Audit || Faktor-faktor Risiko Salah Saji Laporan Keuangan

Summary

TLDRThis video explores the key risk factors of material misstatements in financial statements according to audit standards. It explains three main categories: inherent risk, control risk, and fraud risk. Inherent risk relates to the nature of transactions and accounts, especially complex or non-routine ones. Control risk involves the effectiveness of internal controls, particularly in computerized systems. Fraud risk highlights pressures, opportunities, and rationalizations that may lead to financial misstatements. The video emphasizes that understanding these risks helps auditors focus their procedures, but assessment alone does not replace substantive audit work. Practical examples clarify each risk type for better comprehension.

Takeaways

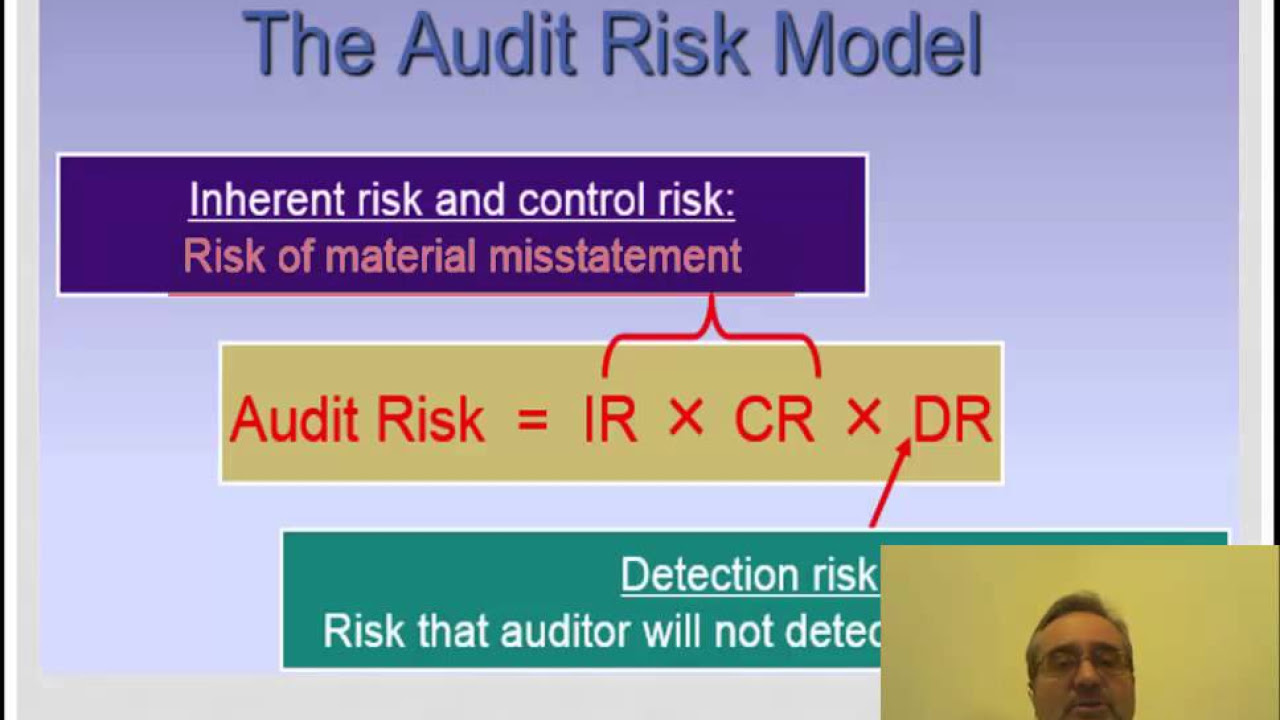

- 😀 Auditors must perform risk assessment procedures to identify and evaluate the risk of material misstatement in financial statements, as mandated by audit standards SA 315.

- 😀 Risk assessment alone is insufficient for forming an audit opinion; additional audit procedures, including substantive testing and control testing, are necessary.

- 😀 There are three main categories of risk factors: inherent risk, control risk, and fraud risk.

- 😀 Inherent risk arises from characteristics of the entity, transactions, or accounts, and is influenced by the complexity, nature, and history of past corrections.

- 😀 Accounts requiring subjective judgment, such as depreciation or asset write-offs, typically have higher inherent risk compared to more objective accounts.

- 😀 Control risk is associated with the effectiveness of internal controls in ensuring reliable financial reporting, operational efficiency, and compliance with laws and regulations.

- 😀 Auditors should assess risks related to computerized information systems, including uniform processing, automatic transactions, and potential unauthorized access or undetectable changes to electronic data.

- 😀 Fraud risk indicates the possibility, but not the certainty, of fraud occurring, and is classified into three elements: incentives/pressure, opportunities, and attitudes/rationalizations.

- 😀 Incentives or pressures can include performance targets, unrealistic deadlines, threats of job loss, or personal financial needs, increasing the risk of misstatement.

- 😀 Opportunities for fraud arise when controls are weak, such as access to high-value assets, ability to override controls, or transactions requiring significant subjective judgment.

- 😀 Attitudes or rationalizations that contribute to fraud risk include employees perceiving management as unethical, feeling entitled to assets, or believing honest reporting may lead to punishment.

- 😀 Understanding management’s responses and the effectiveness of internal controls is essential for auditors to evaluate the nature, timing, and extent of risks in financial statements.

Q & A

What is the main focus of the video by Haryandani?

-The main focus is on the factors of misstatement risk in financial statements, especially material misstatements, and how auditors identify and assess these risks during financial audits.

According to SA 315, what is the purpose of risk assessment procedures in auditing?

-Risk assessment procedures are performed to provide a basis for identifying and assessing the risk of material misstatement in financial statements and assertions. They do not, by themselves, provide sufficient audit evidence for the audit opinion.

What are the three main categories of risk factors that auditors need to consider?

-The three main categories are inherent risk factors, control risk factors, and fraud risk factors.

Can you explain what inherent risk is in the context of financial audits?

-Inherent risk refers to the susceptibility of an account, transaction, or assertion to a material misstatement due to its nature or characteristics, without considering any related internal controls.

What types of entities or transactions are considered more vulnerable to inherent risk?

-Entities with complex programs, non-routine transactions, accounts requiring significant subjective judgment, or activities involving consumable goods or expiring inventory are generally more vulnerable to inherent risk.

How does control risk affect the audit process?

-Control risk reflects the risk that a material misstatement will not be prevented or detected by the entity’s internal controls. Auditors focus on testing relevant controls to determine whether they are effective in ensuring reliable financial reporting and compliance with laws.

What are some key considerations regarding information systems when assessing control risk?

-Auditors should consider that automated processing can lead to consistent errors if programming is faulty, minimal human involvement can hide misstatements, and personnel competence in operating the system must be evaluated.

What are the three elements of fraud risk according to the video?

-The three elements are incentive or pressure, opportunity, and rationalization or attitude of employees.

Can the presence of fraud risk factors be interpreted as evidence of fraud?

-No, the presence of fraud risk factors only signals that fraud could occur. It does not indicate that fraud has actually taken place.

How can incentives or pressures contribute to fraud risk in financial statements?

-Incentives or pressures, such as the desire to report higher profits for bonuses, unrealistic performance targets, or personal financial pressures, can motivate employees or management to manipulate financial reporting.

What role does opportunity play in increasing fraud risk?

-Opportunity arises when management or employees can override controls, process unusual transactions, or access valuable assets with weak controls, creating a chance to commit fraud without immediate detection.

How do behavior and rationalization affect fraud risk?

-Employees may rationalize fraudulent behavior by believing that reporting honestly leads to punishment, that performance targets are unrealistic, or that management is unethical, which can make fraud seem acceptable or justified.

Outlines

Cette section est réservée aux utilisateurs payants. Améliorez votre compte pour accéder à cette section.

Améliorer maintenantMindmap

Cette section est réservée aux utilisateurs payants. Améliorez votre compte pour accéder à cette section.

Améliorer maintenantKeywords

Cette section est réservée aux utilisateurs payants. Améliorez votre compte pour accéder à cette section.

Améliorer maintenantHighlights

Cette section est réservée aux utilisateurs payants. Améliorez votre compte pour accéder à cette section.

Améliorer maintenantTranscripts

Cette section est réservée aux utilisateurs payants. Améliorez votre compte pour accéder à cette section.

Améliorer maintenant

5.0 / 5 (0 votes)