Peluang dan Tantangan Fintech di Indonesia

Summary

TLDRThe speaker discusses the rise and challenges of fintech in Indonesia, tracing its roots to the 2007-2008 financial crisis, which sparked the growth of technology-driven finance solutions like P2P lending. Despite challenges such as low financial literacy and increased regulation, fintech has rapidly expanded, especially in sectors like payments and lending, offering new opportunities for financial inclusion. The speaker emphasizes fintech's potential to boost economic growth, particularly through supporting micro, small, and medium enterprises (UMKMs), and its critical role in enhancing Indonesia's financial accessibility and productivity in the future.

Takeaways

- 😀 Fintech in Indonesia grew significantly due to crises like the 2008 financial crisis and the COVID-19 pandemic, which created opportunities for innovation in the financial sector.

- 😀 The 2008 global financial crisis led to a decline in trust towards traditional banking institutions, paving the way for new technologies like fintech and peer-to-peer lending to emerge.

- 😀 The fintech industry in Indonesia is projected to exceed $100 billion by 2024, with growth expected to continue into 2030, highlighting its potential as a major economic driver.

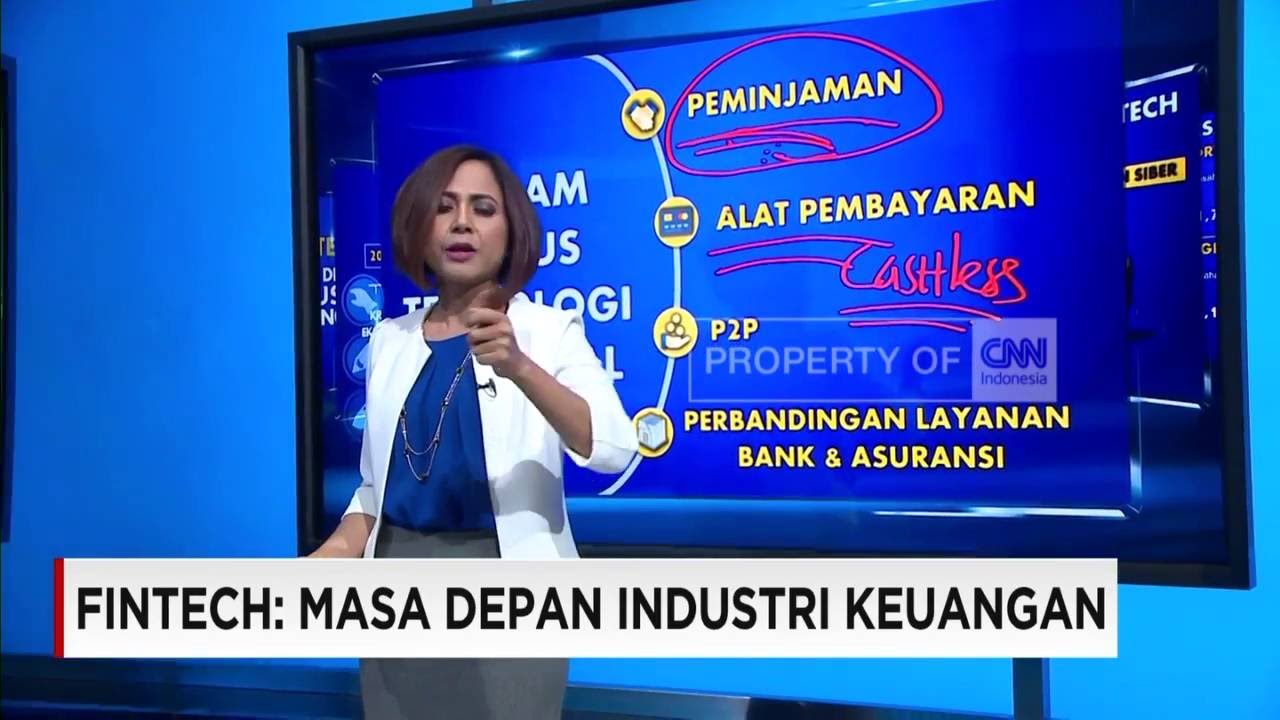

- 😀 Payment services are the largest segment within fintech in Indonesia, with P2P lending and wealth management following behind in terms of assets managed.

- 😀 A major challenge facing Indonesia's fintech industry is financial literacy. Despite high levels of fintech usage (85.1% inclusion), literacy rates remain low at 49.77%.

- 😀 Improving financial literacy is crucial to ensuring that consumers understand the fintech services they use, preventing fraud and misuse, especially among educated segments like university students.

- 😀 The regulatory environment in Indonesia is evolving, particularly with data protection laws such as the Personal Data Protection (PDP) Act, which creates a balance between protecting consumers and fostering innovation.

- 😀 Indonesia’s fintech sector has the potential to drive greater economic inclusion, particularly for underserved groups like small businesses (UMKM), which are often excluded from traditional banking services.

- 😀 Adoption of fintech and technology in Indonesia can lead to increased productivity and economic output, particularly in emerging markets where technology adoption can significantly improve factors of production.

- 😀 Looking ahead, fintech in Indonesia is expected to contribute significantly to the country’s GDP, with projections suggesting a market share of 20% in ASEAN by 2025, driven by inclusive growth and digital financial services.

Q & A

What triggered the emergence of fintech in Indonesia?

-The 2007-2008 financial crisis in the U.S. played a pivotal role in the emergence of fintech. It led to distrust in traditional banking systems and regulatory changes, which created an environment ripe for the rise of technologies like fintech, particularly Peer-to-Peer lending.

How does fintech contribute to economic inclusion in Indonesia?

-Fintech, particularly Peer-to-Peer (P2P) lending, enables access to financial services for underserved sectors, especially SMEs. This allows businesses and individuals who may not qualify for traditional bank loans to access capital, thereby promoting economic inclusion.

Why is financial literacy important in the context of fintech adoption in Indonesia?

-Financial literacy is crucial because many users in Indonesia adopt fintech services without fully understanding them. This gap leads to risks such as fraud, mismanagement, and poor financial decision-making, which can affect even well-educated individuals.

What challenges does Indonesia face in terms of fintech regulation?

-Indonesia faces challenges in balancing innovation and regulation in the fintech sector. The introduction of the Personal Data Protection (PDP) law and the rising need for consumer protection may increase compliance costs for businesses, potentially slowing down the pace of innovation.

What is the projected growth of the fintech sector in Indonesia by 2024?

-According to research from Google, Temasek, and Bain, Indonesia's technology-driven industries, including fintech, are projected to surpass USD 100 billion by 2024, with further growth anticipated by 2030.

How do fintech platforms contribute to Indonesia’s economic growth?

-Fintech platforms, especially P2P lending, contribute to Indonesia's economic growth by providing access to finance for sectors like SMEs, which are often excluded from traditional banking. This inclusion boosts productivity and economic output.

What are the most common fintech sectors in Indonesia, and which has the largest market share?

-The most prominent fintech sectors in Indonesia are P2P lending (35%), payments (33%), and wealth management (17%). Among these, payment services dominate in terms of the assets managed.

What role does crisis play in the development of fintech, according to the speaker?

-The speaker highlights that crises, like the 2008 financial crisis and the 2020 pandemic, often serve as catalysts for the development of fintech. These events create an environment where traditional financial systems fail, paving the way for technological innovations like fintech to meet emerging needs.

What impact does the Personal Data Protection law have on the fintech industry in Indonesia?

-The Personal Data Protection (PDP) law introduces stricter requirements for data management, which increases operational costs for fintech companies. While the law aims to protect consumers, it can pose a challenge for businesses that need to comply with data protection standards.

How does fintech adoption in emerging markets like Indonesia differ from developed countries?

-In emerging markets like Indonesia, the adoption of fintech has a more significant impact on increasing economic output and productivity because these regions have lower technological infrastructure. In contrast, in more developed countries, technology adoption mainly enhances comfort and speed rather than driving substantial increases in productivity.

Outlines

This section is available to paid users only. Please upgrade to access this part.

Upgrade NowMindmap

This section is available to paid users only. Please upgrade to access this part.

Upgrade NowKeywords

This section is available to paid users only. Please upgrade to access this part.

Upgrade NowHighlights

This section is available to paid users only. Please upgrade to access this part.

Upgrade NowTranscripts

This section is available to paid users only. Please upgrade to access this part.

Upgrade NowBrowse More Related Video

Fintech, Masa Depan Industri Keuangan

¿Qué es Fintech? Al tablero con Colombia Fintech

Docuvlog : Ketika ekonomi USA hancur Karena KPR

Financial Technology - Definisi Fintech, sejarah perkembangan, ruang lingkup, manfaat, dan jenisnya

FINTECH 2.0 - THE FUTURE OF FINTECH

Finalcial Teknologi -IKNB I Ekonomi Kelas X (Kurikulum Sekolah Penggerak) | EDURAYA MENGAJAR

5.0 / 5 (0 votes)