services by establishing rules for payment system providers, including their licensing, obligations, and reporting requirements, to ensure a comprehensive and efficient payment system.

What does the PP No. 19/2017 regulation cover regarding financial technology?

-PP No. 19/2017 is intended to support the establishment of a stable monetary system and efficient, smooth, safe, and reliable payment system. It applies principles of consumer protection, risk management, and due diligence, aiming to support sustainable and inclusive national economic growth.

What is the focus of the regulation outlined in BI Circular No. 1615/KETENT/Pks.IV/2013?

-BI Circular No. 1615/KETENT/Pks.IV/2013 focuses on the registration, reporting, and supervision of financial technology providers, ensuring that they comply with the necessary regulations and maintain the stability and security of the financial system.

How do the mentioned regulations contribute to the overall financial system in Indonesia?

-The regulations contribute to the overall financial system in Indonesia by providing a structured and regulated environment for the fintech industry, ensuring consumer protection, financial stability, and fostering an efficient and inclusive economic growth.

What is the significance of an escrow account in peer-to-peer lending as mandated by the OJK Regulation?

-The escrow account is significant as it ensures that the funds involved in peer-to-peer lending are securely held and managed by a trusted third party, protecting both the lenders and borrowers from potential misuse of funds.

How do the regulations address the concern of money laundering and terrorism financing in the fintech industry?

-The regulations, particularly OJK Regulation No. 77/2016, directly address these concerns by implementing strict measures for consumer protection and transaction monitoring to prevent money laundering and terrorism financing within the fintech industry.

What is the role of the Financial Services Authority (Otoritas Jasa Keuangan) and Bank Indonesia in regulating the fintech industry?

-The Financial Services Authority and Bank Indonesia play a crucial role in regulating the fintech industry by introducing and enforcing regulations that govern the operations of fintech companies, ensuring consumer protection, financial stability, and compliance with legal and ethical standards.

Outlines

このセクションは有料ユーザー限定です。 アクセスするには、アップグレードをお願いします。

今すぐアップグレードMindmap

このセクションは有料ユーザー限定です。 アクセスするには、アップグレードをお願いします。

今すぐアップグレードKeywords

このセクションは有料ユーザー限定です。 アクセスするには、アップグレードをお願いします。

今すぐアップグレードHighlights

このセクションは有料ユーザー限定です。 アクセスするには、アップグレードをお願いします。

今すぐアップグレードTranscripts

このセクションは有料ユーザー限定です。 アクセスするには、アップグレードをお願いします。

今すぐアップグレード関連動画をさらに表示

Fintech, Masa Depan Industri Keuangan

Peluang dan Tantangan Fintech di Indonesia

Financial Technology - Definisi Fintech, sejarah perkembangan, ruang lingkup, manfaat, dan jenisnya

Finalcial Teknologi -IKNB I Ekonomi Kelas X (Kurikulum Sekolah Penggerak) | EDURAYA MENGAJAR

Fintech is Dead, Long Live Fintech | Vikram Vaidyanathan on the Future of Fintech | Razorpay FTX 24

FINTECH REGULATION EXPLAINED : EVERYTHING YOU NEED TO KNOW

5.0 / 5 (0 votes)