Y1/IB 2) Opportunity Cost and Production Possibility Curves (PPCs)

Summary

TLDRThis video explains key economic concepts, focusing on opportunity cost, production possibility curves (PPC), and resource allocation. It explores how choices impact the allocation of scarce resources and highlights the trade-offs involved in producing goods versus services. The concept of Pareto efficiency is introduced, showing how no one can be made better off without making someone else worse off. The PPC is used to demonstrate opportunity cost, with increasing specialization leading to higher trade-offs. Finally, the video covers how shifts in resource availability affect production capacity.

Takeaways

- 💡 The economic problem forces societies to make choices about what to produce, how to produce it, and for whom to produce it.

- 🔄 Opportunity cost is the value of the next best alternative foregone when a decision is made.

- 🛑 Free goods, like sunlight and air, have no opportunity cost because they are in unlimited supply.

- 📉 Economic goods, on the other hand, have opportunity costs because they are scarce and require allocation.

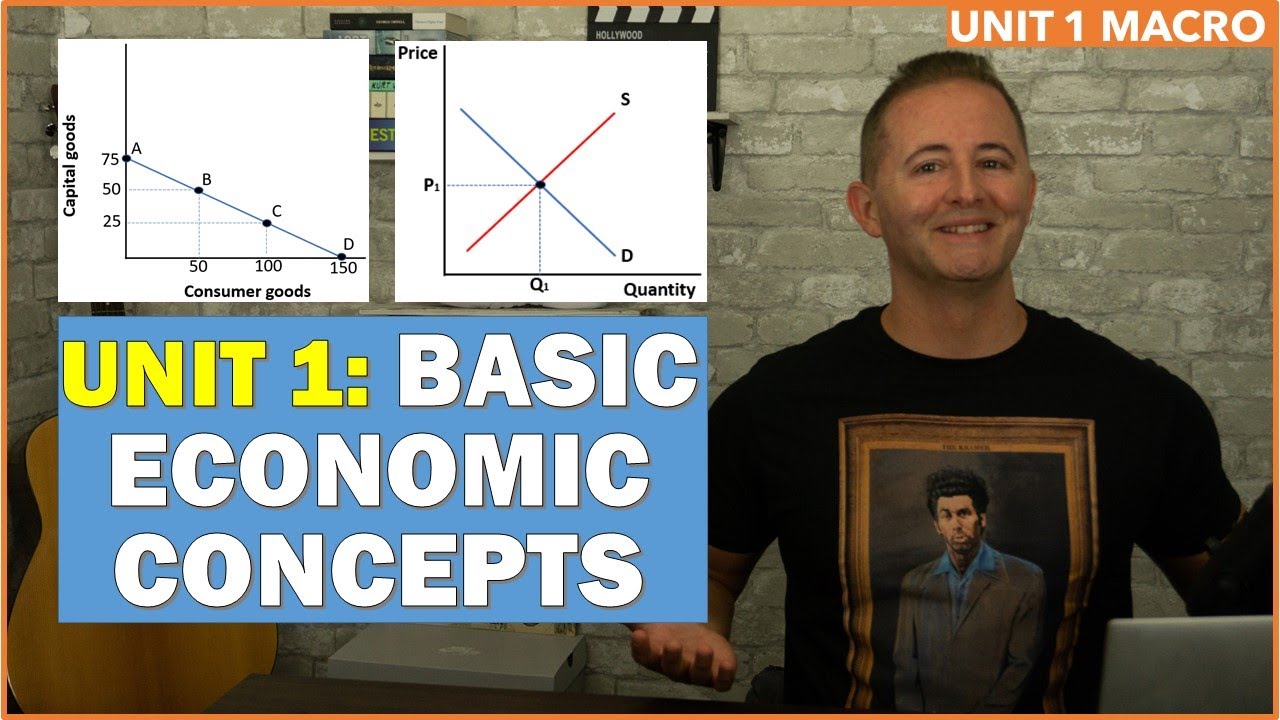

- 📊 A Production Possibility Curve (PPC) shows the maximum production capabilities of an economy using scarce resources.

- ⚖️ Points inside the PPC represent inefficiency, while points on the curve indicate productive efficiency.

- 🚫 Points outside the PPC are unattainable given current resource constraints.

- 📈 As an economy specializes more in one type of good, the opportunity cost of producing more increases.

- ⚙️ The PPC shifts outward when there is an increase in the quantity or quality of factors of production, such as labor or capital.

- 🤝 Pareto efficiency occurs when it’s impossible to make one person better off without making someone else worse off.

Q & A

What is opportunity cost?

-Opportunity cost is the cost of the next best alternative that is forgone when a choice is made. It refers to what is given up to pursue a particular option.

Can free goods have an opportunity cost?

-No, free goods like sunlight, seawater, and air have no opportunity cost because they are in unlimited supply and there is no need to allocate them.

What is a Production Possibility Curve (PPC)?

-A Production Possibility Curve (PPC) shows the maximum amount of two goods or services that can be produced in an economy given the available resources and factors of production. It illustrates trade-offs and opportunity costs.

What does it mean for an economy to be 'productively inefficient'?

-An economy is productively inefficient if it operates inside the PPC, meaning it is not utilizing all of its resources effectively, and thus could produce more of either or both goods and services.

What does a point on the PPC curve represent?

-A point on the PPC curve represents a productively efficient use of resources, where the maximum possible output is being achieved with the available resources.

What is Pareto efficiency?

-Pareto efficiency occurs when no one can be made better off without making someone else worse off. Any point on the PPC represents Pareto efficiency, as resources are being used in the most efficient way.

What happens when an economy moves from point A to point B on the PPC?

-When an economy moves from point A to point B on the PPC, it reallocates resources to produce more of one good and less of another, reflecting opportunity costs and changes in the combination of goods and services produced.

Why does opportunity cost increase as an economy specializes in producing more of one good?

-Opportunity cost increases as specialization occurs because resources become less suited for producing additional quantities of the specialized good, resulting in higher trade-offs or sacrifices in the production of the other good.

What causes the PPC to shift outward?

-The PPC shifts outward when there is an increase in available resources, improvements in technology, or other factors that enhance production capabilities.

Outlines

このセクションは有料ユーザー限定です。 アクセスするには、アップグレードをお願いします。

今すぐアップグレードMindmap

このセクションは有料ユーザー限定です。 アクセスするには、アップグレードをお願いします。

今すぐアップグレードKeywords

このセクションは有料ユーザー限定です。 アクセスするには、アップグレードをお願いします。

今すぐアップグレードHighlights

このセクションは有料ユーザー限定です。 アクセスするには、アップグレードをお願いします。

今すぐアップグレードTranscripts

このセクションは有料ユーザー限定です。 アクセスするには、アップグレードをお願いします。

今すぐアップグレード関連動画をさらに表示

(EKONOMI INTERNASIONAL) TEORI TEORI PERDAGANGAN INTERNASIONAL part 2

(Production Possibility Frontier/Curve, PPF, PPC) Why can't things be free?

PEMBAHASAN SOAL OSN EKONOMI TAHUN 2020 TINGKAT KABUPATEN KOTA

INTRODUCTION TO MICROECONOMICS CLASS 11 ECONOMICS CHAPTER 1 ONE SHOT 2025-2026

Konsep Ilmu Ekonomi dan Permasalahannya - Materi Ekonomi SMA dan Ujian Mandiri

Unit 1 Macro Review - Basic Economic Concepts

5.0 / 5 (0 votes)