UK ISA Accounts Explained | Everything you Need to Know (2025)

Summary

TLDRIn this video, the presenter explains everything you need to know about ISAs (Individual Savings Accounts) in the UK. They cover the different types of ISAs, including cash ISAs, stocks and shares ISAs, lifetime ISAs, innovative finance ISAs, and junior ISAs. The presenter discusses the benefits, limitations, and specific requirements of each type, offering valuable tips on how to maximize your savings. They also highlight the importance of understanding tax-free benefits, ISA limits, and how to manage your ISA accounts effectively. The video serves as a comprehensive guide for anyone looking to open an ISA.

Takeaways

- 😀 An ISA (Individual Savings Account) allows tax-free savings or investments in the UK, with a yearly limit on contributions.

- 😀 The annual ISA allowance for the 2023-2024 tax year is £20,000, which resets at the start of each tax year.

- 😀 Money withdrawn from an ISA does not increase your allowance; it stays the same until the next tax year resets it.

- 😀 Cash ISAs allow you to save money without worrying about paying tax on any interest earned, unlike a standard savings account.

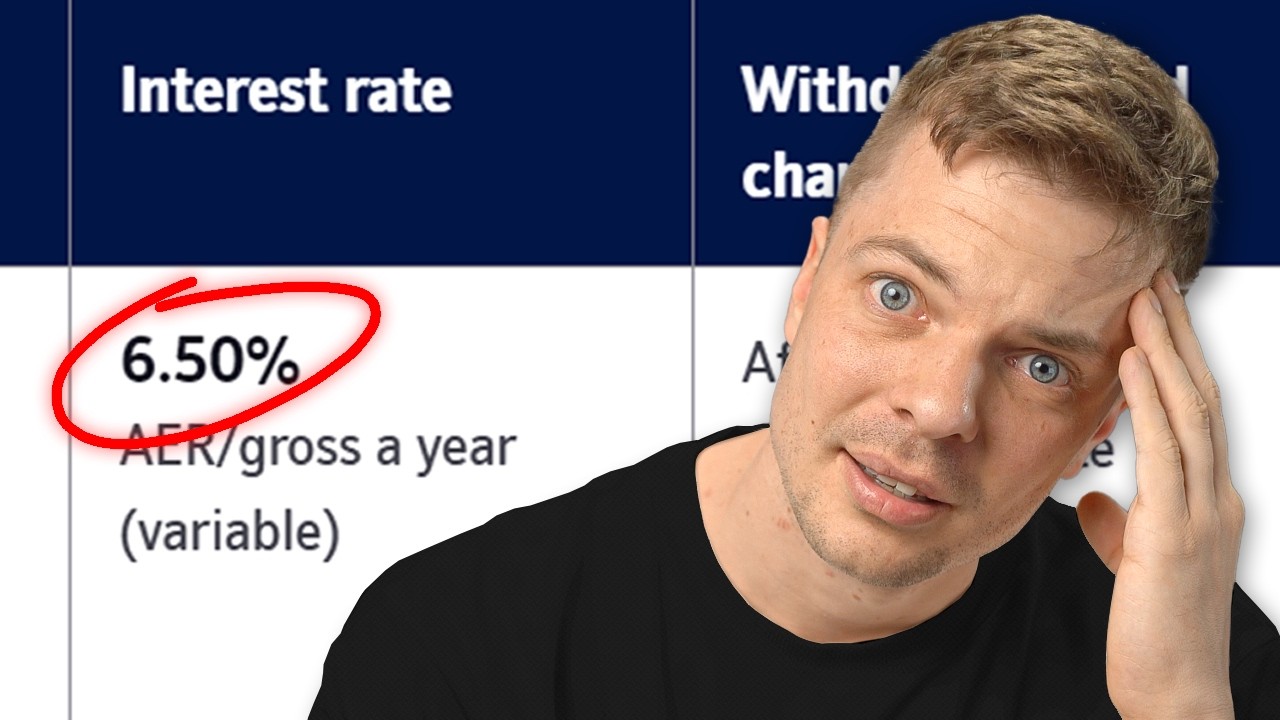

- 😀 There are two main types of Cash ISAs: easy access (no penalties for withdrawal) and fixed-rate (higher interest but penalties for early withdrawal).

- 😀 Stocks and Shares ISAs allow you to invest in stocks, funds, and bonds, offering potential for higher returns, but with more risk.

- 😀 A Stocks and Shares ISA is ideal for long-term wealth building, especially when invested over five years or more to smooth out market fluctuations.

- 😀 Lifetime ISAs, launched in 2017, allow you to save for a first home or retirement with a £4,000 contribution limit each year, plus a 25% government bonus.

- 😀 With Lifetime ISAs, the government adds a 25% bonus on your savings, but there are penalties if the money is withdrawn for purposes other than buying a house or retirement.

- 😀 Innovative Finance ISAs allow you to lend money to businesses, with tax-free interest earned, but come with higher risk due to the nature of lending.

- 😀 Junior ISAs (JISAs) are for saving on behalf of children, with a £9,000 annual limit, and they sit outside the standard £20,000 ISA limit for adults.

- 😀 If your child is aged 16 or 17, they can access both Junior ISA and standard ISA allowances, but they cannot access their Junior ISA funds until 18.

- 😀 You can have multiple ISAs, but the combined contributions across all your ISAs cannot exceed the £20,000 annual limit.

- 😀 If you want to switch ISA providers, avoid withdrawing your funds to ensure you don't waste your annual allowance—transfers are the better option.

- 😀 The ISA limit resets every year, so it's important to try to maximize your contribution before the reset to take full advantage of the tax-free allowance.

Q & A

What is an ISA and why should everyone have one?

-An ISA (Individual Savings Account) is an account where you can save or invest your money without paying tax on the gains. Everyone should consider having one as it allows you to grow your wealth tax-free, which can be very beneficial for long-term savings and investments.

How much can I contribute to an ISA each year?

-For the tax year 2023 to 2024, you can contribute up to £20,000 to your ISA. However, this is an annual limit, and it resets at the start of each new tax year.

What happens if I don't use the full ISA allowance in one year?

-If you don’t use the full £20,000 allowance in a year, it doesn’t roll over to the next year. The limit resets each year, and you lose the unused portion of the allowance.

What is the difference between a cash ISA and a stocks and shares ISA?

-A cash ISA is where you store your money in a savings account with interest, while a stocks and shares ISA allows you to invest in assets like stocks, bonds, and funds. Cash ISAs are generally lower risk but offer lower returns, while stocks and shares ISAs come with higher risk but greater potential for returns.

What is the personal savings allowance, and how does it relate to a cash ISA?

-The personal savings allowance is the amount of interest you can earn on savings before paying tax. For basic-rate taxpayers, it's £1,000, and for higher-rate taxpayers, it's £500. If you earn interest above this allowance in a standard savings account, you'll pay tax on it. However, interest earned in a cash ISA is tax-free and does not count toward the personal savings allowance.

What are easy access ISAs and fixed-rate ISAs?

-Easy access ISAs allow you to access your funds whenever needed without penalties, while fixed-rate ISAs require you to lock your money away for a set period in exchange for a higher interest rate. With fixed-rate ISAs, withdrawing funds early usually results in a penalty.

Who should consider opening a stocks and shares ISA?

-A stocks and shares ISA is ideal for those with a long-term investment horizon and an understanding of market risks. If you're willing to take on some risk for potentially greater returns, this ISA can be a good option.

What is a Lifetime ISA and who can open one?

-A Lifetime ISA is designed to help people save for their first home or retirement. You can contribute up to £4,000 per year, and the government adds a 25% bonus on the amount you save, up to a maximum of £1,000 per year. To open one, you must be aged between 18 and 39.

What are the penalties associated with a Lifetime ISA?

-If you withdraw money from a Lifetime ISA and do not use it for buying a first home or for retirement, you will incur a penalty of 25%, which works out to about a 6% loss on the original amount saved.

Can you have multiple ISAs, and how does the £20,000 limit apply?

-Yes, you can have multiple ISAs, but the £20,000 limit applies to the total contributions made across all your ISAs combined, not individually. For example, you can contribute £10,000 to a cash ISA and £10,000 to a stocks and shares ISA in the same year, as long as the total doesn’t exceed £20,000.

Outlines

Cette section est réservée aux utilisateurs payants. Améliorez votre compte pour accéder à cette section.

Améliorer maintenantMindmap

Cette section est réservée aux utilisateurs payants. Améliorez votre compte pour accéder à cette section.

Améliorer maintenantKeywords

Cette section est réservée aux utilisateurs payants. Améliorez votre compte pour accéder à cette section.

Améliorer maintenantHighlights

Cette section est réservée aux utilisateurs payants. Améliorez votre compte pour accéder à cette section.

Améliorer maintenantTranscripts

Cette section est réservée aux utilisateurs payants. Améliorez votre compte pour accéder à cette section.

Améliorer maintenant

5.0 / 5 (0 votes)